IL MERCATO UNICO DIGITALE EUROPEO: UNA STRADA NON ANCORA PRESA ?

←

→

Trascrizione del contenuto della pagina

Se il tuo browser non visualizza correttamente la pagina, ti preghiamo di leggere il contenuto della pagina quaggiù

GRUPPO TELECOM

Università ITALIA

di Urbino

22 Novembre 2016

Urbino, 22 novembre 2016

IL MERCATO UNICO DIGITALE EUROPEO:

UNA STRADA NON ANCORA PRESA ?

Lorenzo Pupillo, TIM *

NON ANCORA PRESA ? *

Lorenzo Pupillo*

Regulatory Affairs and Equivalence

*I contenuti di seguito presentati rappresentano solo il punto di vista dell’autore e non coinvolgono TIM

MERCATO

..difficoltà per chi vende

per chi acquista ……

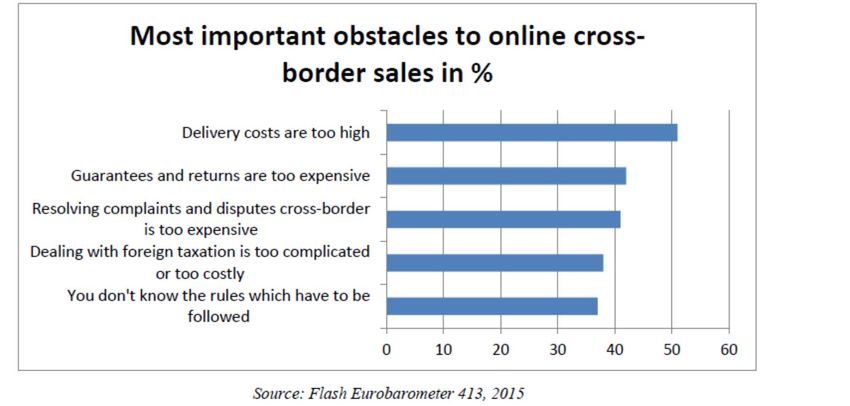

Le preoccupazioni maggiori di chi acquista da un paese all’altro sono: costi di

spedizione (27%), costi di rispedizione (24%), tempi di consegna (23%) etc.

UNICO Fattori di scala 500 milioni di abitanti rispetto ai 320 milioni degli USA Un impatto sul GDP Europeo di 415 miliardi di euro (European Parliament Research Service 2015) Il digitale permette di raggiungere grandi numeri di clienti potenziali ( MICRO‐ MULTINAZIONALE!!) AMAZON as DIGITAL UTILITY

DIGITALE 1/2 L’economia digitale coinvolge oggi molte industrie e settori: le telecomunicazioni, il commercio, la finanza e le assicurazioni, i media, i trasporti, la sanità, l’energia , il settore alberghiero , l’istruzione, etc. L’economia digitale si caratterizza per molte delle proprietà dell’economia tradizionale ( economie di scala e di scopo, - alti costi fissi e costi marginali vicino allo zero- esternalità di rete, mercati a più versanti), ma con un’accentuazione molto più spinta di queste caratteristiche ( si pensi alla combinazione della presenza di esternalità di rete sia dal lato della domanda che da quella dell’offerta che porta molto spesso al modello «the winner takes all!) Ma l’economia digitale si caratterizza anche per nuove proprietà come l’economics of attention, cioè per l’abbondanza piuttosto che per la scarsità di informazioni. Questo implica che come dice il premio nobel Herbert Simon « A wealth of information creates a poverty of attention» e che di conseguenza il ruolo degli aggregatori di informazione e il consenso informato dei consumatori nelle transazioni acquista un valore centrale con tutte le conseguenze sui temi dell’aggregazione dei dati, del trust, della profilazione ,etc

