Operating Model October 26th, 2017 - Launch of a new functionality: Additional Intraday Margin with securities

←

→

Trascrizione del contenuto della pagina

Se il tuo browser non visualizza correttamente la pagina, ti preghiamo di leggere il contenuto della pagina quaggiù

Operating Model

October 26th, 2017

Launch of a new functionality: Additional Intraday Margin

with securities

Segue versione in Italiano

Functionality’s details

• Intraday Margin Calls payable with securities will be only the ones received after a specified time (after

2:00 pm);

• The functionality will be activated the first day of the month after the explicit request by Clearing Members

and will be effective until revocation;

• The functionality will be subject to a monthly fee;

• The Clearing Member who adheres to the functionality:

o will be able to choose 2 ISIN for each Intraday Margin Call. The list of eligible ISIN will be available

on ICWS;

o will send to CC&G by email the ISIN codes that he wants to deposit as well as the information

needed for the valorization of the collateral. The information required will be provided in the

Annexes to the Instructions;

o if he will deposit securities that may not be considered eligible partially or totally (for example

because of non-compliance with concentration limits) he will have to pay the uncovered amount

with cash. Such amount should be made available on his own PM Account of Target 2 or in the

account of his Settlement Agent in order to allow CC&G to collect it by direct debit. Financial

instruments not included in the list of eligible securities on ICWS will be returned.

• CC&G:

o will indicate alongside the notification of Intraday Margin Call also the term, which shall not be less

than thirty minutes, for the deposit of securities and the term for the deposit of cash if the amount

of the financial instruments does not cover totally the Intraday Margin Call.

o will communicate to the Clearing Member if the Intraday Margin Call has been successfully

covered or if an additional cash amount is necessary.

o will revoke the possibility to cover Intraday Margin Call with securities to the Participants who

deposit instruments not sufficient or unfit to cover Margin Calls for a number of times greater than

the thresholds reported in the Annexes to the Instructions.

Operating Model

October 26th, 2017

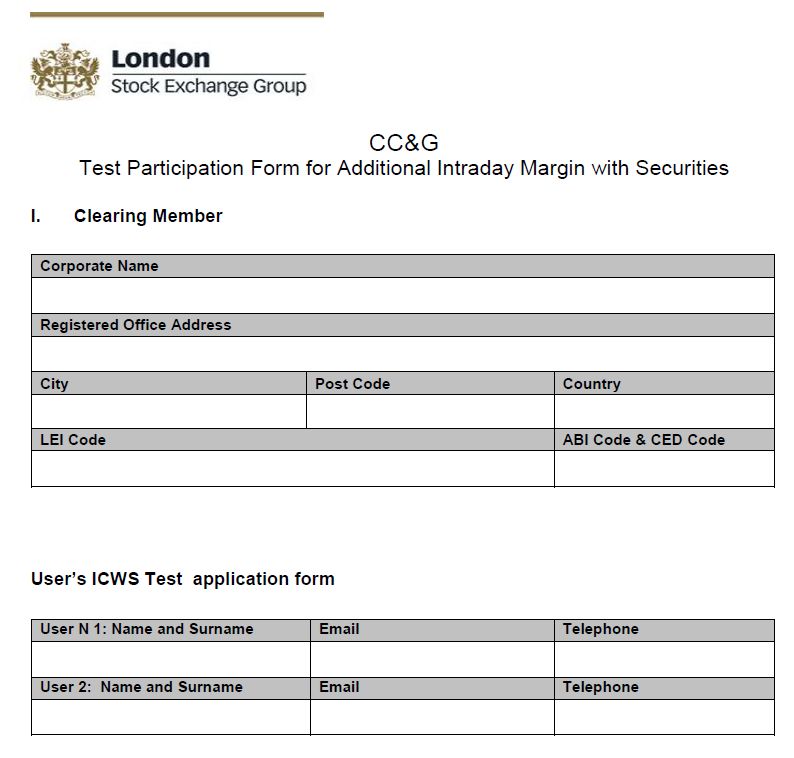

How to take part in the test

In order to take part in the execution of the tests and to receive the credentials needed to access to the ICWS Test

Environment, it is necessary to fill the attached module. This module shall be sent to client.services@lseg.com

with the following object: “Test CCP Intraday Margin in Securities”.

