PAYMENTS ON THE GO: MAKING SENSE OF THE EVOLVING MOBILE PAYMENTS LANDSCAPE - INCLUDE INTRODUZIONE AL CONTESTO ITALIANO - PWC

←

→

Trascrizione del contenuto della pagina

Se il tuo browser non visualizza correttamente la pagina, ti preghiamo di leggere il contenuto della pagina quaggiù

www.pwc.com/fsi

Payments on the go:

Making sense of the evolving

mobile payments landscape

Include introduzione

al contesto italiano

Payments on the go: un’istantanea del mercato

italiano

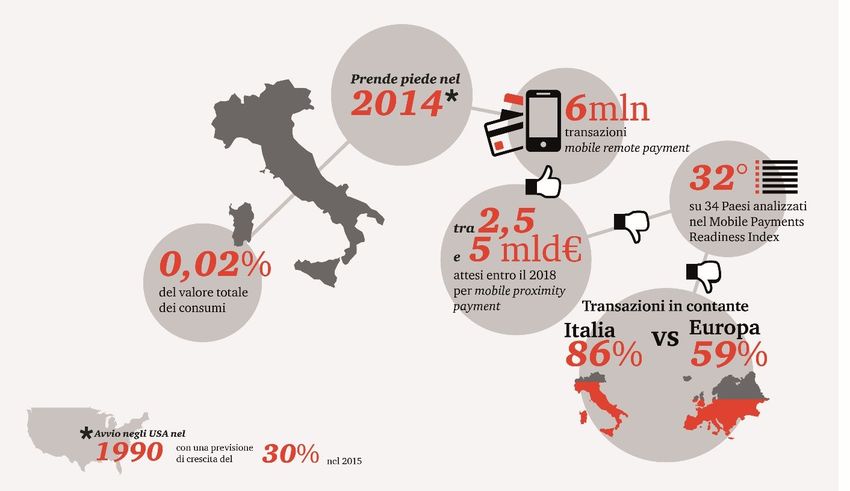

Le pagine che seguono presentano tramite mobile; è in quest’anno anche rispetto agli altri Paesi

alla comunità finanziaria italiana che cominciano infatti a europei, il mercato è ancora poco

alcuni spunti di riflessione registrarsi i primi dati di qualche sviluppato (nel 2014, il transato

elaborati dal Financial Services rilievo per volumi di transazione del MP è stato di 0,2 miliardi su

Institute di PwC sulla diffusione e eseguite (nel 2014 si sono 950, pari allo 0,02% del valore

lo sviluppo del Mobile Payments registrate 6 milioni di transazioni totale dei consumi italiani3). Nella

(MP) negli Stati Uniti, indagando relative al mobile remote classifica relativa al MP Readiness

le sue prossime evoluzioni e payment1). Index4, l’Italia si trova infatti in

suggerendo possibili indirizzi terz’ultima posizione su 34 stati

futuri. Ciò permetterà di ricavare Con il passare del tempo il analizzati. Uno dei motivi è il forte

alcuni utili elementi di confronto e concetto di MP oltreoceano è attaccamento italiano al denaro

di differenza anche con il mercato cambiato e si è ampliato: oggi con contante, ancora largamente

italiano. questo termine si intende la utilizzato (circa l’86% delle

possibilità di pagare prodotti e transazioni di importo inferiore a

Se negli States il MP era già servizi, sia in prossimità che da 100 € è effettuato in contante,

diffuso a partire dagli inizi degli remoto e trasferire denaro con gli rispetto al 59% delle transazioni in

anni novanta (alcune compagnie smartphone. Il livello di diffusione contante in Europa) e il ritardo

petrolifere consentivano ai propri di questa forma di pagamento è in nell’adozione delle tecnologie

clienti di pagare direttamente alla Nord America in forte espansione adeguate.

pompa con dispositivi RFID, (+30% di crescita prevista per il

mentre diverse organizzazioni di 2015 rispetto all’anno

beneficienza raccoglievano denaro precedente2), mentre in Italia,

attraverso mobile donations), per

il mercato italiano è il 2014 l’anno 1 Osservatorio Mobile Payment & Commerce del 3 Osservatorio Mobile Payment & Commerce del

reale d’avvio dei pagamenti 2

Politecnico di Milano

Forrester Research, “US mobile payments forecast, 2014 to

Politecnico di Milano. “Mobile Payment & Commerce: un

ponte tra il mondo fisico e il mondo digitale.” 2013-2014.

