INDIA GOES GREEN : BNL AND BNP PARIBAS SUPPORT - MAURIZIO ACCINNI RIMINI 6 NOVEMBRE , 2015

←

→

Trascrizione del contenuto della pagina

Se il tuo browser non visualizza correttamente la pagina, ti preghiamo di leggere il contenuto della pagina quaggiù

INDIA GOES GREEN :

BNL AND BNP PARIBAS SUPPORT

MAURIZIO ACCINNI

INTERNATIONAL DEVELOPMENT MANAGER

RIMINI 6 NOVEMBRE , 2015

DIVISIONE CORPORATE

Agenda BNL BNP PARIBAS INDIA POWER SECTOR AND BNP PARIBAS CAPABILITIES

BNL BNP PARIBAS

Solidi, dinamici, internazionali, italiani

UNA BANCA SOLIDA SU CUI CONTARE

La solidità patrimoniale ci permette di essere al vertice tra i nostri competitor in termini di rating (Standard & Poor's

A+): una garanzia per la continuità della relazione finanziaria.

Una favorevole situazione di liquidità consente di sostenere in modo costante l’economia del paese e lo sviluppo

strategico dei nostri clienti.

UNA BANCA DINAMICA

Una strategia commerciale basata sulla diversificazione dell'offerta: una tra le più complete sul mercato, per

l’operatività corrente e straordinaria. Una capacità di seguire l’evolvere delle esigenze aziendali innovando prodotti

e servizi. Oggi e domani, partner, insieme.

BNL GRUPPO BNP PARIBAS. LA FORZA DI UN’IMPRESA INTERNAZIONALE

Tra i dieci gruppi bancari più grandi al mondo; i nostri clienti italiani possono accedere facilmente ad un network

internazionale presente in più di 80 nazioni, in tutti i continenti. In India da 150 anni, 3.000 dipendenti in Cina.

Leader nel Bacino del Mediterraneo e nel Golfo Persico. 90 Trade Center in 55 paesi, di cui 5 in Italia, con esperti

dedicati al commercio internazionale

BNL. UNA REALTÀ ITALIANA

Distribuzione capillare in tutta l’Italia. Oltre 2,5 milioni di clienti privati, oltre 27.000 imprese e 16.000 enti

Legame solido con il tessuto produttivo italiano e con la Pubblica Amministrazione centrale e locale.

4L’attività del gruppo in Italia

5BNL: la banca per i bisogni del cliente

6Il percorso di internazionalizzazione

Sostenere le tue

attività all’estero

Investire

Esportare Capitale e Credito

Esplorare i Trade Center

mercati

Consulenza e strutture

Un modello costruito per stimolare, semplificare e supportare

l’internazionalizzazione dei nostri clienti

7Esplorare i mercati: le strutture

LA RETE BNP PARIBAS

Una forte presenza in Europa…….

UNA “CORSIA PREFERENZIALE” PER ACCEDERE AI NUOVI MERCATI Austria

Belgio

Bulgaria

• 75 paesi e 198.000 collaboratori Danimarca

Francia

Olanda

• Più di 1700 gestori di relazione dedicati alle imprese Germania

Polonia

Ungheria

Portogallo

• Una combinazione «unica» di competenze e soluzioni Irlanda

Romania

per soddisfare le specifiche esigenze del cliente Italia

Russia

Lussemburgo Regno Unito

• Conoscenza qualificata nelle relazioni con il mercato Norvegia

Repubblica ceca

locale Spagna

Svezia

Svizzera

Turchia

….. Asia, Africa, Medio Oriente …..e sul continente americano

Algeria

Tunisia

Marocco

Canada

Senegal

USA

Guinea

Messico*

Burkina Fasi

Colombia*

Mali

Venezuela

Costa d’Avorio

Brasile

Gabon

Perù

Sud Africa

Cile

Turchia

Argentina

Arabia Saudita

Kuwait

Bahrain

Qatar

Emirati Arabi * Ufficio di rappresentanza

8Investire su nuovi mercati

CAPITALE CREDITO RETI DI IMPRESA

Interventi diretti BNL nel capitale Interventi creditizi diretti BNL in favore Le imprese che si uniscono in rete sono più

d’impresa volti a favorire le aziende italiane della case madre italiana o delle competitive e possono ottenere maggiore

che aspirano ad una dimensione sussidiarie estere. attenzione da parte della banca

internazionale del proprio business.