Reports

The reporting will remain unchanged for the Clearing Members who do not adhere to the functionality and for

Intraday Margin Calls payable only in cash (received by Clearing Members before the time reported in the point 1 of

the paragraph “Functionality’s details”).

Clearing Members who adhere to the new functionality will receive, in case of Intraday Margin Calls after the time

indicated above, a new set of reports:

1) Report MS31: the report will indicate the Intraday Margin Call amounts, the time-limit for securities

collateral deposit and the time-limit for the direct debit in cash in case of insufficient coverage with

securities collateral;

2) Report MS32: the report will indicate if the securities deposited as collateral cover or not the Intraday

Margin Call. Whether the collateral is not sufficient to cover the intraday call the report will indicate also the

amount to be paid in cash and the debit time;

3) Report MI01: the report will show the intraday margin amount, the amount and composition of collateral

(cash and securities) that the Participant has at CC&G at the moment of the Intraday Margin Call;

4) Report MI02: the report will have the same structure of the current MA03. The report will provide the

details of the Government Securities deposited by the Clearing Member into each account showing the

related amount, the haircut applied and the concentration limits (total limit and country limit). CC&G will

send this report any time an Intraday Margin Call is trigger as well as each time the Clearing Member will

deposit securities to cover such Intraday Margin Call;

5) Report MS35: currently CC&G sends the report MS35 to the Settlement Agent on behalf of the Clearing

Members for whom it operates. CC&G added some information to this report in order to inform the

Settlement Agent that the Clearing Member has received an Intraday Margin Call and that such Clearing

Member could cover it with securities. Moreover, the file includes the information about the Maximum

Potential Amount payable that the Settlement Agent would be debited if the securities posted as collateral

are not sufficient to cover the intraday margin call amount, as well as the actual amount requested if the

securities posted as collateral are not sufficient to cover the intraday.

The reports will be available on CC&G’s website in the Technical Manual.Operating Model

October 26th, 2017

Data Service

The Data Service will be integrated for this new functionality:

1) D21E: this file will have the same structure of the D21A which contains information regarding the requested

integration of Margins to Clearing Members. Compared to the D21A the new file will contain a new field

“Intraday Coverage with securities”. D21A and D21E will be generated in parallel for six months. After six

months the file D21E will replace the D21A. In particular the D21E will be denominated D21A and the

current D21A will cease to be produced.

2) D21D: this file will be sent to the Settlement Agent on behalf of the Clearing Members for whom it operates

if the Clearing Member requires covering Intraday Margin Call with securities. It will have the same

structure of the file D21C. Compared to the D21C the D21D will include the field “Max Potential Amount”

which represents the maximum potential amount that the Settlement Agent would be debited if the

securities posted as collateral are not sufficient to cover the intraday margin call amount.

For any additional information please contact:

Clearing operations

Tel. +39.06.32395.303

e-mail: clearing.settlement@ccg.com

Post Trade Sales

tel. +39 02 33635283

e-mail: pt.sales@lseg.com

Risk Management

tel. +39.06.32395.444

e-mail: rm.group@lseg.com

Membership

Tel. +39.02.7242.6501

e-mail: client.services@lseg.comOperating Model October 26th, 2017

Modello Operativo

26 ottobre 2017

Avvio della funzionalità di Copertura richieste di margini

aggiuntivi infragiornalieri in Titoli

Modello di funzionalità

Potranno essere coperte in titoli soltanto le richieste intraday effettuate dopo un determinato orario

(oltre le ore 14:00);

La funzionalità viene attivata il primo giorno del mese successivo a quello di richiesta del

Partecipante Diretto , sarà efficace fino a revoca e sarà soggetta ad una commissione mensile;