2019,” November 17, 2014 4 http://mobilereadiness.mastercard.com/the-index

2

In aggiunta, nel mercato italiano

si registrano quasi esclusivamente

operazioni di mobile remote

payment con tassi di crescita

simili a quelli americani (15%

annuo circa): questa è la forma di

pagamento in prevalenza legata

alla possibilità di utilizzare gli

smartphone per il pagamento di

bollettini, parcheggi, trasporti e

car sharing, che negli States è gia

utilizzata anche per il pagamento

di prodotti a distanza.

Nonostante il ritardo italiano ad

oggi registrato, nell'adozione del

MP e delle nuove tecnologie

collegate (quali i sistemi NFC ed i

contactless Pos), i segnali per i

prossimi anni sembrano positivi.

Secondo una ricerca Il MP nel mondo delle Solo più di recente si è cominciato

dell'Osservatorio Mobile Economy Financial Institutions a guardare al MP come ad

ci si aspetta infatti, entro il 2018, un’evoluzione dei pagamenti

un forte sviluppo del mobile tradizionali ed una potenziale

proximity payment, ovvero i Come emerge dal documento opportunità di sviluppo e di

pagamenti in prossimità effettuati americano, il MP è stato percepito rafforzamento del ruolo

con lo smartphone (tra 2,5 e 5 inizialmente dalle istituzioni dell’intermediario finanziario

miliardi di euro) e delle finanziarie, specialmente banche, nella filiera dei pagamenti, oltre

transazioni effettuate attraverso i come una minaccia. La possibilità che un’opportunità per creare un

Mobile Pos per acquistare beni e di creare nuovi modelli di business modello di relazione multicanale

servizi (circa 2 miliardi di euro). legati ai pagamenti e il con il cliente, dove i dispositivi

conseguente ingresso di nuovi mobili rappresentano un pilastro

Un incentivo allo sviluppo in Italia competitor nel mercato dei fondamentale. Negli anni recenti

potrebbe arrivare dalle Pubbliche pagamenti, anche se il loro peso le banche italiane hanno iniziato a

Amministrazioni. Ad oggi sono resta tuttora marginale, ha proporre soluzioni innovative ed

infatti ancora poche le PA e gli portato gli intermediari finanziari alcune prime esperienze di

Enti (inclusi Comuni e Città a ripensare alla catena del valore successo si sono affermate anche

metropolitane) che hanno dei pagamenti nel suo complesso in Italia, sia basate sul modello

sviluppato applicazioni per il per cercare di mantenere un NFC sia remote.

pagamento dei servizi di pubblica presidio sui clienti che sono alla

utilità in mobilità (le principali si ricerca di forme di pagamento più

legano alla vendita online di innovative e in mobilità.

ticket). A tendere la competizione fra le

diverse soluzioni si giocherà sulla

A questo proposito il Governo capacità da parte dei diversi

italiano, nell’ambito delle player di garantire al cliente non

iniziative legate all’Agenda solo sicurezza ed affidabilità dei

Digitale (es. Nodo dei Pagamenti, sistemi, ma anche un’esperienza di

Identità digitale, etc.), sta pagamento positiva ed integrata

promuovendo lo sviluppo dei con tutti i servizi del mobile wallet.

servizi digitali offerti dalle PA e

spronando alla maggiore

diffusione di questi.

3

A questa opportunità stanno già I fattori critici di La sfida per gli operatori sarà

lavorando da tempo gli over the successo dunque quella di far leva da un

top (Google, Apple, Microsoft e lato su valori di base quali

Samsung), che a poco a poco si comodità, sicurezza e velocità,

stanno affacciando anche al Come insegna l’esperienza dall’altro di garantire insieme al

mercato italiano e che basano le americana, i principali fattori che pagamento anche servizi

loro soluzioni proprio nel corso dei prossimi anni aggiuntivi quali:

sull’esperienza distintiva nel incideranno in maniera

pagamento da far vivere al significativa sullo sviluppo e la

cliente. Sarà interessante valutare diffusione del MP sono la loyalty program, coupon,

quanto il mercato degli customer experience, l’utilizzo e la premi e sconti;

smartwatch potrà rafforzare la sicurezza dei dati, la servizi informativi pre e post

user experience di un acquisto in collaborazione e la partecipazione vendita (quali ad esempio:

mobilità e trainare il business dei dei diversi attori coinvolti nella filiera. suggerimenti, confronto prezzi

pagamenti. Ad oggi le previsioni e informazioni sui prodotti);

di vendita di Apple Watch integrazione dei diversi sistemi

A conferma, la recente indagine di di pagamento (peer to peer,

PwC7 sulla user experience nel proximity e remote).

