IPSAS/EPSAS Stato dell'arte - ODCEC Roma

←

→

Trascrizione del contenuto della pagina

Se il tuo browser non visualizza correttamente la pagina, ti preghiamo di leggere il contenuto della pagina quaggiù

IPSAS/EPSAS

Stato dell’arte

Roma, Ottobre 2019

MEF – RGS – Servizio Studi Dipartimentale

Indice

► IPSAS e IPSAS Board

► EUROSTAT ed EPSAS Working Group

► Progetti RGS

MEF – RGS – SeSD

2

IPSAS e IPSAS Board

MEF – RGS – SeSD

3

International Public Sector Accounting Standards

IPSAS: regole tecnico-contabili per la redazione di GPFR*

*General Purpose Financial Reports: consistono in un sistema di report finanziari, che si basano

principalmente su un sistema di contabilità a base accrual (competenza economica), che forniscono

informazioni fondamentali sulla situazione e i risultati economico-finanziari di un’amministrazione pubblica.

I report contengono le informazioni sulla situazione e sui risultati economico-finanziari di un PA

Rilevano e rappresentano «integralmente» il patrimonio di una PA e le connesse variazioni di esercizio

Sono rivolti a potenziali destinatari interni ed esterni alla PA

RECOMMENDED

38 ACCRUAL BASIS IPSAS

3 PRACTICES

GUIDELINES

33 Adattamenti di

IAS/IFRS

5 Specifici per il

settore pubblico

MEF – RGS – SeSD

4

IPSAS Board

• Organismo rappresentativo della professione contabile a

livello internazionale;

• Unisce 157 ordini della professione contabile di 122 paesi;

• Ha il compito di emettere standard, tra i vari, anche nei

seguenti settori auditing (revisione), etica,

istruzione/formazione.

Mission

IPSAS Board

“Adoperarsi per l’interesse della collettività, sviluppando principi

contabili per il settore pubblico di elevata qualità e favorendo la

convergenza di principi nazionali ed internazionali, così da

migliorare la qualità e l’uniformità della rendicontazione contabile in

ogni parte del mondo”.

Public Interest Composizione

Committee • Standard Setter;

• Auditor privati e pubblici;

Consultation

• Rappresentanti professione contabile;

Advisory Group

• Docenti universitari, ecc.

MEF – RGS – SeSD

5

Iter di elaborazione di uno standard IPSAS

L’intero iter di elaborazione e approvazione di un nuovo standard è sottoposto a un processo

obbligatorio e formalizzato (c.d. “due process”) teso a garantire la trasparenza dei lavori e la

partecipazione, attraverso consultazioni pubbliche, di tutti i soggetti interessati.

«DUE PROCESS»

Consultation Exposure Approvazione Standard

paper draft (maggioranza 2/3)

9 - 18

Public Public

mesi

Consultation Consultation

Il Consultation paper (non è ancora uno standard) è un documento che tratta questioni di

principio che il Board intende preliminarmente sottoporre all’attenzione di tutti

pubblicandolo per almeno 4 mesi sul proprio sito internet per raccogliere commenti e rilievi

da parte di tutti i possibili soggetti interessati.

MEF – RGS – SeSD

6

IPSAS BOARD: PROGETTI IN DISCUSSIONE

2019 2020

Mar. Giu. Set. Dic. Mar.

IPSAS IPSAS IPSAS IPSAS IPSAS

Board Board Board Board Board

• Public Sector • Leases • Public Sector • Leases • Leases

Specific Financial • Revenue Specific Financial • Not-exchange • Public sector

Instruments • Not-exchange Instruments expenses measurement

• Leases expenses • Leases • Public sector • Infrastructure

• Revenue • Public sector • Revenue measurement assets

• Not-exchange measurement • Not-exchange • Infrastructure • Heritage

expenses expenses assets

• Public sector • Infrastructure • Heritage

measurement assets

• Heritage • Heritage

MEF – RGS – SeSD

7

EUROSTAT ed EPSAS Working Group

MEF – RGS – SeSD

8

EUROSTAT: Direttiva 2011/85/UE

Anche la CE ha evidenziato* l’importanza dell’adozione di sistemi di contabilità di tipo accrual,

sottolineando che questi non determinano l’abolizione o la sostituire dei sistemi di contabilità cash-

based, in particolare quando quest’ultima è utilizzata ai fini della redazione del budget e per il

controllo del rispetto dei limiti di utilizzo delle risorse pubbliche fissati nei budget medesimi.