Accesso ai mercati di capitali BNL ha firmato un intesa con Confindustria per

attraverso emissioni obbligazionarie e/o supportare la creazione di Reti premiandole con

Intervento congiunto BNL – SIMEST MINIBONDB forme di credito innovative a loro dedicate.

finalizzato ai progetti di investimento e alle

iniziative di radicamento sul mercati esteri Convenzioni per finanziamenti a breve Prodotto di finanziamento 2X Rete: la

delle imprese italiane. e medio lungo termine con garanzia banca sosterrà i progetti di sviluppo delle reti

SACE per agevolare l’accesso al credito finanziandoli per un importo fino a due volte le

delle PMI italiane che presentano un risorse destinate alla realizzazione delle

fatturato estero non inferire al 10% e che iniziative di rete fino ad un massimo di 3 mln €

vogliono allargare la propria operatività sui

Riduzione dello spread su tali

mercati internazionali

finanziamenti dal 15% al 30% per i migliori

progetti di rete.

Sostegno alle reti per il loro sviluppo

SIMEST, Società Italiana per le Imprese SACE, Servizi Assicurativi del Commercio internazionale con l’appoggio di tutti gli sportelli

all’Estero, promuove i processi di Estero, è la principale agenzia di credito esteri della banca

internazionalizzazione delle imprese italiane e all’esportazione italiana mirata a sostenere

assiste gli imprenditori nelle loro attività gli investimenti all'estero delle imprese

all’estero, partecipando alla realizzazione di italiane, assicurandone le operazioni contro il

investimenti e favorendo gli scambi rischio commerciale e politico.

commerciali.

9Investire su nuovi mercati

CASA MADRE

ITALIANA

CINA TURCHIA INDIA TUNISIA

SUSSIDIARIA CINESE SUSSIDIARIA TURCA SUSSIDIARIA INDIANA SUSSIDIARIA TUNISIA

Una strategia «unica», un «unico» entry point …. verso un mondo di opportunità

With you across Europe and Beyond

10Partnership

“…aumentare e integrare la capacità di offerta di servizi alle imprese

e, tramite le reciproche professionalità e le rispettive reti di contatti

sull’estero, incrementare l’efficacia dei servizi stessi..”

…..perché le grandi imprese si costruiscono insieme!!!!

11India Power Sector and BNP PARIBAS capabilities

India Power Sector – Key Milestones

1991-2003 – Liberalisation Era

Private sector participation in

generation

National Electricity Policy Fast track clearing of proposals

(2006) Rationalisation of tarriffs

Guidelines for bidding

Coal Block Auction

Case-1 and Case-2

bidding for power projects GoI has kick-started

the next phase:

Launch of UMPP scheme 1991-

auction and allotment

(bidding for 4000MW 2003 of 67 coal blocks

power projects) Private Equity completed

2006 Investments in Supreme Court

Renewable energy cancels allocation of

Renewed GOI

Renew Power 214 coal blocks

incentive and push for

Continuum Energy Fresh auction to be

Renewable Energy

Green Infra conducted for the 214

2008- Greenko

coal blocks

2010 Azure Power

Mytrah Energy

2010

IPOs of large thermal 2011 2015

2014

power producers 2011-12 2012

Reliance Power

Adani Power

Indiabulls Power

JSW Energy

Policy support for CAG (comptroller

Renewables accounts general)

Jawaharlal Nehru National Changes in regulations accuses government

Solar Mission (Solar Capacity in Indonesia of inefficient coal

of 20W by 2022; 2019 target Increase in prices of block allocation

of 15GW) imported coal from between 2004-2009

Tax holidays and generation Indonesia

based incentives

13Thermal Power - slow and gradual revival…

… Driven by Ongoing coal block auctions and SEB reform programme

KEY TRENDS

India Power sector is an important contributor to overall growth and GDP

STRUCTURAL

Over the last few years, the thermal power sector has been adversely impacted by: IMBALANCES

