Assemblea Cosmetica Italia

←

→

Trascrizione del contenuto della pagina

Se il tuo browser non visualizza correttamente la pagina, ti preghiamo di leggere il contenuto della pagina quaggiù

Assemblea Cosmetica Italia FRANCESCO CAVONE Director, Offering Suppliers & Consumer Health, Italy © 2019. All rights reserved. IQVIA® is a registered trademark of IQVIA Inc. in the United States, the European Union, and various other countries.

AGENDA + IQVIA CONSUMER HEALTH + SCENARIO DEL MERCATO IN FARMACIA + PRINCIPALI FATTORI DI CAMBIAMENTO + I NUMERI DELL’E-COMMERCE

3

Driving consumer healthcare from Concept to Consumer Global end-to-end capabilities Copyright © 2019 IQVIA. All rights reserved. 4

Il mercato italiano in farmacia

Il mercato perde 1% a valore, ma con comportamenti opposti tra i

comparti «etico» e «consumer», anche se nell’ultimo MAT si

registra un rallentamento

Totale mercato 4%

MAGGIORE COMPETITIVITÀ

Variazione%

€ 24,3 Mld

3 anni

+ Nuove aperture

▼ -1,0% a valore 3%

+ Nuovi canali (online)

▼ -2,1% a unità

CONSUMER* + Sviluppo catene

2%

+ Crescita del commerciale

€ 10,0 mld

1% ESIGENZE DEL CONSUMATORE

ultimo anno ▲ +0,3%

ultimi 3 anni ▲ +1,1% + Più informato ed esigente

0%

-3% -2% -1% 0% 1% 2% 3% + Decisione più «fluida»

Variazione% + Benessere e non solo cura

1 anno

-1%

ETICO

DINAMICHE DI MERCATO

€ 14,3 mld

-2%

+ Riduzione valore «generici»

ultimo anno ▼-1,8% + Switch su canale non-retail

ultimi 3 anni ▼-2,6%

-3%

+ Concentrazione dei

distributori

-4%

Fonte: IQVIA Multichannel MAT 10/19 (eur/pub) in farmacia

Copyright © 2019 IQVIA. All rights reserved.

* Consumer = commerciale + autocura

6

Il comparto OTC ed in particolare gli integratori guidano la

crescita del commerciale, mentre parafarmaco e nutrizionale

sono sempre meno presenti

Totale mercato 5%

Variazione%

€ 10,0 Mld

3 anni

4%

▲ +0,3% a valore

▼ -1,8% a unità

3%

OTC Automed; OTC INTEGRATORI;

-0,1%; 2%

PEC; 3,1%;

1,1%; 0,7%; 3,7%;

2.259 k€ 1% 0,7%; 3.805 k€

1.973 k€

0%

-6% -4% -2% 0% 2% 4% 6%

PARAFARMACO; Variazione%

-4,4%; -1%

1 anno

-3,0%;

1.618 k€ NUT; -2%

-4,2%;

-2,7%;

387 k€ -3%

-4%

-5%

* PEC = Personal Care

Fonte: IQVIA Multichannel MAT 10/19 (eur/pub) in farmacia

Copyright © 2019 IQVIA. All rights reserved. 7

Focus comparto PEC (Personal Care): crescono solo i prodotti

bellezza in farmacia e corner

Peso e trend 1 anno nei 3 canali Peso sul comparto NEC2 coverage 80%

-1% -5% 2% 0%

PGP

-4% -7% -1% -1% 0%

BELLEZZA 52%

-5% -6% 3% -4%

11% 6% 12%

-10%

25% 11%

11% 9% IGIENE

83% -20%

PERSONALE 30%

79% 79%

7%

68%

Peso

-30%

ACCESSORI 13%

-40%

-50%

BAMBINI 5%

ACCESSORI BAMBINI BELLEZZA IGIENE

-60%

PERSONALE

Farmacia Paraf Corner

Copyright © 2019 IQVIA. All rights reserved. 8

Fonte: IQVIA Multichannel MAT 10/19 (eur/pub) in farmacia

La crescita del comparto PEC in Europa ha rallentato negli ultimi

due anni, registrando comunque un trend stabile e positivo

Europe PEC Market Size and Yearly Growth

4%

3%

0% 1%

6.953 7.153 7.161 7.215

6.672

2015 2016 2017 2018 2019

Market Size (LEU mn) Y-o-Y Growth

Copyright © 2019 IQVIA. All rights reserved. 10

I Paesi CEE (Repubblica Ceca, Ungheria e Croazia) crescono più

rapidamente, mentre Paesi come l’Italia e la Svizzera mostrano un

calo sia nel breve che nel medio termine

EUROPE PEC Growth by Country: Long vs Short Term

EUROPE Latest Year growth 10

+0,8%

Greece Hungary

8

Portugal

Czech Republic

6

Poland Slovakia

Croatia

4

Belgium

Spain

Switzerland

2

Austria

0

-3 -1 1 3 5 7 9 11 13

EUROPE 3 Year Average growth

Italy -2 Germany +1,2%

France

-4

-6

Copyright © 2019 IQVIA. All rights reserved. 11Il numero di abitanti per farmacia si è ridotto del 7% in 3 anni, il

fenomeno delle nuove aperture è in controtendenza rispetto

all’Europa

In Europa fenomeno inverso all’Italia

Popolazione (.000 abitanti)