indicano5 circa 2,8 milioni di soli mercato italiano dimostra che il

preordini in US contro i 3,27 cliente non è di fatto ancora in

milioni di iPad 1 venduti nel grado di percepire il valore del Da non trascurare gli aspetti di

relativo primo trimestre dal MP come strumento di pagamento protezione e corretto uso dei dati

lancio. Considerando che in tutto in sé, alternativo al tradizionale personali: questa è una delle fonti

il 2014 sono stati venduti utilizzo di carte e contanti, ma solo di maggiore preoccupazione del

globalmente6 circa 6,8 milioni di come parte integrante di cliente. È necessario infatti che le

wearable da polso, tra un’esperienza legata ai istituzioni finanziarie prestino

smartwatch e braccialetti da beni/servizi che sta acquistando. attenzione allo sviluppo di

fitness, si può prevedere che il adeguati e sofisticati metodi di

biennio 2015-2016 sarà un authorization e authentication.

periodo di forte cambiamento per Questi vanno poi opportunamente

il settore dei wearable e dei comunicati e fatti percepire al

relativi servizi abilitati, tra cui i cliente finale senza penalizzare

pagamenti in mobilità. l’usabilità e l’esperienza di

pagamento.

5 Dati di vendita Apple, Slice Intelligence, maggio 2015 7 PwC, “Total Retail 2015. Analisi dei risultati per il

6 Analisi Smartwatch Group, febbraio 2015 mercato italiano e confronto con i principali Paesi”, 2015

4

Potenziali opportunità Gli aspetti di data monetisation La sfida per l’Italia consisterà nel

infatti sono quelli su cui si stanno puntare a soluzioni integrate ed

concentrando i principali interoperabili più sicure e

Un freno da rimuovere allo operatori del mercato americano. convenienti, sia per il cliente sia

sviluppo del MP, sia nel mercato per il merchant. In tale contesto

italiano sia nord americano, è la Alcuni dati posso dare un segnale saranno di supporto quegli

collaborazione spesso difficoltosa del fenomeno8: se il Global interventi legislativi che tramite

tra i diversi attori coinvolti nella Advertising Spending è dato adeguati sistemi di incentivi

filiera (operatori telefonici, PSP, crescere a un CAGR del +4,7% tra favoriscano sempre più lo

merchant). il 2015 e il 2019, nello stesso sviluppo del digitale e dei

periodo il Global Consumer pagamenti elettronici (es. incentivi

In particolare, i merchant/retailer Spending salirà di solo il +2,9%. fiscali per adottare sistemi di

non considerano il MP come un Questo significa che il mercato accettazione/App per veicolare in

servizio sufficientemente sarà ancora più dipendente dagli elettronico volumi significativi di

redditizio e dimostrano una certa investimenti in pubblicità, e da transazioni anche per importi

riluttanza ad investire in nuove quanto i merchant sapranno inferiori ai 50€).

tecnologie di cui non percepiscono essere distintivi in tale contesto.

benefici immediati. Un possibile Customer experience, marketing

incentivo per questi merchant Sul lato dell’offerta, i diversi attori automation, utilizzo e sicurezza

potrebbe essere legato allo stanno lavorando sulla customer dei dati, importanza di servizi

sfruttamento e monetizzazione dei experience, integrando il MP con addizionali sono alcune delle

dati sottostanti le transazioni di servizi addizionali, consentendo al riflessioni su tendenze ed

pagamento. merchant/retailer l’accesso ad evoluzioni future che possono

una mole di dati strutturati e rappresentare un sicuro spunto

Altro elemento rilevante è quello utilizzabili per permettergli di anche per gli operatori del

rappresentato dalla gestione delle rafforzare la conoscenza e la mercato italiano; tali aspetti

informazioni. Il MP è in grado di relazione. In Italia, pur nella vengono ripresi e discussi nel

veicolare una mole significativa di coscienza di dover sfruttare al punto di vista sul mercato

dati relativi alle abitudini di meglio i dati delle transazioni americano che illustra come

acquisto del cliente che, se gestite come una opportunità per evolvere nel MP.

ed utilizzate adeguatamente, conoscere meglio il cliente, sono

possono garantire al presenti sul mercato ancora poche

merchant/retailer una visione iniziative e progettualità di rilievo

complessiva di comportamenti e che facciano da traino per il lancio

abitudini del proprio cliente. di questi servizi.