DIGITALE 2/2 E’ evidente quindi che, pur potendo dire che i cambiamenti caratterizzano oggi più la tecnologia che le leggi economiche è necessario evidenziare la necessità che sia la regolamentazione che le norme antitrust affrontino in modo differente l’economia digitale rispetto a quanto fatto fino ad oggi. Le piattaforme che si caratterizzano per definizione come mercati ad almeno due versanti e che quindi implicano scelte di produzione e di prezzo congiunte tra i due versanti, richiedono, per esempio, che l’antitrust analizzi i due versanti simultaneamente, altrimenti è facile arrivare a conclusioni sbagliate. I mercati dell’ICTs si caratterizzano in modo distintivo rispetto ai mercati dei prodotti tradizionali molto più vicini alle commodity. L’ecosistema digitale si caratterizza soprattutto per: a) modularità ( i prodotti e i servizi digitali sono basati sulla combinazione di input complementari come applicazioni, contenuti e apparati), b) forti esternalità di rete sia dal lato della domanda che da quello dell’offerta, che comportano una crescita veloce dei mercati e della presenza di imprese leader in essi; c) competizione dinamica ( le imprese competono soprattutto nell’innovazione di prodotto, nell’ingresso e nella creazione di nuovi mercati e nell’uso di nuove tecnologie per l’offerta di servizi esistenti ma a prezzi più bassi). Tutto questo, molto spesso comporta una concorrenza NON NEL MERCATO (Esistente) ma PER IL MERCATO (completamente nuovo). Le regole antitrust, quindi devono tener presente queste caratteristiche. La complessità degli ecosistemi digitali aumenta l’incertezza regolatoria, rende più difficile da parte dei regolatori la valutazione delle performance del mercato e l’individuazione di soluzioni, rendendo la regolamentazione esistente obsoleta.

Servizi di telecomunicazioni ..anni ‘’90 !!!!

L’ ECOSISTEMA DI INTERNET DI OGGI !!!! Fonte: A.T. Kearney analysis “A Viable Future Model for the Internet”

Telecom Single (Internal) Market: una idea che

viene da lontano… 1/2

1998: Primo Pacchetto Telecom: liberalizzazione dei servizi di

telecomunicazione e misure di armonizzazione per la creazione di un

Telecom Single market

Controllo dei prezzi al dettaglio

Obblighi sul Servizio Universale

Controllo dei prezzi all’accesso ( Direttiva sull’Interconnessione, ULL, etc)

Sviluppo di una competizione basata sui servizi e non sulle

infrastrutture

Telecom Single (Internal) Market: una idea che viene da

lontano… 2/2

2002: Secondo Pacchetto : quadro complessivo di misure per rafforzare la

concorrenza e far sviluppare le infrastrutture.

5 Direttive ( Framework , Authorization, Access, Universal Service,

ePrivacy )

Introduzione dello schema: 1) Analisi del mercato; 2)identificazione della posizione

dominante; 3) definizione dei rimedi

Identificazione di 18 mercati rilevanti candidati alla regolamentazione ex-ante

2009: Terzo Pacchetto:

Regolamenti sul Roaming ( 2007, 2009)

Creazione del Body of European Regulators for Electronic Communications (BEREC)

Fase 2 sui rimedi. ( Maggiore pressione da parte della Commissione ma no veto power)

Spettro: Neutralità tecnologica e di servizio e spectrum trading and sharingIL TELECOM SINGLE MARKET …NON ESISTE

(ANCORA ) !!!

2007 : La Commissaria per l’Information Society Viviane Reading « Two

decades after we started to open national markets formerly dominated by

state owned monopolies, to competition, we still do not have an internal

market for telecoms «

2010 : La nuova Commissaria per l’agenda digitale , Neelie Kroes al Mobile

World Congress . « Europe is still a patchwork of national markets . We no

longer have queues of lorries at frontiers but we are still very far from

achieving a Digital Single Market»IL TELECOM SINGLE MARKET …NON ESISTE ANCORA !!!

ENORMI DIFFERENZE DI PREZZO TRA I SERVIZI

Fonte : Pelkmans & Renda 2011IL TELECOM SINGLE MARKET …NON ESISTE ANCORA !!!

A BROADBAND DIVIDE : ENORMI DIFFERENZE NELL’OFFERTA DI SERVIZI

A LARGA BANDA

Fonte : Pelkmans & Renda 2011Perché i due pacchetti Telecom non hanno creato il mercato

unico ?