«…gli Stati membri si dotano di sistemi di contabilità pubblica che coprono in modo

Art.3 completo e uniforme tutti i sotto-settori […] e contengono le informazioni […] per

generare dati fondati sul principio ACCRUAL al fine di predisporre i dati basati

sulle norme SEC 2010.»

Art.12 «[…] uniformità nelle norme e nelle procedure contabili nonché l’integrità

dei sistemi di raccolta ed elaborazione dei dati sottostanti.»

Art.13 «Gli Stati membri istituiscono meccanismi appropriati per il coordinamento tra tutti i

sotto-settori dell’amministrazione pubblica…»

Art.16

«La Commissione, entro il 31 dicembre 2012, valuta l’adeguatezza degli STANDARD

contabili internazionali applicabili al settore pubblico per gli Stati membri.»

* Relazione della Commissione Europea al Parlamento Europeo del 6.3.2013 - Verso

MEF –contabili

l'applicazione di standard RGS – SeSD

armonizzati per il settore pubblico negli Stati membri,

Idoneità degli IPSAS per gli Stati membri. 9

Move towards IPSAS

«La Commissione, entro il 31 dicembre 2012, valuta l’adeguatezza degli STANDARD

contabili internazionali applicabili al settore pubblico per gli Stati membri.»

Timing of definition and implementation

Standard directly applicable without

a. adjustments.

Standard that requires adjustments

b.

Standard that requires

c. substantial changes

0 1 2 3 4 5 6 Year

Definition Implementation

MEF – RGS – SeSD

10MS «accounting maturity» - Questionnaire

The "maturity" in the application of the IPSAS based accrual

accounting was measured, through a questionnaire, concerning the

following aspects:

Reporting Revenue

Consolidation Accrual and

expenses

Fixed assets

Employee

Intangible asset benefits

Inventories Provisions

Financial

instruments

MEF – RGS – SeSD

11MS «accounting maturity» - Results

…"maturity" in the application of the IPSAS based accrual accounting

Accounting

maturity Central State Local Social Funds

(AM)