Low utilization of power

Supreme Court judgment: Cancellation of coal mining license

plants

Breakdown in Policy issues: Delay in environmental clearance of coal blocks

Reliance on imported coal

Externality: Increase in Indonesian coal royalty and taxes

given relatively low coal

Poor financial health of SEBs resorting to load shedding

linkage from Coal India

INR USD adverse movement with PPA contracts having no fuel pass-through

Insufficient cash flow for

High interest / inflation rate environment resulting in increasing interest costs

interest, principal payments

Recent coal block

update:

Structural imbalances in Sector to be resolved in near-medium term; demand to revive

On Sep 2014, Short Term: Change of PPA contracts adversely impacted by no-fuel pass through; “Modi” government

Supreme Court of India

expected to revive the overall industry creating additional power “demand”; Merchant power tariffs to tighten

cancelled the

allocation of 204 coal Medium Term: Pick-up in captive coal projects; SEB financial health restored leading to increase in power

blocks allocated to the procurement cost; cost of borrowing for infrastructure projects to reduce

private sector between

1990-2010 on the

grounds of corruption

Margin/return recovery is linked with improvement in power offtake and tariffs, domestic coal availability

Post the judgement, situation and lowering of interest rate cycle

GoI has kick-started

the next phase: auction

and allotment of 67

coal blocks completed Source: Brokers’ reports, BNP Paribas views

14Regional demand trends

South and North India faces higher energy deficiency than other parts of India

Power Demand Supply Position FY15 (BU) Peak Demand and Peak Met FY15 (GW)

6,3% 8,3%

1.069 1.031

4,1% 5,2% 155147

2,4%

0,8% 3,6% 2,2% 2,3%

5,1%

317 315 332 312 52 48

286 274 44 43

39 37

133 130 20 19

ER&NE SR WR NR All India ER&NE SR WR NR All India

Requirement Availability Deficit Requirement Availability Deficit

As of March FY15, India had a peak deficit of 8 GW

North India had the highest power deficit of 6.3% across India, while the overall deficit for India was 3.6%

The peak deficiency is worst for North India with deficiency of 8.3%

All India PLFs in FY2015 was 65% - low PLF was primarily due to poor financial health of discoms in India owning

to inability to pay power producers

Though new generation capacities are being added, issues related to low off-take, inadequate fuel availability,

transmission corridor availability and weak financial condition of the discoms continue to persist

15Recent consolidation in Thermal and Hydro Power Sectors

Power generation companies are focused on repairing their balance sheet

Many of the players in India do not have the financial firepower to invest in growth and new assets

Active M&A activity: exit of weaker players, driven by banks around concerns of high leverage

Consolidation is being led by players with strong balance sheet and foreign players

Nov 2014

$680mn

Acquisition of Adani Power Limited acquired Korba West Power Company Limited, the India-based owner and

Korba West Power Company operator of thermal power generation plant, from Avantha Power & Infrastructure Limited

owned by

Korba West is a 600MW power plant and will take the total installed capacity of Adani Power to

11,040MW making it the largest private sector power utility in the country

by The Avantha Group has been under pressure to cut debt raised through private equity firms and

banks for its power business and with this deal has announced its exit from the power business

JSW Energy Limited, acquired Himachal Baspa Power Company Limited from Jaiprakash Power

Nov 2014

$1,571mn Ventures Limited for $1,571mn

Acquisition of

Himachal Baspa Power Company Limited (HBPCL), owns and operates 300 MW Baspa II hydro-

Himachal Baspa Power

owned by electric project and 1,091 MW Karcham Wangtoo hydro project.

Through this acquisition, JSW will become a largest private sector hydro power generator in India

with its installed power generation capacity of increasing to 4,351 MW

by

Jaiprakash Power was cash strapped and had high leverage and this asset sale was inevitable;

Further it required capital to re-bid for coal mines that were de-allocated earlier by the Supreme

Court

Aug 2014

$984mn Adani Power acquired Udupi Power Corporation Limited, a 1,200MW coal fired power plant from

Acquisition of LANCO Infratech Limited, the listed India-based company engaged in the construction of

Udupi Power Corp infrastructure projects, ranging from dams, power projects and industrial structures to highways and

owned by

flyovers, for a consideration of $984m

The acquisition was a strategic fit to Adani’s integrated infrastructure business model and will further

by expand its footprint in Southern India.

The proceeds from the sale was used by Lanco to reduce its debt.

16Strong drivers underpinning Renewable Energy growth outlook in India….