Eccessiva enfasi sull’approccio nazionale ai mercati ( 500 analisi di mercato

nazionali )

Mancata armonizzazione legata alla mancanza da parte della Commissione

del potere di veto sui rimedi ( art 7 della procedura)

Regulatory Gap legato all’assenza di un vero regolatore unico in Europa (

ERG, BEREC…) : «nè carne né pesce»

Problemi legati alle policy sugli investimenti infrastrutturali

Poteri sullo spettroThe current European institutional setting

Directives

Regulations

Recommendations

Guidelines

Regulatory Regulatory

guidance European guidance

BEREC(1) RSPG(2)

Commission

Article 7 procedure

on market analysis

NRAs

(1) Body of European Regulators for Electronic Communications

(2) Radio Spectrum Policy GroupMarket Analysis: Art.7 procedure

► NRAs must notify to the European Commission (EC), the Body of

Phase I European Regulators for Electronic Communications (BEREC) and other

NRAs the findings of their analyses of the competitiveness of markets

susceptible of ex‐ante regulation

►The Commission can open an extended investigation (Phase II) if it has

serious doubts

►Market definition and SMP: the Commission has a veto power

Phase II ►Remedies: the Commission has no veto powerEU POLICY SUGLI INVESTIMENTI

I Telecom Packages hanno fallito:

EU ha perso la leadership che avevano con il 3G a favore degli USA con

il 4G

Sostanziale mancanza di investimenti soprattutto nelle reti in fibra e

accessi 4G

Eccessiva enfasi sui prezzi ( Accesso/Make or Buy)

Politiche sul consolidamentoCONFRONTO USA EU SUGLI INVESTIMENTI 1/2 Source: Yoo ( 2015)

CONFRONTO USA EU SUGLI INVESTIMENTI 2/2 Source: Yoo (2015)

Modelli di sviluppo digitale a confronto: meno operatori più reti

Diversi livelli di consolidamento di mercato Diversi livelli di copertura nelle principali aree mondiali

COPERTURA UBB FISSA Ultimo dato disponibile*

SUD COREA 98%

GIAPPONE 94%

≥ 50 Mb/s USA 85%

13* ≥ 30 Mb/s UE 62%

RETE FISSA

OPERATORI ATTIVI

>300* ITALIA 32%

* Italia 03/2015 – UE Q4 2013 – Altri 2014

* USA: operatori con copertura in almeno 20 stati Fonte GSMA: 2014

COPERTURA UBB MOBILE

* UE: operatori di rete fissa e operatori con un accordo di unbundling

SUD COREA 100%

GIAPPONE 99%

4** RETE MOBILE

OPERATORI ATTIVI

>100** USA 98%

** USA: 4 operatori hanno il 95% del mercato (9 operatori totali) ITALIA 80%

** UE: conteggiata la presenza degli operatori in ogni singolo mercato nazionale

UE 75%CONTENT REGULATION

Regole sul commercio elettronico: una combinazione di direttive e regolamenti scritti e gestiti dai

vari direttorati della CE con l’obiettivo non di UNIFICARE le legislazioni nazionali ma di

ARMONIZZARLE per creare le condizioni per un mercato unico digitale.

3 aree di interesse : SALES, INTELLECTUAL PROPERTY, DATA E CONSUMER PROTECTION gestite

attraverso una serie di direttive framework:

2001 E-Commerce Directive

2001 Copyright Directive

1995 Data Protection Directive

2011 Consumer Rights Directive

E-Commerce Directive :

Principio del «paese di origine»: se il servizio è legale nel paese di origine, allora lo è anche in

quello di destinazione

Responsabilità degli Intermediaries: pure conduit !

Audio-Video Media Services Directive (AVMSD) che coordina il settore audiovisivo in Europa :

sistema due corsie: televisione lineare e on demand con regole separate.

Fonte : Andrej Savin ( 2015)LIMITI DELLA CONTENT REGULATION

Il framework per il Commercio Elettronico ha offerto un quadro di riferimento stabile ma

permangono notevoli criticità.

L’esistenza di un gruppo di direttive relative alle vendite, non nasconde il fatto che non esiste

una legge universale sui contratti

Le leggi sulla consumer protection nei fatti non proteggono i consumatori nelle transazioni

cross- border

Le misure di protezione dei consumatori che permettono la gestione del contenzioso nel

paese in cui sono domiciliati non tengono conto del fatto che i consumatori raramente si

riivolgono ai tribunali per queste operaizoni e che quindi dovrebbero esistere meccanismi

alternativi per risolvere le controversie.