Il Partecipante Diretto che ha aderito alla funzionalità:

o può scegliere al massimo 2 ISIN per ogni richiesta tra quelli presenti in una lista consultabile in

ICWS;

o invierà a CC&G con un’apposita comunicazione via email i codici ISIN dei titoli che intende

depositare e le informanzioni necessarie alla valorizzazione della garanzia. Le informazioni

richieste saranno previste negli Allegati alle Istruzioni;

o nel caso in cui abbia depositato titoli non utilizzabili in tutto o in parte (per esempio a causa del

mancato rispetto limiti di concentrazione), sarà tenuto al versamento in contante della parte

rimasta scoperta rendendo disponibile tale ammontare sul proprio conto PM in Target2 o in quello

del suo eventuale Agente di Regolamento, consentendo così a CC&G di prelevarlo mediante

addebito diretto. I titoli non censiti nella lista riportata nel file in ICWS precedentemente citato

saranno restituiti;

CC&G:

o indicherà contestualmente alla richiesta il termine, non inferiore a 30 minuti, per il deposito dei

titoli e il termine per la copertura in contante dovuto dal Partecipante Diretto qualora il

controvalore utile dei titoli depositati non copra, in tutto o in parte, l’ammontare dei Margini

richiesti;

o una volta acquisiti i titoli invierà il riscontro della totale copertura dei Margini richiesti o, in caso di

parziale copertuta, l’ammontare che sarà addebitato in contante;

o revocherà la possibilità di coprire i Margini Infragiornalieri in titoli ai Partecipanti che depositano

titoli insufficienti o non idonei per un numero di volte superiore ai parametri e alle soglie che

saranno indicate negli Allegati.Modello Operativo

26 ottobre 2017

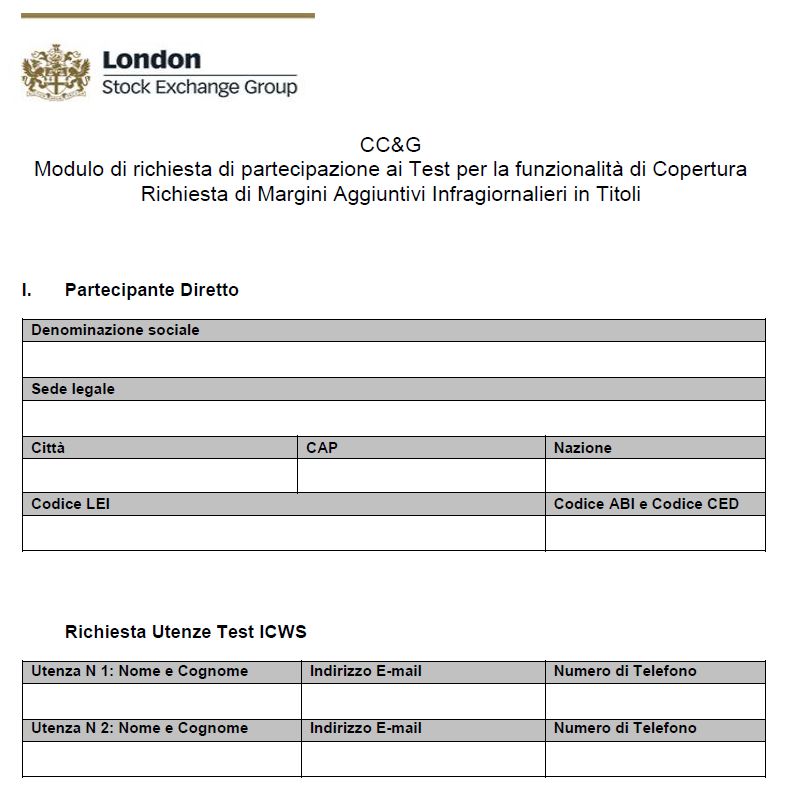

Modello di Partecipazione ai test

Per partecipare allo svolgimento dei test e richiedere le utenze per l’ambiente di Test occorre completare

il modulo allegato che dovrà essere inviato all’indirizzo e-mail client.services@lseg.com, citando in

oggetto “TEST CCP Copertura richieste di margini aggiuntivi infragiornalieri in Titoli”.