…given challenges in thermal around fuel risk, regulatory overhang and increasing

tariffs

Incentivising capacity addition based on wind, solar and hydro power

Generation based incentive for wind energy projects – wind energy generators

Policy Support eligible for an incentive of INR 0.50/kWh for wind energy fed to the grid (cap of

for Renewable INR 10 mn/MW)

Energy Tax holiday for power projects which start generation by March 31, 2017

Proposed plan to set up country wide green Corridor for Renewable Energy

Lower regulatory overhang

Electricity demand consistently outpaced electricity supply

Power Demand Electricity supply side challenges - Consistent failure to achieve capacity

and supply addition targets laid out in five –year plans

mismatch Pressure of increasing electricity demand – Increasing electrification and

consumption growth have increased electricity demand

Gas and coal supply shortage, increasing cost of imported coal for thermal

power

Renewable Reduced availability of domestic gas led to low plant load factor (57% in

FY2012-13) for gas-fired power plants – as of October 2014, 16,000 MW gas-

Energy Sector No Fuel Risk

fired power capacity stranded due to gas shortage

Increase in imported coal- regulatory changes in major coal exporting countries

such as Indonesia and South Africa have led to increase in imported coal prices

Renewable energy is well positioned to see significant investments and

growth due to the mitigation of coal/gas fuel risk

Increasing power purchase cost of state utilities

Achieving Tariff Higher cost of imported coal and reduced supply of domestic gas have

Parity increased generation cost from imported coal and gas-fired power plants

Generation cost of power from renewable energy has become more

competitive

Increasing fuel cost driving industrial customer tariff

Increasing power purchase cost has led to higher supply costs, forcing

distribution companies to increase retail tariffs

High Cost of

Industrial Power Cross subsidizing domestic and agri customers by increasing industrial

customer tariff has led to industrial customers opting for renewable energy

resources

17Ambitious targets for Renewable Energy

India Government has set target generation capacity of 160GW by 2022

RENEWABLE ENERGY INSTALLED CAPACITY BREAK – UP (MARCH 2014)

Waste to

Energy

Solar Renewable energy growth led by wind

Bagasse 8,4%

0,3% sector which has grown by 24% (FY

Cogeneration

8,4% 2002 – 14)

Biomass

4,3% Strong investor interest for investment

Small Hydro into India – Sembcorp has acquired 60%

12,0% stake in Green Infra for $227mn

Wind

66,6%

Multiple Private-equity backed

Renewable energy companies in India

Total installed capacity31.7GW

GROWTH OF RENEWABLE INSTALLED

CAPACITY SIGNIFICANT POTENTIAL TO ADD CAPACITY

(GW) (GW)

40 12,6% 13,0% 15% 60.000

12,5%

11,4% 48.000

10,4% 50.000

30 9,6%

10%

40.000

20 21,1 30.000

19,1 30.000

17,4 23.000

14,2 5% 21.135

10 10,2 11,8

6,8 20.000 15.000

2,6 4,3 5,1

1,6 2,1 3,8

0 2,4 2,7 3,0 3,3 3,6 0% 10.000 3.804 4.121 2.649

Mar-2009 Mar-2010 Mar-2011 Mar-2012 Mar-2013 Mar-2014

0

Wind Wind Small Hydro Bio Power Solar

Others

Small Hydro Potential (MW) Installed Capacity (MW)