Lo stesso discorso si può fare per il settore dell’audio-visivo: se è vero che è stato raggiunto un

certo grado di coordinamento nel settore in Europa, tuttavia non sono stati risolti i problemi di

fondo:

La grande quantità di contenuti americani consumati in Europa;

L’impossibilità di fra circolare liberamente e universalmente i contenuti in Europa

Le incertezze generate dalla concorrenza da parte degli OTT

Più in generale le difficolta collegate alla convergenza di tecnologie e di servizi : «does a video

service which runs on a mobile network fall under the telecom rules, e-commerce rules or both ?»

Fonte : Andrey Savin (2015)I grandi attori di Internet sono tutti… «Born in the USA»

Nei confronti degli USA il ritardo dell’Europa non è solo in termini di reti, ma soprattutto in termini di

squilibrio rispetto ai grandi attori del mondo Internet

I grandi attori di internet viaggiano

«sopra la rete» (Over the Top)

Le ragioni del successo mondiale

Economie di scala

Modello di business innovativo incentrato su

advertising mirato e valorizzazione dei BIG DATA

OTTs

? Servizi gratuiti finanziati da advertising

Ma anche…

RETE Assenza di regole negli USA su privacy, data

protection, sicurezza

Assenza costi per infrastrutture di rete

TELCOs In Europa invece

La privacy è un diritto inalienabileAsymmetry between OTT and Telcos

24Maggio 2010: THE DIGITAL AGENDA

Maggio 2010 - THE DIGITAL AGENDA : 16

Key Actions

Planned delivery date

A vibrant digital Single Market

Key Action 1: Simplify copyright clearance, management and cross-border licensing by:

• Enhancing the governance, 2010

transparency and pan-European licensing

for (online) rights management by

proposing a framework Directive on

collective rights management

• Creating a legal framework to facilitate 2010

the digitisation and dissemination of

cultural works in Europe by proposing a

Directive on orphan works, to conduct a

dialogue with stakeholders with a view to

further measures on out-of print works,

complemented by rights information

databases

• Reviewing the Directive on Re-Use of 2012

Public Sector Information, notably its

scope and principles on charging for

access and use.

Key Action 2: Ensure the completion of the Single Euro Payment Area (SEPA), 2010

eventually by binding legal measures fixing an end date for migration and facilitate the

emergence of an interoperable European eInvoicing framework through a

Communication on eInvoicing and by establishing a multistakeholder forum

Key Action 3: Propose a revision of the eSignature Directive with a view to provide a 2011

legal framework for cross-border recognition and interoperability of secure

eAuthentication systems

Key Action 4: Review the EU data protection regulatory framework with a view to 2010

enhancing individuals' confidence and strengthening their rightsMaggio 2010 - THE DIGITAL AGENDA : 16 Key Actions

Interoperability and standards

Key Action 5: As part of the review of EU standardisation policy, propose legal measures on 2010

ICT interoperability to reform the rules on implementation of ICT standards in Europe to

allow use of certain ICT fora and consortia standards

Trust and security

Key Action 6: Present measures aiming at a reinforced and high level Network and 2010

Information Security Policy, including legislative initiatives such as a modernised European

Network and Information Security Agency (ENISA), and measures allowing faster reactions in

the event of cyber attacks, including a CERT for the EU institutions

Key Action 7: Present measures, including legislative initiatives, to combat cyber attacks 2010 2013

against information systems by 2010, and related rules on jurisdiction in cyberspace at

European and international levels by 2013

Fast and ultra fast internet access

Key Action 8: Adopt a Broadband Communication that lays out a common framework for 2010

actions at EU and Member State to meet the Europe 2020 broadband targets, including:

• Reinforce and rationalise, in this 2014

framework, the funding of high-speed

broadband through EU instruments (e.g.