Reportistica

La reportistica non subirà modifiche per i Partecipanti che non aderiscono alla funzionalità in oggetto e

per le richieste Intraday pagabili solo in cash (antecedenti quindi all’orario riportato al punto 1 del

precedente paragrafo).

I Partecipanti Diretti che aderiranno alla funzionalità riceveranno invece, in caso di Richieste Intraday

successive all’orario precedentemente indicato, un nuovo set di report:

1) Report MS31: il report indicherà l’ammontare della richiesta intraday, il termine per il deposito

degli strumenti finanziari ed il termine dell’addebito in contante in caso di parziale copertura in

strumenti finanziari;

2) Report MS32: il report indicherà al partecipante se i titoli depositati a copertura degli intraday

sono sufficienti a coprire i margini infragiornalieri. Se non sufficienti il Report indicherà

l’ammontare scoperto da versare in cash e il termine dell’orario di addebito;

3) Report MI01: il report indicherà l’ammontare dei margini iniziali ricalcolati intraday, l’ammontare

delle garanzie e la composizione delle stesse (cash e titoli) che il Partecipante Diretto ha presso

CC&G al momento della richiesta intraday;

4) Report MI02: avrà lo stesso formato del report giornaliero MA03. Riporterà nel dettaglio il valore

del collateral depositato dal Partecipante Diretto, l’haircut applicato su ciascun titolo depositato a

collateral e i limiti di concentrazione (limite totale e limite paese). Il report sarà inviato

contestulamente alla richiesta intraday ed ogni volta che verranno acquisiti i titoli a copertura

degli intraday. In questo modo il Partecipante Diretto conoscerà immediatamente il nuovo

ammontare delle garanzie;

5) Report MS35: questo report viene già inviato alle banche Agenti del Regolamento. CC&G ha

apportato delle modifiche al fine di informare la banca Agente del Regolamento se il Partecipante

per il quale presta il servizio è soggetto ad una richiesta intraday copribile in titoli e in tal caso

l’ammontare potenziale massimo che la Banca Agente del Regolamento potrebbe essere tenuta

a versare, nonché al termine del periodo di copertura in titoli, se è richiesta una copertura in

contante o meno.

I report saranno disponibili nei prossimi giorni sul Manuale Tecnico disponibile sul sito web.Modello Operativo

26 ottobre 2017

Flussi

I flussi, così come la reportistica, sono stati integrati per tener conto della nuova funzionalità. In

particolare:

1) D21E: rispetto al flusso D21A verrà aggiunto un campo in coda al tracciato: “Intraday Coverage

with securities”. Questo flusso verrà prodotto in parallelo al D21A per 6 mesi; trascorsi questi

mesi il D21E verrà denominato D21A e il D21A attualmente vigente non verrà più prodotto.

2) D21D: questo flusso verrà prodotto ed inviato alle Banche Agenti del Regolamento che prestano

la funzionalità per Partecipanti colpiti da una Richiesta Intraday pagabile in titoli. Avrà lo stesso

formato del D21C. Rispetto a quest’ultimo riporterà il campo “Max Potential Amount”

rappresentante l’ammontare massimo potenziale che la banca Agente del Regolamento sarà

tenuta a versare qualora i titoli coprano parzialmente la richiesta intraday.

Per ogni ulteriore informazione contattare:

Clearing operations

Tel. +39.06.32395.303

e-mail: clearing.settlement@ccg.com

Post Trade Sales

tel. +39 02 33635283

e-mail: pt.sales@lseg.com

Risk Management

tel. +39.06.32395.444

e-mail: rm.group@lseg.com

Membership

Tel. +39.02.7242.6501

e-mail: client.services@lseg.comModello Operativo 26 ottobre 2017 ALLEGATO

Puoi anche leggere