Percentage contribution of total installed capacity

18Wind Sector has experienced phenomenal growth in recent past

The sector has grown at CAGR 23.6% during FY 2002 to FY 2014

Huge potential of wind power yet to be untapped in

various states across India Challenges of the sector

Causes variability in generation

INTERMITTEN Mitigation

T NATURE OF Load dispatch and grid management practices

35.071

Gujarat WIND including day ahead forecasting of loads, likely

3.414

wind power injection and optimal play of hydro

reservoirs

14.493 Procurement of land for development of wind

Andhra Pradesh

753 projects is an obstacle in many states

LAND Mitigation

ACQUISITION

Land laws in each state need to be reviewed to

14.152

Tamil Nadu streamline land procurement for wind turbines

7.276

Mitigation

13.593 Comprehensive study of wind patterns and other

Karnataka

2.409 WIND climatic factors for a period of 2 to 5 years

RESOURCE New technologies and approaches to wind

ASSESSMENT resource assessment such as Lidar, Sodar,

5.961

Maharashtra meso-maps, numerical modelling etc. need to be

4.098 established for selection sites

With increasing turbine sizes, large cranes are

5.050

Rajasthan LOGISTICS & required for erection proposes

2.820

TRANSPORTA Availability of road connectivity in certain hilly regions

TION or far flung regions could pose a challenge to

2.931 logistics and transportation

Madhya Pradesh

439

Developing adequate transmission infrastructure for

0 10.000 20.000 30.000 40.000 evacuation of wind power and keeping pace with

EVACUATION growth of the wind energy sector

ISSUES

Grid system for power to flow from distributed wind

Wind Power Potential (MW) Present Installed Capacity (MW)

power generation to the main grid (220 kV/400 kV

level)

19Recent M&A activity in the Renewables Sector

Oct 2015

ReNew Power Ventures raised $ 265mn in a round led by Abu Dhabi Investment Authority (ADIA),

Equity Value: $200mn one of the two sovereign funds of the UAE

Minority stake in

ADIA invested $ 200mn to pick up a significant minority stake, while the rest came from existing

investors Goldman Sachs ($ 50mn) and Global Environment Fund ($ 15mn)

Acquired by Goldman Sachs continues to be the lead investor with a total investment of $ 370mn till date

Funding from the latest round takes the total amount raised by the company to $ 665mn till date

Sep 2015

Enel Green Power, the Italian developer of solar and wind energy projects, entered the Indian

Equity Value: $34mn

Majority stake in renewable power market with a €30mn ($34mn) acquisition of a majority stake in BLP Energy

BLP Energy is the solar and wind power subsidiary of Indian energy company Bharat Light & Power

Transaction marks the company’s first move into the Asia Pacific region

Acquired by

Acquisition also increases Enel’s net installed global capacity of clean energy to more than 10 GW

Jun 2015

Equity Value: $310mn SunEdison, the world’s largest renewables company acquired Continuum Energy for a total equity

Acquisition of valuation of $310mn (Enterprise Valuation: ~$615mn)

Continuum gives SunEdison ~242MW of operational wind power capacity with 170MW under

construction and over 1,000 MW of wind power plants under development

by

Continuum was 85% owned by Morgan Stanley Private Equity who had invested ~INR 1,200Cr. in

2012 to acquire the stake

Feb 2015 Sembcorp Utilities Pte Ltd, the Singapore-based company engaged in providing utilities, waste

$171mn management, terminalling, and logistics services acquired a 60% stake in Green Infra Limited, the

Acquisition of India-based company engaged in renewable power generation, from IDFC Private Equity for USD

171m

Green Infra adds to Sembcorp a sizable 516-megawatt operating asset portfolio with an additional

200MW under construction

by

Green Infra’s portfolio will almost triple Sembcorp’s current renewable energy generation capacity

globally to over 1,000 megawatts.

20India Presence for more than 155 Years

INVESTMENT

CORPORATE & SOLUTIONS

INSTITUTIONAL BANKING

Investment Banking

Wealth Management SBI Life Insurance

• M&A Advisory

74% SBI & 26% BNP Paribas (2001)

• Equity Capital Markets

• Debt Capital Markets BNP Paribas Investment

Corporate & Institutional

• Loan Capital Markets Sundaram BNP Paribas Fund

Services

• Project Debt Advisory & Financing Services

Client Coverage

• Sector Coverage 51% Sundaram Business Services &

Delhi BP2S Custody Services

• Energy & Natural Resources 49% BNPP Securities Services

(F&O Clearing) (2009)

• Media & Telecom

8 branches

• Transportation & Infrastructure BNP Paribas Sundaram Global

14,000+ employees: Securities Operations

Transaction Banking o 375 in CIB 51% BNPP Securities Services &

49% Sundaram Business Services

o 1,080 in ITES business (2009)

Fixed Income & Treasury Ahmedabad o 9,200 in Investment

Solutions BNP Paribas Mutual Fund

Kolkata 100% BNPP Investment Partners

Commodity Derivatives o 3,500 in Retail Banking (2010)

Invested USD1bn in last

Equity Derivatives and Cash Equities Mumbai few years

Pune

BNP Paribas India Holding Pvt. Ltd.