ERDF, ERDP, EAFRD, TEN, CIP) by 2014 and

explore how to attract capital for broadband

investments through credit enhancement

(backed by the EIB and EU funds);

• Propose an ambitious European Spectrum 2010

Policy Programme in 2010 for decision by the

European Parliament and the Council that

will create a co-ordinated and strategic

spectrum policy at EU level in order increase

the efficiency of radio spectrum

management and maximise the benefits for

consumers and industry

• Issue a Recommendation in 2010 to 2010

encourage investment in competitive Next

Generation Access networks through clear

and effective regulatory measuresMaggio 2010 - THE DIGITAL AGENDA : 16 Key Actions Research and innovation Key Action 9: Leverage more private investment through the strategic use of pre-commercial procurement and public-private partnerships , by using structural funds for research and innovation and by maintaining a pace of 20% yearly increase _ of the ICT R&D budget at least for the duration of FP7 Enhancing digital literacy, skills and inclusion Key Action 10: Propose digital literacy and _ competences as a priority for the European Social Fund regulation (2014-2020) Key Action 11: Develop tools to identify and 2012 recognise the competences of ICT practitioners and users, linked to the European Qualifications Framework and to EUROPASS and develop a European Framework for ICT Professionalism to increase the competences and the mobility of ICT practitioners across Europe

Maggio 2010 - THE DIGITAL AGENDA : 16 Key

Actions

ICT-enabled benefits for EU society

Key Action 12: Assess whether the ICT sector has 2011

complied with the timeline to adopt common

measurement methodologies for the sector's own energy

performance and greenhouse gas emissions and propose

legal measures if appropriate

Key Action 13: Undertake pilot actions to equip Europeans 2015- 2020

with secure online access to their medical health data by

2015 and to achieve by 2020 widespread deployment of

telemedicine services

Key Action 14: Propose a Recommendation defining a 2012

minimum common set of patient data for interoperability

of patient records to be accessed or exchanged

electronically across Member States

Key Action 15: Propose a sustainable model for financing 2012

the EU public digital library Europeana and digitisation of

content

Key Action 16: Propose a Council and Parliament Decision 2012

to ensure mutual recognition of e-identification and e-

authentication across the EU based on online

'authentication services' to be offered in all Member States

(which may use the most appropriate official citizen

documents – issued by the public or the private sector)11 september 2013 : TSM Regulation Proposal –

the institutional governance reform

► On 11 September 2013, the EC published a draft Regulation aimed at

achieving the goal of a Telecom Single Market (TSM).

► Amongst other things, it proposes:

► a “light” BEREC reform;

► Commission veto powers on remedies for SMP operators operating under

an EU authorisation;

► new rules on Spectrum including Commission veto power on spectrum

right of use assignment.European Parliament position

► On April 3, 2014 the European Parliament, voted a set of amendments to TSM

Regulation among which:

1) deletes the Commission veto power on remedies;

2) deletes the BEREC reform;

3) reinforces NRA’s autonomy by defining NRA’s minimum competences;

4) confirms the reform on spectrum and adds a minimum 25 years duration for

spectrum right of use assignment;

5) requires the Commission to review the entire EU Regulatory Framework by 30

June 2016 (no review of BEREC explicitly requested).

31The previous EC proposals for regulation review

2002 Review 2009 Review TSM Regulation

Proposed Result Proposed Result Proposed EP

Veto power on market

Yes Yes Yes Yes ‐ ‐

definition and SMP

Veto power on remedies Yes No Yes No Yes No

Power on spectrum Yes

Yes Yes Yes

No (Pan European No

assignment (veto power)

Authorization)

(veto power) (veto power)

European Regulatory High Level BEREC with more

Com. Group

No EECMA BEREC autonomy

No

Authority

*European Electronic Communications Market AuthorityA new EC and a new Digital Single Market Strategy

A new European Commission took office in November 2014, approved by a

new elected European Parliament (May 2014)

The new EC adopted on 6 May 2015 the Digital Single Market (DSM)

Strategy that «aims to open up digital opportunities for people and business

and enhance Europe’s position as a world leader in the digital economy»

The DSM Strategy is built on three pillars and includes a set of targeted

actions to be delivered by the end of 2016 (it’ll be some time before the EC

proposals translate into actual changes in EU law)

Will it be an improvement or a real step change ?