La disponibilità di dati su gusti, Lato domanda, per evitare freni e

consuetudini e tipologie di tutelare il consumatore, ma anche

acquisto, se opportunamente per incrementare la fiducia dei

integrate con le informazioni consumatori e la crescita

derivanti dagli altri canali di dell’innovazione digitale, a livello

vendita, potrebbero essere UE è in corso di definizione la

sfruttate per sviluppare campagne normativa di contesto9 che

promozionali e di marketing, dovrebbe essere applicata a

offerte, sconti e premi regime nel biennio 2017-2018.

personalizzati per il singolo

consumatore, aumentando il

valore dell’offerta al cliente e

rafforzando la relazione.

8 PwC, “Global Entertainment & Media Outlook 2015-

2019”, giugno 2015

9 General Data Protection Regulation (GDPR)

5

Contatti Marco Folcia Gianluca Meardi marco.folcia@it.pwc.com gianluca.meardi@it.pwc.com (02) 66720433 (02) 66720396

The heart of the matter

Despite an estimated $142 billion market for

mobile payments by 2019, few solutions have

gained traction in the US. 1 Scattered successes

among a few providers have revealed what may

be the logical direction for success, but the

landscape is still fragmented and unknown.

To succeed, a mobile payment system will have to

solve multiple issues that have stymied adoption

in the past. How should merchants and technology

innovators work out the best plan for moving

forward?

Mobile phones have already Nevertheless, it remains difficult for Whichever mobile payment system

revolutionized our lives, often taking merchants who want to save money succeeds, it will have to entice

the place of cameras, calculators, and and better serve customers to figure adoption on both sides of the

paper tickets from airlines. What out the best plan for participating in equation; that is, it must appeal to

they haven’t replaced—yet—is this increasingly important arena. both merchants and customers. It

money. The mobile trend has also While other international payment will have to solve multiple issues that

spawned countless mobile payment options, such as M-Pesa, have have so far stymied adoption. These

systems, but most have gained little established a foothold in regions range from convenience and user

or no traction among merchants or where payment alternatives were experience to security and cost.

consumers in the US. 10 slim, the challenge in the US and

other developed countries is

With the stakes rising, this is about different. In these countries,

to change. As seen in Figure 1, innovators need to figure out more

Forrester Research projects that the than just delivering a convenient and

mobile payments market will jump to secure payment solution. They need

$142 billion by 2019.11 These stakes to offer a broader, more satisfying

have driven innovators to keep trying customer experience—one that

with unflagging zeal. encompasses a much larger value

chain that could involve loyalty

rewards, discounts, and other

incentives, and perhaps even perks

and experiences no one has

considered yet.

10 Forrester Research, “US mobile payments forecast, 2014 to

2019,” November 17, 2014.

11 Ibid.

Payments on the go:

Making sense of the evolving mobile payments landscape 7

Figure 1: US mobile payments expected to hit $142 billion by 2019. Source: Forrester Research, “US mobile payments forecast, 2014 to 2019,” November 17, 2014. Payments on the go: What mobile means for merchants and tech players 8

An in-depth discussion

A short history of mobile For years, companies have tried to technology players. Merchants are

payments figure out ways to make mobile also hesitant to invest. New payment

payments simple, almost all without solutions may require costly new

Several years ago, as we noted in our

widespread success. Startups such as point-of-sale devices and software

2011 FS Viewpoint, Dialing Up a

Bling Nation, FaceCash, FonePays, implementations or, if handled by

Storm, financial institutions were at

and Obopay have come and gone.12 another party in the process,

risk of losing their place in the

Even larger, established companies merchants may lose insight into

payments value chain to telcos,

have had trouble with mobile which customers are buying which

technology innovators, and device

payment systems. In 2010, AT&T items.

manufacturers, among others. That

Mobility, T-Mobile, and Verizon

threat is still alive today, but it’s At the same time, consumers are

Wireless announced the Isis Mobile

become clear that mobile payment reluctant to switch to a payment

Wallet (renamed Softcard in 2014),

solutions are part of an evolution, system that has not been proven to

eventually teaming with major card

rather than a revolution, in a be more convenient or more secure

companies. By leveraging near-field

changing payments landscape. than what they already use. Indeed,

communication (NFC) technology,

users were able to pay by tapping a lacking additional incentives,

Even what we think of as “mobile

payment terminal with their mobile consumers have little reason to

payments” is changing. As early as

device. However, as with other switch to something that requires

the 1990s, oil companies began

efforts, its potential for success was downloading a new app and shifting

developing RFID chip-enabled

unclear. While Google shut down ingrained habits from a card swipe to

devices that customers could wave at

Softcard’s operations after it a relatively more complicated

the pump to buy gasoline. Charities

acquired the company in 2015, it is smartphone. As seen in Figure 2,

have raised millions of dollars by

leveraging certain aspects of the consumers expect many services to

enabling givers to send text-message

technology in Google Wallet. be included in a mobile wallet.