100% BNP Paribas SA (2012)

Hyderabad RETAIL BANKING

BNP Paribas Securities India Pvt. Ltd. Sundaram BNP Paribas Home

SREI Equipment Finance

(Institutional Broking) Bangalore Finance

50% SREI Infrastructure & 50%

100% BNP Paribas (2013) 50.1% Sundaram Finance &

BNP Paribas Lease Group (2007)

49.9% BNP Paribas Group (2007)

Chennai

BNP Paribas India Solutions (ITES) ARVAL India (Fleet Geojit BNP Paribas (Retail

100% BNP Paribas (2005) management) broking)

100% BNP Paribas (2007) 34% BNP Paribas (2007)

Joint Ventures / Subsidiaries (year of formation)

21Power Project Financing – Typical Transaction Structure

Sponsors Banks

Equity Debt CERC/ Regulator

Concession

Project Company

EPC Contractor

EPC Contract

(Special Purpose Vehicle) O&M Contract

O& M Contractor

Power

Fuel Supply Purchase

Agreement Agreement

Fuel Supplier Offtakers

EPC: Engineering, Procurement & Construction; PPA: Power Purchase Agreement

Sponsors: Established domestic (and few international) players

Revenue source: Long term Power Purchase Agreements (22-25 yrs) with State utilities, increasingly projects with

part merchant risk

Tariff: Mostly rupee denominated fixed tariff PPAs for bulk of capacity

Fuel Supply: Captive coal mines or third party long term fuel supply agreements (Domestic/International coal / Gas)

Technology: JVs of established international technology providers e.g. Siemens, Alstom etc with Indian companies,

increasing involvement of Chinese equipment suppliers

EPC contracts: fixed price, date certain EPC contracts

Power evacuation: transmission infrastructure, grid connectivity

Operations and Maintenance (O&M): In-house or O&M arrangements with experienced contractors

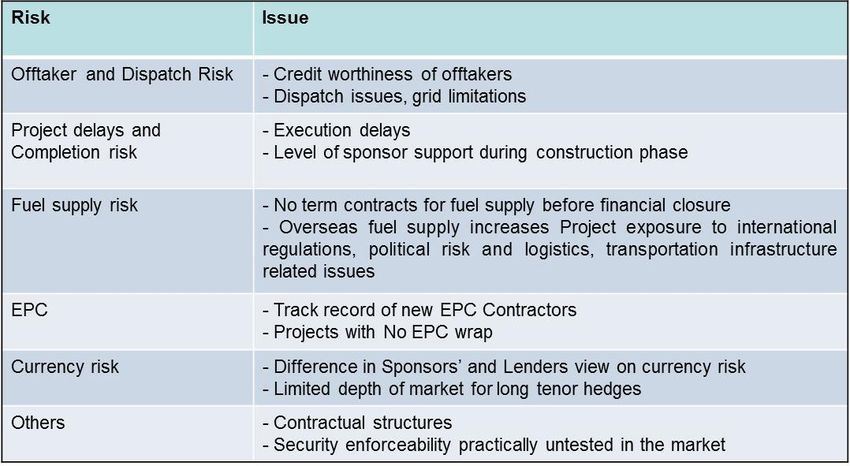

22Key Challenges for International Lenders

23Energy Sector - What BNP Paribas brings to the table

Financing Solutions Associated Solutions

Vanilla Products • M&A Advisory – building on global reach and in-

house expertise

Short Term

• Bilateral working capital solutions in INR • Debt Capital Market Solutions – offshore and

• Import financing solutions for raw materials onshore

• Export pre/post-financing solutions • Fixed Income hedging solutions

• Non-funded solutions – LCs/ BGs/ SBLCs/ documentary collections • Short tenor forwards and flow products

• Medium Term Swap Solutions (currency

Medium/ Long Term

• Syndicated Commercial Loan (ECB) and interest rates)

• ECA backed Financing • Commodity Hedging – Oil & Gas, Coal, Freight

• Project Financing • Carbon Credits Solutions

• Cash Management – domestic and international

Specialized/ Structured Products

Short Term

• Pre- export Financing solutions

• Specialized Inventory Finance (SIF)

• Borrowing base/ Transactional Financing solutions

Medium/ Long Term BNP Paribas has long relationships

• Reserve Base Lending (RBL) with most of the players in the Power,

• Mine Development Financing sector

• Other Limited Recourse Financing Solutions

24Select Credentials in Power sector in India

2015 2014 2014 2013 2013 2008

Power Power Power Power, Mining Power Power

Deal Size: US$ 300mn Deal Size: US$ 332mn Deal Size: $35mn Deal Size: US$ 400mn Deal Size: US$ 33mn Deal Size: US$ 327mn

7 year Rights Issue of Medium term INR loan due 5 year Corporate Guarantee Coastal Gujarat Power Ltd.