33A Strategy for the Digital Single Market 1/2

EC President Junker’s political guidelines three pillars

We will need to have the courage to break down

national silos in telecoms regulation, in copyright and

data protection legislation, in the management of radio

Better online access for

waves and in the application of competition law.

consumer and business to on-

line goods and services across

We can ensure that consumers can access services, Europe

music, movies and sports events wherever they are in

Europe and regardless of borders

Creating the right condition for

digital network and service to

We can create a fair level playing field where all flourish

companies offering their goods or services are subject

to the same data protection and consumer rules Maximising the growth

potential of our European

By creating a connected digital single market, we can

Digital Economy

generate up to € 250 billion of additional growth

thereby creating hundreds of thousands of new jobs

34A Strategy for the Digital Single Market 2/2

PILLAR ACTION

1. Harmonization and simplification of consumer and contract law for online purchases

of digital content (2015)

2. Review of the Regulation on Consumer Protection Cooperation (2016)

Better access for 3. More efficient and affordable parcel delivery (2016)

consumer and 4. End of unjustified geo-blocking through the review of e-Commerce Directive and of

business to on-line Services Directive (2015)

goods and services 5. Antitrust competition inquiry into the e-commerce sector in the EU (2015)

6. Review of the copyright framework to improve access to digital content (2016)

across Europe

7. Review of the Satellite and Cable Directive (2015/2016)

8. Reduction of the administrative burden businesses face from different VAT regimes

(2016)

9. Review of the TLC regulatory framework to ensure effective spectrum coordination,

and common EU-wide criteria for spectrum assignment at national level; create

Creating the right incentives for investment in UBB; ensuring a level playing field for all market players

(TLC operators and OTT) (2016)

condition for digital

10. Review of the Audiovisual Media Services Directive (2016)

network and service

11. Comprehensive assessment on the online platforms (2015)

to flourish 12. Review of the e-privacy Directive (2016)

13. Privat Public Partenersip on Cybersecurity (2016)

14. European free flow of data initiative to promote the free movement of data in the EU

(2016)

Maximising the 15. Definition of priorities for standards and interoperability in areas critical to the DSM,

growth potential of such as e-health, transport planning or energy (smart metering) (2015)

our European 16. Support an inclusive digital society where citizens have the right skills to seize the

Digital Economy opportunities of the Internet. New e-government action plan to connect business

registers across Europe and ensure businesses and citizens only have to

communicate their data once to p.a. (2016)TREND DELL’AUGMENTED INTELLIGENCE AGE OR

AUGMENTED AGE

ARTIFICIAL INTELLIGENCE: disrupts the nature of advice, that is better at

everyday tasks like driving, health care and basic services than humans

DISTRIBUTED, EMBEDDED EXPERIENCES that are embedded into the

world and devices around us enable frictionless, contextualised service,

products, advice. Everything will have a chip inside it, will sync with the

cloud and interface with humans and other computers.

SMART INFRASTRUCTURES: improvements that radically change the way .

energy is delivered, goods and people are moved (drones, solar energy,

electric vehicles..)

GENE EDITING AND HealthTech are going to eadically change the way we

think about health care. Hereditary diseases like Parkinson’s, Alzheimer’s

etc, will be eliminated within two decades.FIRST PILLAR :Better access for consumer and

business to on-line goods and services across

Europe

Focus on:

Geoblocking

Review of the copyright framework to improve access to digital

content (2016)

FintechDSM: Geo-Blocking

Geo‐blocking or geoblocking is the practice of Geo‐blocking is sometime used to

restricting access to content based upon the user's redirect online shoppers to a local

geographical location website which offers the same

products at higher prices, which can

be illegal under EU law.

Another type of geo‐blocking occurs

when media companies prevent

consumers from watching online

content like films or tv series in a

territory where the company has not

acquired licenses.

The commission has agreed to

eliminate “unjustified geo‐blocking”.

The definition of “unjustified” is yet to

Tackling geo‐blocking be defined.

In 52% of all attempts at crossborder orders

the seller does not serve the country of the consumer “The EU’s internal market and geo‐

blocking cannot coexist.” Andrus Ansip,

less clients, EU Vice‐President for Digital Single

less revenues Market

for companies

Commission s’ Cross Border

Portability ProposalDSM: Copyright

Copyright is critically important to the European Union because it affects media,

cultural, and knowledge industries.

The Commission’s objective is to modernise copyright and ensure the right balance between

creators' and consumers' interests. This will give people better access to culture, support

cultural diversity, and open new doors for artists and creators.

‐Widening and harmonizing

exceptions and limitations

‐Unified rules across Europe for

Commission’s innovative ways to generate value

Proposals with data and data mining

‐Pan european license for contentFINTECH

«All business that use innovative operational, technological or business models designed to

address merging issues in the financial services industry» ( Association France Fintech)

It includes personal finance management services, equity financing or crowdfunding platforms,

money transfer services, InsurTech, etc.