65.850 60.340 60.626 59.394 59.685 60.783 60.796 60.666 60.589 60.484 60.360

Thousands

55.850

45.850

35.850

25.850

15.850

5.850

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

22000 3.700

Abitanti per f.cia # Farmacie

21500

3.452

3.401 3.500

21000

20500

3.300

20000

3.163

19500 3.100

19000

19.082

2.900

18500

18000

17.481

17.874

2.700

17500

17000 2.500

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Copyright © 2019 IQVIA. All rights reserved. Fonte: IQVIA Analysis Ago19 12In Italia la distribuzione risente del calo del mercato con elevata

polverizzazione di quote, mentre il Europa c’è maggiore

concentrazione

Top3 grossisti in Europa I distributori in Italia nell’ultimo decennio

Var 3 anni

16%

14%

2008

Top5;

12% Spain; 59,8% 45%

10%

8%

Germany; Top10;

Belgium; 6% 63,5% 57%

Austria; 83,9%

71,9%

4%

2%

Top5;

0%

-2% -1% 0% 1% 2% 3% 4% 56%

2019

-2% Var 1 anno

Italy; 40,2%

-4%

Mercato retail 2018 Germania Spagna Austria Belgio Italia

Top10;

Variazione ultimo anno 4,2% 1,1% 4,4% -0,9% -1,0% 80%

Variazione 3 anni 3,7% 2,0% 5,3% -0,7% -1,1%

Copyright © 2019 IQVIA. All rights reserved. 13Modelli e principali catene presenti in Italia

INTERNATIONAL GROUPS NATIONAL WHOLESALERS

INVESTMENT FUNDS NETWORK OF SPECIALIZED BRAND

VIRTUAL CHAIN REAL CHAIN

Copyright © 2019 IQVIA. All rights reserved. Source: IQVIA analysis and #PoS estimation 14…analizzando i dati, Nulla (o quasi) è cambiato dall’entrata in

vigore del DDL concorrenza…

0

0

9 /20

16 8/2017 0

9/2019

Copyright © 2019 IQVIA. All rights reserved. 15…il peso delle catene sul totale mercato a valore è del 14% in

ponderata e 13% in numerica

Reali

Virtuali forti

Virtuali light

Focus Chains

Indipendenti

Focus Virtual Chains

Focus Independents

69%

Indip

85%

18%

11% Chain

14%

2%

Copyright © 2019 IQVIA. All rights reserved. 16Cambia la visione se osserviamo il fenomeno con la lente puntata su aree geografiche con presenza di catene organizzate Copyright © 2019 IQVIA. All rights reserved. 17

I numeri dell’eCommerce

Il caso Amazon

Gen/18 Cosa può fare Alexa I clienti (pazienti) hanno poco tempo, non possono perdere

oggi…

un assistente medico tempo a cercare prodotti (medicinali) e fare la fila.

personale? I prodotti stessi devono raggiungere il cliente (paziente) e

Feb/18

devono essere il più comodi possibile!

Giu/18

Amazon ha brevettato un

sistema di consegna

Lug/18 basato su droni

Set/18 Amazon è in fase di test

con 6 Robot Scout nella

Ott/19 periferia di Washington

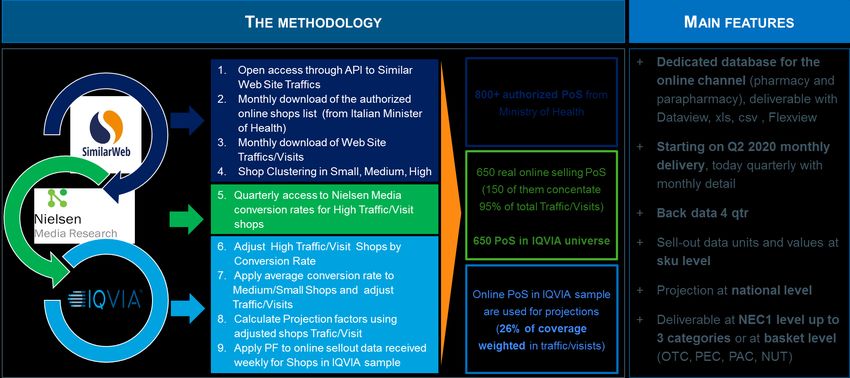

Copyright © 2019 IQVIA. All rights reserved. 19Alto potenziale per il canale eCommerce, ma lo scenario è ancora

molto frammentato

1. PRODUCT CATEGORIES 2. DELIVERING TYPE 3. TYPE OF SITES

•

Which product categories could be sell

Which type of delivery? Which websites?

online?