Belgium, Cyprus,

Austria, Czech Czech Republic,

Czech Republic,

Republic, Denmark, Estonia, Finland,

Estonia, Finland,

HIGH Estonia, Finland, France, Ireland,

France, Lithuania,

AM ≥ 70% France, Latvia, Latvia, Lithuania,

Netherlands,

Slovak Republic, Malta, Portugal,

Portugal, Sweden

Spain, Sweden, UK Slovak Republic,

Sweden, UK

Bulgaria, Denmark, Austria, Belgium,

Belgium, Bulgaria,

MEDIUM Germany, Hungary, Bulgaria, Croatia,

Hungary, Ireland,

70%>AM Belgium, Spain Netherlands, Denmark, Hungary,

Poland, Portugal,

≥40% Poland, Romania, Ireland, Latvia,

Romania, Slovenia

Slovenia, Spain Poland, Spain

Cyprus, Germany,

Croatia, Cyprus,

Austria, Croatia, Greece, Italy,

LOW Germany, Greece,

Austria, Germany Greece, Italy, Luxembourg,

AM < 40% Italy, Luxembourg,

Luxembourg Romania, Slovak

Malta, Netherlands

Republic, Slovenia

MEF – RGS – SeSD

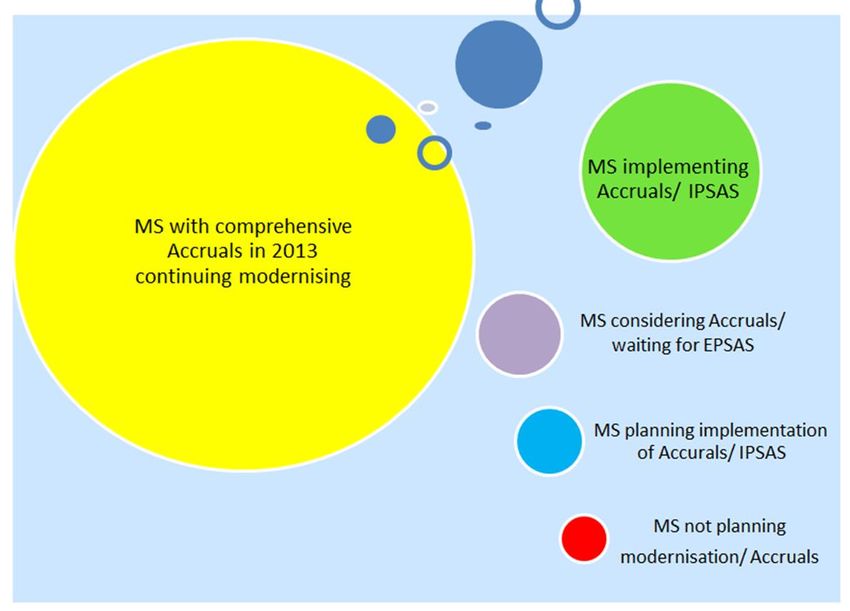

12MS «accounting maturity» - Central and Local

Government (2013)

Accounting maturity for

Member States

Proximity to IPSAS

Source: PwC Study on

behalf of Eurostat, 2013/14

MEF – RGS – SeSD

13State of the art - European context (2017)

MEF – RGS – SeSD

14Il percorso delineato da Eurostat

Eurostat ha istituito un Working Group per l’analisi degli IPSAS e la definizione di un EPSAS

Project.

Successivamente ha identificato due principali fasi per l’adozione degli EPSAS all’interno degli

Stati membri.

Fase 1 Fase 2

2020 2025

First First EPSAS

Preparation Transition

Accrual EPSAS transition

period period

OBS* OBS** period

-- Trasparenza e completezza del sistema ++

ELEMENTI ESSENZIALI

Contabilità per competenza: unico sistema generalmente accettato che fornisce un quadro

completo e attendibile della posizione finanziaria ed economica e del risultato di bilancio di una

PA.

L’applicazione del principio di competenza non può prescindere da una contabilità in partita

doppia.

Adozione di standard internazionali di contabilità pubblica IPSAS con opportuni adattamenti

(EPSAS).

* First

MEF Accrual

– RGS –Opening

SeSD Balance Sheet (Primo Bilancio di apertura a base Accrual)

** First EPSAS Opening Balance Sheet (Primo Bilancio di apertura a base EPSAS)

15EPSAS Working Group e Celle

2018 2019

Ott. Nov. Mag. Ott. Nov.

Cell on EPSAS EPSAS Cell on

Principles Working Working Principles EPSAS

related to Group Group related to Working

EPSAS EPSAS Group

Standards Lux Rome Standards

• L’EPSAS Working Group è affiancato da tre sottogruppi (Cell):

1. “EPSAS Cell on Governance Principles”;

2. “Cell on First-Time Implementation”;

3. “EPSAS Cell on Principles related to EPSAS standards”.

• Le Cell fungono da supporto tecnico per il lavoro del WG. Le prime due Celle hanno

completato i lavori elaborando due documenti tecnici*. L’ultima Cella, i cui lavori sono

ancora in corso, si occupata di definire il conceptual framework degli EPSAS.