Private investment in Fintech climbed from $4bn in 2013 to $19bn in 2015 and estimates for

spending over the next three to five years stanf at $150bn.

The United States is where the bulk of investments in FinTech were concentrated in 2015:

totalling $12bn, followed by Europe ($4bn) and the APAC region ($3bn) (Digiworld n. 103)

Within 20 years ,may banks will physically disappear and all operations will be done online.

Paper and signatures have no future in the banking world

MOVEN https://moven.com/ «the bank of the future» !!!! It redefines people’s relationship with

their money

In the EU direct cross border activities in the retail financial sector have been negligible . For

example in the euro area only 0,8% of retail loans for households were extended on a cross-

border basis in 2013 . The only exceptions is Luxemburg (31,6%) with large group of commuters.

The low market share can be explained by the presence of several obstacles. Natural barriers like

geographical distance and languages to structural barriers like difference sin regulation, taxation,

infrastructures and institutional framework.POTENTIAL FOR CROSS-BORDER MARKET ACROSS RETAIL

FINANCIAL SEGMENTS IN THE EU

Source : Study on the role of digitalisation in teh creating a true singe market for retail financial

services and insurances . EU (2016)BLOCKCHAIN

A blockchain is a decentralized ledger that relies on cryptographic algorithms and economic

incentives in order to ensure the integrity and legitimacy of every transaction. A copy of the

blockchain is shared amongst all nodes connected to the network, which comprises the history

of all valid transactions. Each transaction is recorded into a “block” which is appended

sequentially to the previous block of transactions. In order to prevent anyone from tampering

with past transactions, the blockchain acts as append-only ledger –i.e. once information has

been recorded onto the blockchain , it can no longer be edited or deleted. The result is a long

chain of blocks that represents the whole chain of transaction ever since the first genesis

block. The blockchain can thus be regarded as a secure database that comprises a public log of

all transactions which have been thus far validated by the network. In view of its decentralized

nature, the security of the blockchain and the validity of every transaction can only be ensured

through distributed consensus (i.e. through nodes verifying the integrity and legitimacy of each

block, independently of any trusted third party) (Primavera De Filippi , 2016)

https://www.youtube.com/watch?v=VJ2cMN2rnQQ

https://www.youtube.com/watch?v=2Zp37zarSQc

BLOCKCHAIN APPLICATIONS

: https://www.youtube.com/watch?v=cFfCh0AUDTw

Energy, etc

Estonian Governments has decides to offer blockchain notarization services to e-residentsSECOND PILLAR :Creating the right condition for digital

network and service to flourish

• FOCUS ON :

• CYBERSECURITYCYBERSECURITY

Cyberspace: a backbone of

digital society & economic growthCybersecurity incidents are

increasing at an alarming pace

with potentially profound effect on daily

functioning of society & economy,

both online and offline

…as well as financial theft, loss of intellectual property, data breaches, etc.What does this mean in practice? The survival of strong European cybersecurity industry all together is at stake!

Cybersecurity is also an opportunity!

TODAY

TOMORROWCybersecurity contractual Public-Private

Partnership (cPPP)

• Stimulate the

competitiveness and

innovation capacities of the

digital security and privacy

industry in Europe

• Ensure a sustained supply of

innovative cybersecurity

products and services in

Europe H2020 = legal framework for the establishment of the cPPP

H2020 LEIT‐ICT to focus on technology‐driven digital security building blocks and horizontal

requirements

H2020 Societal Challenge 'Secure Societies' to deliver societal benefits for users of technologies

(citizens, SMEs, critical infrastructures…).

H2020 public funds to be matched by private sector investment

49THIRD PILLAR :Maximising the growth potential of

our European Digital Economy

:

• FOCUS ON : ICT, JOBS & SKILLSCurrent challenges Rough Structural Changing economic unemployment demographics recovery

Autor and Dorn (2012):U‐shaped curve

(employment by skill level)

Autor and Dorn 2012

The Growth of Low Skill Service Jobs and the Polarization of the U.S. Labor MarketAreas with significant job losses