+ RX: Italian legislation doesn’t allow + Click & Collect: no + Portals: out of scope

+ OTC: Self-Medication products need ministerial + Pick & Pay: no + Pharmacy/para website: in scope

authorization + Delivery at home: yes

+ Consumer: everyone can sell at any price

General Specialized PoS Pure online Omni Market concentration

portals portals website channel

No. of Players with

90% Value Share 800+

Portals Pharmacies & Parapharmacies

Portals Brand or product PoS with their No brick and Chain web

category portals own website mortar portals

150

IQVIA scope

Copyright © 2019 IQVIA. All rights reserved. 20Una metodologia innovative per gestire l’espansione del canale a livello nazionale Copyright © 2019 IQVIA. All rights reserved. 21

Crescita a doppia cifra e forte concentrazione in categorie e line

di prodotto

Copyright © 2019 IQVIA.

Copyright All IQVIA.

© 2019 rights reserved.

All rights reserved. 22Le 5 principali categorie coprono oltre il 60% del canale

Il canale online per comparti Top5 NEC1 e principali prodotti

11%

89%

Auto-

Integratori 62% 66%

OTC Med

04-Vitamine, 10-App

03-App intestinale 12-Urologia 02-Analgesici

minerali circolatorio

30% 91%

PEC

82-Bellezza 83-Bellezza 85-Igiene

86-Capelli 93-Cavo orale

femmin. unisex personale

5% 64%

PAC

56-Strum 58- 57-Acces.

52-Incontinenza 54-Infanzia

medic/chir Ortop./Reumatici Medico/Chirurg.

3% 94%

NUT

30-Nutrizione 36-Alimenti per 35-Dietetici

34-Dimagranti 32-Senza glutine

enterale adulti infanzia

Copyright © 2019 IQVIA. All rights reserved. 23Comportamento dei Top10 produttori nel comparto PEC

valore canale online MAT 09/19 66,4 mln€

Online Top10 Manufacturer Online Top products ppg 6mth Online new products

140%

TRUDY BB CARE M/L -51%

%PPG 6mth

Top8 ANTHELIOS XL

ORAL B DENT.FLOSS -53%

120%

DERMON DOCCIA SCH. 7%

100%

Top3 SAUGELLA… 9%

DEFENCE SUN

ELMEX DENT. 0%

80% Top5

MUSTELA BEBE 11%

60% EUCERIN PH5 6%

RILASTIL S S

ALOEVERA 2 32%

Top10

40%

Top6

KEOPS DEODORANTE 60%

Top4 Top1 EUPHIDRA AMIDO MIO 28%

20%

Top9 SOMATOLINE

MINERAL 89 36% COSMET

0% CERAVE 32%

0% 1% 2% 3% 4% 5% 6% 7% 8%

NUXE HUILE PRODIGI 97%

-20% BIOCOLLAGENIX

Top7 Top2 ANNURMETS HAIR 30%

BIOSCALIN PHYSIOG. -8%

-40% %Market Share

Copyright © 2019 IQVIA.

Copyright All IQVIA.

© 2019 All rights reserved.Fonte:

rights reserved. IQVIA DW eCommerce 24Da un servizio di “audit” ad un servizio integrato di “analisi

combinata” del canale online

OGGI SVILUPPI FUTURI

+800 150 +32.000

Top PoS in the

Authorized PoS references

online market

eCommerce

Promo

ad hoc project

144 mln 26% 38 mln analysis and

channel

as PMR Projects

IQVIA sample annual traffic in «nominative e-

annual traffic integration

(views) IQVIA sample data»

Integration

offline and

13 mln 41% 5,3 mln online Consulting &

IQVIA sample annual purchases channels Services

annual purchases (Multichannel, Projects

(conversion rate) in IQVIA sample

Pharmatrend,

Weekly Trend)

220 mln€ 17 mln +34%

estimated units sold

turnover in 2019 online %PPG 1y (Giu19)

Copyright © 2019 IQVIA.

Copyright All IQVIA.

© 2019 rights reserved.

All rights reserved. 25iqviaconsumerhealth.com

linkedin.com/showcase/iqvia-consumer-health/

www.IQVIA.com

IQVIA Italia

IQVIA_ITALIA

©2018 IQVIA All rights reserved. This document and the information herein contained are CONFIDENTIAL and PROPRIETARY and

cannot be disclosed to third parties without IQVIA’s written permission. No part of this document and the information herein contained

may be reproduced, stored in back-up systems or transmitted in any form or by any mean without IQVIA’s prior written consent. 26Puoi anche leggere