Syndicated Term Loan Tata Power 2016 Syndicated Term Loan CLP India to CLP Project Finance

Windfarms

Mandated Lead Arranger Joint Lead Manager Bilateral deal Mandated Lead Arranger MLA, Security Agent, KEIC

& Underwriter & Bookrunner Bilateral deal Agent & Sole Lender

Facility priced at Issue First funded deal Syndication of Part of RBI’s Multi-tranche

160bps over oversubscribed with Tata Power ANZ, Bank of FCNR-B limited-recourse

LIBOR by 1.96x, highest Pvt. Ltd. America, concessional project financing

Syndication of level for any Part of RBI’s Barclays, Credit scheme in support of a

RBS, Axis Bank, rights issue in FCNR-B Agricole, 4,000MW coal-

First Gulf Bank, India concessional Deutsche Bank, fired power

Societe Generale Strong scheme RBS and station in Mundra,

and SBI as other participation from Standard Gujarat

MLAs key institutional Chartered as

and retail other MLAs

investors

25Select Credentials in Oil & Gas sector in India

2015 2015 2014 2014 2014 2014

Advisor to

USD 2.25 bn

Deal Value : USD1.5bn Deal Value : USD400mn Deal size: USD 2.21 bn- Deal Size: CHF 200mn Acquisition Finance Sale of 30% stake in

3.6year Syndicated Term 3.25year Syndicated Term equivalent Senior Notes Facilities Peru block 108 to

Loan Loan Dual currency triple-tranche 3.00% due 2019 Woodside/Plus Petrol

bond issuance Mandated Lead Arranger

Mandated Lead Arranger Mandated Lead Arranger Joint Bookrunner Joint Bookrunner Sole M&A advisor

& Bookrunner & Bookrunner & Agent

2014 2013 2013 2013 2013 2013

USD 900 mn

Acquisition Finance Facility Deal Value : USD500mn Deal Value : USD500mn Deal Value : USD1.75bn Deal Value : USD400mn Deal Size: EUR 55 mn

6 year Syndicated Term Loan 3 year Syndicated Term Loan 5 & 6 year 5 year Syndicated Term Loan ECA Financing

Mandated Lead Arranger Mandated Lead Arranger & Syndicated Term Loan

& Bookrunner & Agent Bookrunner & Agent Mandated Lead Arranger Mandated Lead Arranger Mandated Lead Arranger

& Bookrunner & Bookrunner & Bookrunner & Agent

2010 2010 2010 2004, 2007 & 2011 2007 2007

Deal Size: USD 2bn Deal Value : USD 300mn Niko Resources Ltd Deal Value : USD275mn

Initial Public Offering of Deal Value : USD1.8bn Deal Value : USD150mn Deal Value : USD550mn

Essar Energy Plc Syndicated Term Loan Global ECA Facilitator

Syndicated Term Loan IFC – B Loan MLA (2004, 2007) Gas Field Development

(over multiple transactions) Lead Arranger Sole Arranger (2011) – White Financing

Co Lead Manager Mandated Lead Arranger Knight Lead Arranger

26Thanks for your attention !

m.accinni@bnlmail.com

internazionalizzazione@bnlmail.com

Le informazioni contenute in questo documento sono elaborate da BNL o tratte da fonti ritenute attendibili ma non vi è alcuna garanzia o dichiarazione sulla loro accuratezza,

completezza o correttezza.

BNL declina qualsiasi responsabilità per danni diretti o conseguenti danni derivanti da qualsiasi utilizzo del presente elaborato o del suo contenuto. Questo documento, pubblicato

per l'assistenza dei destinatari, è strettamente confidenziale e non può essere riprodotto, pubblicato o diffuso per alcuno scopo.

27Puoi anche leggere