• Postal Service Mail Carriers ‐11%

• Meter Readers, Utilities ‐17%

• Travel Agents ‐46%

• Data Entry Keyers ‐54%

• Telephone Operators ‐71%

US data. Source: Robert Atkinson, OECDGrowth in personal services: Child care

2000 2010

398 090 631 240

US data, Source: Robert Atkinson, OECDTechnology leads to labour market transformations

Technological upheavals 1930 2000

Technological upheavals: Internet

New high skilled ICT jobs

Data scientists

App developers

Engineers

Transformed jobs with

new ICTs

Jobs in traditional

sectors but workers

need reskilling and

retraining to take

advantage of new ICTs

Displaced (Lost,

Outsourced)

Some workers will not

be able to make the

transition and will be

displaced. Need social

policies.SKILLS IN EUROPE

• NEW HIGH SKILLED ICT JOBS :

• Over the period 2000-2012 ICT employment growth was 4.3% per year more than 7 times

higher than the total employment growth over this period.

• Regarding the demand for digital skills a recent study among CEOs showed that concerns

regarding the availability of key skills have grown significantly, reaching 73% of

respondent.

• In the UK alone the demand for big data specialists is expected to rise by 160% over the

period 2013 to 2020.

• Employment of ICT professionals is resistant to economic downturns and ICT professionals

contribute to increased productivity in firms. It has been estimated that by 2020 the

shortage of ICT professionals will amount to up to 825.000if no decisive action is taken. In

the EU only the app developer work force will grow from 1 million in 2013 to 2.7 million in

2018.

• RETRAINING

• Currently 39% of EU citizens have only low or not digital skills. About 18% of the EU population

has never used the Internet.

• There is also a significant shortage of employees who combine specialised and soft skills as

entreprenership, business and management skills

• GLOBAL PARTNERSHIP BETWEEN THE PRIVATE & THE PUBLIC SECTOR, Grand Coalition for

Digital Jobs , Coding Initiative, etcMOOCs

Massive Open Online Courses

• Coursera: Nearly 4 million registered users

• 390 open courses

• 83 partner universitiesProposta di Nuovo Codice delle Comunicazioni

Elettroniche Europee + Comunicazione Gigabit

Society (14 Settembre 2016) 1/3

• Target 2025 sulla Connettività a Larga Banda

• I Principali motori socioeconomici :connettività simmetrica a 1Gbps

• Tutte le famiglie europee, nelle zone rurali o urbane, dovrebbero avere

accesso ad una velocità di download di almeno 100Mbps

• Tutte le aree urbane e le principali direttrici di traffico dovrebbero avere

una continuità di copertura 5 G. Come obiettivo intermedio il 5G dovrebbe

essere implementato in almeno una grande citta di ogni stato membroProposta di Nuovo Codice delle Comunicazioni

Elettroniche Europee + Comunicazione Gigabit

Society (14 Settembre 2016) 2/3

• Double –lock veto della CE e del BEREC sulle decisioni delle NRA relative ai

rimedi

• Possibilità le NRA di non imporre obblighi regolatori in caso di

coinvestimento

• Spettro: maggiore protagonismo della CE e delle NRA per armonizzarne la

gestione . Maggiore spazio allo spettro non licenziato, allo sharing e

trading.Proposta del Nuovo Codice delle Comunicazioni

Elettroniche Europee + Comunicazione Gigabit

Society (14 Settembre 2016) 3/3

• Servizi di comunicazione: La CE riconosce che ci sono alcuni servizi forniti

dagli OTT che hanno funzionalità equivalenti a quelli forniti dalle telco pur

non essendo soggetti alle stesse regole.

• REVISIONE degli ECS (Electronic Communication Service,) includendo 3

categorie di servizi: (i) Internet Access Services (IAS, (ii) Communication

Services (CSe (iii) Servizi consistenti principalmente o interamente nel

trasporto dei segnali. La maggioranza delle misure per il cliente finale (es:

accesso ai servizi di emergenza, portabilità del numero, interoperabilità) si

applicheranno solo a IAS e CS che utilizzano risorse di numerazione (quindi

i servizi voce tradizionale ma anche SkypeIn e SkypeOut). Non si

applicheranno invece quando la numerazione è utilizzato solo come

identificativo dell’utente (e.g. Whatsapp e chiamate Skype-Skype).

• Il BEREC viene trasformato in un’agenzia europea.CONCLUSIONI • ANDANTE… MODERATO !!!!

Puoi anche leggere