*EPSAS First Time Implementation

MEF – RGS – SeSD

*Cell on principles related to EPSAS standards - Final Report

16EPSAS Issue papers

Chart of accounts Taxes

Employee Benefits Accounting for grants and other

transfers

Heritage assets

Discount rates

Infrastructure assets

Principled approach to

Intangible assets

disclosures

IPSAS options

Grants and other transfers

Military assets

Provisions, contingent assets/

Segment reporting liabilities, financial guarantees

Relief for smaller and less Loans and borrowings

risky entities

Notion of control

Social Benefits

Consolidation

Social contributions

Service concession

arrangements

MEF – RGS – SeSDWhat does EPSAS bring to politicians and policy

makers?

Financial management: not only about expenditure

High quality information: better management of public finances

Increased credibility of governments

Fiscal stability and sustainability

Economic value of the policies

MEF – RGS – SeSDItaly - Context

2009: Organic Budget Reform

Enhancing transparency of the public budgets

Reinforcement of cash accounting and budgeting system (!?)

Strengthening controls over expenditures

Harmonizing accounting systems across levels of governments

2011: Budgetary Frameworks Directive 2011/85/EU

2012: Constitutional reform: Introduction of the balanced budget principle

……and give back to the Central Government the power on accounting

legislation

2013: EPSAS Task Force (2016: EPSAS WG)

2016: The situation still remains heterogeneous so …. we asked for support (EC)

SRSS

2017: SRSS Project “Design of the accrual IPSAS/EPSAS based accounting reform

in the Italian public administration”

MEF – RGS – SeSDL’importanza della ricetta...

AS IS

TO BE

Legislazione frammentata

3 diversi PdC Quadro concettuale

3 diversi approcci Principi generali

Principi in continuo mutamento Standard (regole)

Matrice COFI-COEP Linee guida e manuali

principi generali=regole=principi applicati Formazione

IT: troppi applicativi IT: ERP

MEF – RGS – SeSD

20Accrual Accounting in Italy – History

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

The public finance and accounting reform:

Law 196/2009

Italian Reform implementation (various

secondary legislations)

Directive 85/2011 UE

MAIN STEPS

EUROSTAT working group

RGS/Academic working group

SRSS 1st Project ”Design of the accrual IPSAS/EPSAS

based accounting reform in the Italian public administration”

Italian Heritage standard Draft (IPSASB and

EPSAS WG)

EUROSTAT project on MCoA for accrual

accounting

Action Plan and Governance for accrual

accounting

Implementation new Governance

NEXT STEPS

Implementation Action Plan

SRSS 2nd Project ”Support for the implementation of

the accrual IPSAS/EPSAS based accounting”

SRSS 3rd Project (in progess: «Asset recognition and

evaluation»)

National activities

MEF – RGS – SeSD European projects 21Accounting scenario - current situation

Regional Governments

Regional Entities

Central Government

Line Ministries and Gov.al Entities

opther consitituonal Local Governments

Bodies

Health care (210)

SOEs

SOEs

SOEs

Full accrual, based on ITA GAAP (developed for private sector)

Full cash/commitments (v.1)

Predominantly cash/commintments (v.2) but with accrual information

Source: Italian Public Sector Accounting Outlook

Predominantly accrual largelly based on ITA GAAP Francesco Capalbo - IPSASB June 2019

MEF – RGS – SeSD

22Progetti RGS

MEF – RGS – SeSD

23Progettazione

1. Analisi e progettazione

SRSS – Fase I Eurostat - MCoA

2. Implementazione (SRSS – Fase II)

SRSS – Fase II

3. Monitoraggio e mantenimento

MEF – RGS – SeSD

24Progetto SRSS – Fase I

Studio della contabilità accrual a base IPSAS in Italia

1/18 9/18 12/18

Working visits

• Visite di studio in Stati Membri che hanno

già implementato una riforma accrual Gap analysis

(selezionati in collaborazione con Eurostat);

• Questionario preventivamente inviato allo • Analizza le differenze riscontrabili nei

stato membro; sistemi contabili in uso e il diverso grado di

“maturità contabile” dell’AP, in termini di

• Report sulle visite di studio.

formazione contabile, cornice normativa,

principi contabili, modelli di bilancio e

sistemi informatici.