donations that are charged to their

wireless accounts and passed on to

In the face of complexity,

charities by their carriers. More

success remains elusive

recently, companies like Square have

given food truck vendors and other Why is success so elusive? There is

small businesses the ability to accept no single answer, because mobile

credit card payments with a small payments are elbowing their way into

card-reading device that works with an established, complicated

smartphones and tablets. Although ecosystem. Getting financial services

these are all forms of mobile players, card networks, merchants,

payments, in this article we focus on smartphone manufacturers, and

the “in-person” solutions that enable telcos to collaborate was never easy.

customers to use their smartphones The question of how best to avoid

to pay for goods and services at fraud risks was also difficult to

brick-and-mortar locations. answer.

Now, efforts have been made more

difficult by the entrance of innovative

12 Adams, John. “Why Great Mobile Payment Ideas Fail.”

American Banker Bank Technology News.

www.americanbanker.com, accessed March 1, 2015.

Payments on the go:

Making sense of the evolving mobile payments landscape 9

The increasing

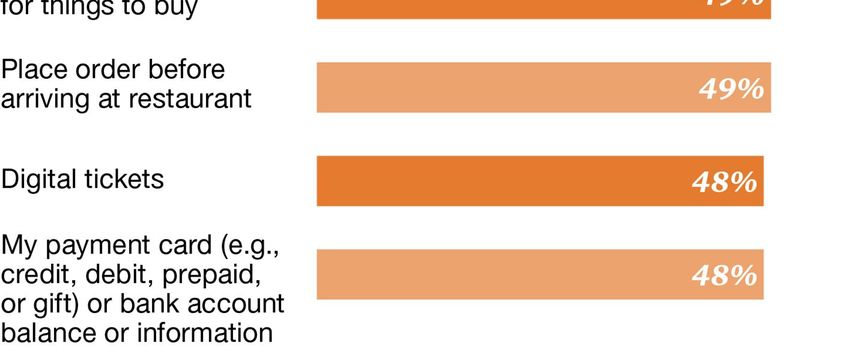

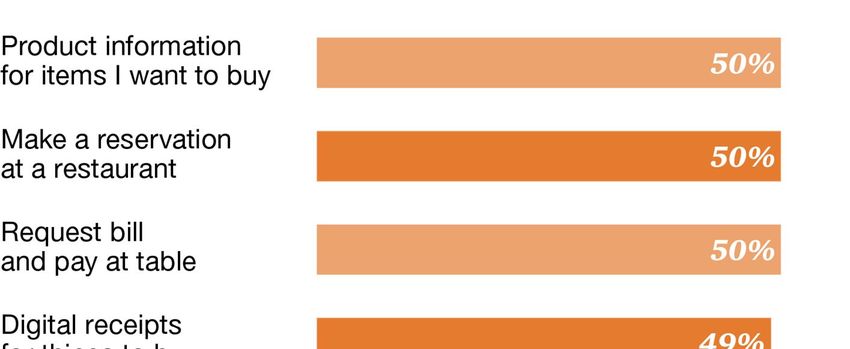

Figure 2: Consumers expect many services to be included in a mobile wallet.

importance of data

Another crucial aspect hovers over

the mobile payment ecosystem: the

importance of data revolving around

the transaction. It’s no longer a

discrete question of what was bought

and where. With data from many

mobile devices, merchants can now

unearth a variety of insights: whether

consumers are responding to a

promotion, or if they patronize a

particular establishment at a regular

time each day. Mobile payments

deliver more context about a

transaction than ever.

The availability of this data creates

challenges. Every participant in the

ecosystem understands the value of

data, but they’ve been forced to deal

with incomplete views. For instance,

merchants know how often

customers come in and what they

buy. They don’t know how often

customers shop at competitors,

though some card issuers and larger

processors do. Issuers, however, may

have visibility into the where but not

necessarily the what. Knowing this

information provides the ability to

digitally influence and measure sales.

As seen in Figure 3, analysts predict

that location-targeted mobile ad

spend in the US will triple between

Source: Forrester Research, “US mobile payments forecast, 2014 to 2019,” November 17, 2014.