Portugal

Belgium Action plan

• Technical Note: riporta i prerequisiti per la definizione

State of Hessen del piano d'azione utile all'implementazione di un

sistema di contabilità a base accrual IPSAS / EPSAS per

tutto il settore pubblico.

City-State of Hamburg

• Action Plan: identifica due ipotesi di governance, che

rappresentano la scelta strategica da operare per poter

Estonia avviare il processo di riforma. Il documento identifica

inoltre un’ipotesi di pianificazione delle due principali

Austria fasi della riforma (fase preparatoria e fase di prima

applicazione) che consentirebbero all’Italia di muoversi

in coerenza con le tempistiche definite a livello

MEF – RGS – SeSD comunitario (2020 e 2025).

25EC SRSS Technical support project

Working visits to analyze and understand

how accrual systems have been implemented

in the most advanced European countries

State of

Accrual accounting topics to be developed Austria Portugal Hessen / Estonia Belgium France UK

Hamburg

Conceptual (accrual principles, conceptual framework, etc..) ●● ●●● ●● ●●

Technical (recognition, recording, measurement, reporting) ●● ●● ●● ●● ●●●

Action plan (design the path towards the accrual accounting implementation plan) ●● ●● ●● ●

IPSAS (transition from accrual accounting to IPSAS: FTI e OBS) ●●

Relations with levels of government (transfers, etc..) ●●● ●●● ●●

Consolidation (techniques and reconciliation with others accounting systems) ●●● ●

Heritage (special focus on heritage) ●●● ●●● ●●●

IT (Infrastructure and software) ●●● ●● ●● ●●● ●● ●

Training (manuals, guidelines, training of trainers and trainees) ●●● ●●●

experience ●

interesting experience ●●

very interesting experience ●●●

MEF – RGS – SeSD

26Working visits – Countries Peculiarities

UNILEO ad hoc Unit 4 Landers and Accrual accounting Complex country IPSAS based

(standard setter) almost all since 2004 (multiculturalism Accrual Accounting

municipalities Accrual budgeting and multilingualism) since 2009

since 2017

3 kinds of Milestone: prudence Accounting Accrual reform 19 IPSASs fully impl.

accounting: principle managed by State process started in 6 IPSASs modified

budgetary, financial Agency the ’80s 7 IPSASs not impl.

and management

Risk matrix: three Accrual based on Ad hoc working Effective «Win win» approach

different systems Commercial code group for multidimensional

(private sector) accounting reform CoA

Multidimensional Hamburg: Accrual Conceptual Adaptation of Reform designed by

CoA accounting and Framework since IPSASs experts of MoF

budgeting 2006, before

IPSASB CF

Training (80.000 “Quick and dirty” Simple and single Accrual budgeting Guidelines and

people) approach CoA (only 1.200 handbooks are

items) essential

Reform process Hessen: Strong Intensive training Pragmatic approach

leads by objectives cooperation with (simplified methods

and not by IT Court of Audits of evaluation)

systems

MEF – RGS – SeSD

27Working visits – Countries Peculiarities

UNILEO ad hoc Unit 4 Landers and Accrual accounting Complex country IPSAS based

(standard setter) almost all since 2004 (multiculturalism Accrual Accounting

municipalities Accrual budgeting and multilingualism) since 2009

since 2017

3 kinds of Milestone: prudence Accounting Accrual reform 19 IPSASs fully impl.

accounting: principle managed by State process started in 6 IPSASs modified

budgetary, financial Agency the ’80s 7 IPSASs not impl.