2014 and 2018. Each participant in

the value chain—merchants, issuers,

The fundamentals of debit and credit which double as issuers and acquirers, processors, and carriers

transactions in and of themselves are networks. With mobile payments, alike—is scrambling to stake its

complex, too. The payments mobile phone manufacturers are claim.

ecosystem encompasses issuing and continuing to enter the fray—as

acquiring banks, networks (such as evidenced by Apple Pay and

Visa and MasterCard), processors Samsung Pay.

(First Data, Global Payments, and

others), merchants, and, of course,

consumers. The ecosystem is

muddied by players such as

American Express and Discover,

Payments on the go:

Making sense of the evolving mobile payments landscape 10Figure 3: Location-targeted mobile ad spend will triple between 2014 and 2018.

Source: BIA/Kelsey, “U.S. Local media forecast – mobile edition (2013-2018).”

The most salient underlying question That means mobile payment Merchant support, however, is only

for success lies in who controls the solutions must take into account the half the equation. Customers must be

relationship with the customer and, cost to merchants of new technology. willing to adopt new technologies.

therefore, who has access to Point-of-sale (POS) hardware and Experience shows that they will do so

transactional data. While other software can cost several thousand only when it is convenient, enhances

participants within the value chain dollars per checkout lane; even for a their overall experience, and makes

have a variety of views around national merchant getting a volume them feel confident that their

transactional data, only the merchant discount, that represents an financial information and transaction

has a direct relationship with the investment of millions of dollars.13 data are protected from fraud.

consumer—knowledge of who Joe And that’s just for POS hardware and Consumers took years to warm up to

Smith is, as well as what he is software: installation, credit and debit cards, only doing so

purchasing. Thus, any successful implementation, certification, and once they understood the

mobile payment solution must start back-end integration not included. convenience these cards provided,

with a strong foundation of merchant along with additional protections

support, and it must address A solution that requires significant through regulation. Customer

merchants’ concerns about potential financial investment without adoption of mobile payments will

fraud risks. providing a clear benefit to require new capabilities beyond the

merchants is likely to stall. But one status quo.

that helps them further solidify the

customer relationship—by extending

the transaction beyond the payment

into the associated realms of loyalty,

convenience, coupons, rebates, and

other tools—has a greater chance for

success.

13 CostHelper. “How Much Does a Point of Sale System

Cost?” http://smallbusiness.costhelper.com/point-of-

sale.html, accessed March 1, 2015.

Payments on the go:

Making sense of the evolving mobile payments landscape 11A snapshot of current technologies

Do the latest offerings meet our criteria? A look at four major competing solutions reveals their

strengths and limitations.

Solution and provider First launched Strengths Limitations

Apple Pay (Apple) October 2014 Has not attempted to supplant any Its NFC contactless technology is

player in the current ecosystem, only accessible to iPhone 6 users.

which has allowed Apple to create Disabled by some merchants

partnerships with ecosystem aligned with CurrentC.

participants.

Less than 3% of retailers currently

Uses a combination of tokenized support NFC on their POS

and biometric security. terminals. The October 2015 EMV

Strong consumer following. chip card compliance deadline will

inevitably expand the number of

compatible terminals as merchants

upgrade to newer systems.

Currently is not integrated with

merchant loyalty programs.

CurrentC (Merchant 2015 (scheduled) Uses QR codes and scanners Privacy concerns over CurrentC’s

Customer Exchange, or rather than NFC terminals. intentions to share purchasing data

MCX) Is device-agnostic and works with with developers, app stores, and

Android and iOS operating phone manufacturers may deter

systems. consumer adoption.14

Uses tokenized security. Requires multi-step payment

process: opening the app, and then

Points customers earn at one store scanning and confirming the codes.

are usable at others within the MCX

network.

Lower transaction fees for

merchants.

Google Wallet (Google) September 2011 Stores loyalty cards, gift cards, and Limited traction with mobile carriers

coupons. and merchants.

Allows funds transfer through Impact of February 2015 acquisition

Gmail. of Softcard unclear.

Works on hundreds of Android

phone models, arguably giving it

the broadest global reach.

Samsung Pay15 2015 (scheduled) Partnerships with major credit cards Available only on limited number of

and financial institutions. Samsung phones.

Proprietary security tokenization

technology called Magnetic Secure

Transmission.

Source: PwC analysis.

14 Constine, Josh. “CurrentC Is The Big Retailers’ Clunky Attempt To Kill Apple Pay And Credit Card Fees.” TechCrunch. http://techcrunch.com/2014/10/25/currentc/, accessed March 1, 2015.

15 Samsung Mobile Press. “Samsung Announces Samsung Pay, A Groundbreaking Mobile Payment Service.” www.samsungmobilepress.com, accessed March 15, 2015.

Payments on the go:

Making sense of the evolving mobile payments landscape 12The importance of OpenTable. Customers can use the At the same time, to spur merchant

customer experience app to search restaurants, make adoption, a payment solution must

reservations, and even pay for the accommodate the collection and

At the heart of many technology

meal (plus tip) at its conclusion. analysis of marketing and purchasing

solutions—especially those relating

Their rewards points are stored in data. Apps must link to back-end

to mobility—is the question of

the system for later use. The app can “commerce platforms” to track data

customer experience. It’s particularly

also e-mail receipts for expense about the customer, from which

important because smartphone apps

reimbursement. merchants derive benefits on an

give many enterprises direct access

ongoing basis. How frequently do

to customers they have never had Uber. In addition to ordering pick- customers visit? What do they

before, for example through indirect ups, customers can see the fees usually buy? Are there ways to use

selling or distribution models. How they’ll pay ahead of time. Because this information to cross-sell or up-

can enterprises make customer they pay with stored payment sell? How can this information be

interactions so smooth and credentials, there’s no back-and- used on a macro level to craft

frictionless that they become a forth with the driver at the end of the marketing campaigns that entice

competitive advantage, especially in ride. Customers can give feedback to similar demographics?

a digitized world where drivers, and vice versa.

differentiation is harder than ever to Merchants, in turn, can use the

achieve? The key point to remember: to spur information to offer discounts,

customer adoption, the transaction rebates, rewards, coupons, or other

Clearly, replacing an action as simple must be experience-driven, not enticements, essentially creating a

as the swipe of a magnetic strip (or device-driven. In fact, the best priceless loop of customer

soon, a chip-and-pin dip, tap, or transactional systems might just be engagement. Overall, mobile

wave) is not sufficient. Just as device-agnostic. If customers can payment solutions must serve both

merchants have to derive an choose from systems that help them these constituencies to succeed.

advantage in a mobile payment beat waiting for taxis or waiting in

solution, so do consumers. Some line for lunches or just generally save

app-based payment systems have time, they’ll be intrigued and

already been widely adopted by eventually enticed.

consumers, and those successes

highlight some key lessons that may

also apply to other payment

solutions:

Starbucks. Consumers benefit

because they can use the app to find

locations, order drinks for pick-up,

get product offers, and see

nutritional information. They can

pay for the transaction using a

scanned QR code, and do so with

stored payment credentials, taking

advantage of rewards points that can

be used at the time of purchase.

Payments on the go:

Making sense of the evolving mobile payments landscape 13What this means for your business

Why mobile payments Given all these interwoven can they do it in a way that retains—

must move beyond the dependencies, it’s important to and even expands, given the

transaction identify the overarching goal: to view increasing use of personal data—the

mobile payments not as a discrete trust that merchants and consumers

The apps used by Starbucks and

transaction but through the have in the system?

Uber offer a high level of customer perspective of the customer

service and intimacy, and represent Merchants. In the face of

relationship. It’s not the mobile

real value for the merchant and the complexity, merchants do not have

payment technology, per se; it’s the

customer alike. They solve a real opportunity to establish digital the luxury to remain on the sidelines

consumer problem in that they when it comes to mobile payment

engagement with customers. Ideally,

remove or reduce the friction in the solutions. Smartphones have become

that means deep engagement with

payment process. But they don’t loyal customers, as well as ways to extensions of our personas, and the

solve the overall mobile payment wallet is the most personal of

entice borderline loyalists and

conundrum simply because they personal possessions. Merchants

prospects, too.

represent high-frequency customer have an opportunity that cannot be

relationships. The mobile payment What will the future of wasted. They can actually sidestep

scenario for casual, infrequent mobile payments look the uproar over mobile payments

transactions still remains unsolved. like? and take advantage of the

There are no clear winners yet, and fragmentation by crafting their own

no clear recipes for success. The challenge for all the players in

branded, solution- and device-

this environment is complexity—the

agnostic options that extend the

That’s why we believe the mobile sheer spectrum of possibilities, from

intimate relationships they already

payment solutions market will creating one’s own app to figuring

have with customers.

remain fragmented, much as it is out how to integrate with various

now. New entrants will continue to offerings without setting up one-off, Furthermore, even as mobile

try to break into this market, and point-to-point solutions with each technology shines a bright light on

consumers will continue to choose participant. new ways to gather data, merchants

among multiple options when must maintain a grander perspective,

making purchases—cash, debit and Technology innovators. For

thinking about how to incorporate

credit cards, store cards, gift cards. providers in the payment value chain

information from multiple

(They will also retain these options to benefit from this turning point in

channels—mobile, web, in-store, and

as a backup for the unfortunate technology, they must work

more—into their customer

moment when their smartphone diligently to reduce complexity. They

engagement models. They must

battery dies and leaves them must figure out how they can retain

make sure they know that the Jane

temporarily impoverished.) Any new what makes the payment process

Smith who’s using a mobile device is

payment system must have a number work, while still creating ways to

the same Jane Smith who was sent a

of related attributes to be considered integrate advancements. How can

promotional ad 48 hours earlier and

successful: merchant acceptance, solution providers expose back-end who then went online to research

customer convenience, loyalty payment capabilities to

products 24 hours earlier. This

rewards, security, and privacy. accommodate whatever new

requires a sense of personalization

technologies might present and scale that may be new to many

themselves, and do so in a way that’s

merchants.

not only as plug-and-play as possible,

but as scalable as possible? And how

Payments on the go:

Making sense of the evolving mobile payments landscape 14At the same time, it will be critical to They may also need to make it easy Ultimately, the path forward for

navigate a regulatory and privacy for consumers to opt-out of data merchants does not solely revolve

landscape that is only partially collection at a later date. Merchants around the two options of either

defined and that will continue to will need to balance their desires to building an app or partnering with

evolve along with the ecosystem. completely control the experience one of the existing mobile payment

Today, consumers typically will against potential consumer backlash providers. Rather, it needs to address

accept an application’s terms of use over privacy rights. multiple strategies targeted at

when they download it, ceding gaining a stronger understanding of

control of how the data is used. In No matter what happens with digital technologies and their

the future, regulators may create regulations, merchants and others potential for improving customer

laws that align this “opt-in” model must be willing and able to answer engagement. Those who want to

with existing laws for the sharing of consumers’ questions about how plant the stake of success in this new

financial services data. This means their data will be used, disseminated, territory must start formulating their

that app developers may have to and purged. As a result, merchants plans now.

separate a consumer’s ability to use and others should design

an app from his or her permission to applications with these future

share data. capabilities in mind.

For a deeper conversation, please contact:

Payments A publication of PwC’s

Retail & Consumer Financial Services Institute

Andrew Luca Phil Bloodworth Marie Carr

andrew.j.luca@us.pwc.com phil.bloodworth@us.pwc.com Partner

(646) 335 4649 (214) 754 7919 Cathryn Marsh

Director

Gregory Holmes PJ Ritters Emily Dunn

gregory.holmes@us.pwc.com paul.j.ritters@us.pwc.com Senior Manager

(415) 498 7435 (612) 596 6356 Kristen Grigorescu

Senior Manager

Nathan Hilt Bryan Oberlander

nathan.hilt@us.pwc.com bryan.s.oberlander@us.pwc.com

(415) 498 8074 (617) 530 4125

Scott Bauer

scott.d.bauer@us.pwc.com

(678) 419 1128

About our Financial Services practice

PwC’s people come together with one purpose: to build trust in society and solve important problems.

PwC serves multinational financial institutions across banking and capital markets, insurance, asset management, hedge funds,

private equity, payments, and financial technology.

As a result, PwC has the extensive experience needed to advise on the portfolio of business issues that affect the industry, and we

apply that knowledge to our clients’ individual circumstances. We help address business issues from client impact to product design,

and from go-to-market strategy to human capital, across all dimensions of the organization.

PwC US helps organizations and individuals create the value they’re looking for. We’re a member of the PwC network of firms in 157

countries with more than 195,000 people. We’re committed to delivering quality in assurance, tax, and advisory services.

Gain customized access to our insights by downloading our thought leadership app: PwC’s 365™ Advancing business thinking

every day.

Follow us on Twitter @PwC_US_FinSrvcs

Payments on the go:

Making sense of the evolving mobile payments landscape 15Contatti Marco Folcia Gianluca Meardi marco.folcia@it.pwc.com gianluca.meardi@it.pwc.com (02) 66720433 (02) 66720396 “Payments on the go: Making sense of the evolving mobile payments landscape,” PwC, June 2015, www.pwc.com/fsi © 2015 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. PwC US refers to the United States member firm, and PwC may refer to either the PwC network of firms or the US member firm. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Puoi anche leggere