and management

Risk matrix: three Accrual based on Ad hoc working Effective «Win win» approach

different system Commercial code group for multidimensional

(private sector) accounting reform CoA

Multidimensional Hamburg: Accrual Conceptual Adaptation of Reform designed by

CoA accounting and Framework since IPSASs experts of MoF

budgeting 2006, before

IPSASB CF

Training (80.000 “Quick and dirty” Simple and single Accrual budgeting Guidelines and

people) approach CoA (only 1.200 handbooks are

items) essential

Reform process Hessen: Strong Intensive training Pragmatic approach

leads by objectives cooperation with (simplified methods

and not by IT Court of Audits of evaluation)

systems

MEF – RGS – SeSD

28Working visits – Countries Similarities

• Reform steered by technicians with strong political

support

• Ad hoc governance unit supported by external experts

• Single and simple accounting system

• Cash data: more reliable and higher quality

• IPSASs as reference

• Single multidimensional CoA

• IT system based on SAP

• Reforms focused on objectives. IT is a tool and not a

driver

• Continuous and centralized training

MEF – RGS – SeSD

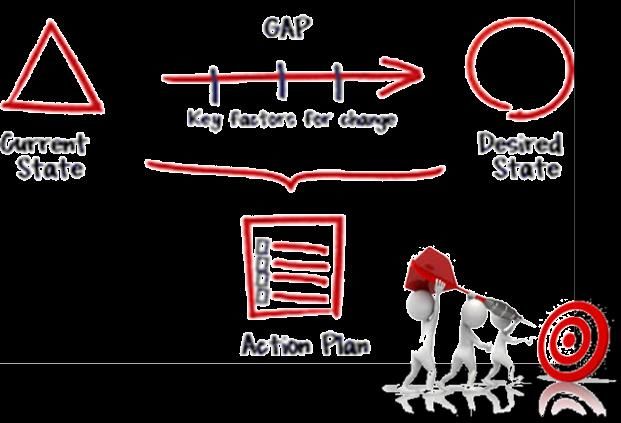

29GAP ANALYSIS

Gap analysis AMI list experts

After analysing the national context and identifying the distance between the accrual

models applied in the different sectors of the Italian public government and an accrual

model based on IPSAS / EPSAS, the gap analysis provided 9 useful recommendations.

Among these, special attention shall be given to the following:

# 1: Coordinate accounting reform actions by changing the governance approach to

accounting harmonization;

# 4: Clarify scope, objective and logic of budgetary accounting and financial

accounting as individual systems;

# 7: Define a new common chart of accounts aligned with best international practice

(regarding this point it’s started a EUROSTAT Project in order to define a key tool for an

effctive government accounting and reporting standards);

# 9: Be conscious of the requirements for IT, human resources, and financial

management systems, to successfully implement the accounting reform.

MEF – RGS – SeSD

30ACTION PLAN

The draft Action Plan envisages two macro-phases:

1. Preparatory phase, for the definition of a new accounting framework;

2. First Time Implementation (FTI) phase, for the first application of the

IPSAS/EPSAS.

MEF – RGS – SeSD

31ACTION PLAN – Governance model

PREPARATORY PHASE FIRST TIME IMPLEMENTATION

Conceptual Chart of

Governance Standard IT Training

Framework Accounts

The process of accounting harmonization and alignment with an IPSAS/EPSAS-based

financial accounting system cannot be carried out without an adequate governance

model.

The latter must respect (in line with the Principles underlying EPSAS

governance) the criteria of independence, professionalism, thus ensuring a process

of implementation of the reform without a representation constraint.

In order to meet the above mentioned need, two possible options can be pursued

through:

A. a standard setter Board EXTERNAL to the MEF-RGS, completely

independent;

B. a standard setter Board WITHIN the MEF-RGS, composed by non-RGS

members with Professional independence and Competence and capacity

In both cases, the Board should represent a synthesis of high-profile skills in the

field of accrual-based public accounting systems.

MEF – RGS – SeSD

32Model A: «External Standard Setter Approach»

This configuration provide for:

Technical Structure: responsible for

production, through studies and

researches, of the preparatory work

necessary for Standard Setter Board;

Standard Setter Board: assigned the

task of drafting the standards (and other

related documents), evaluating the

comments and opinions provided by

stakeholders, issuing the final version of

the standards (and related documents);

Institutional Stakeholder: assigned the

task of providing opinions on the draft of

the standard (and related documents). The

Court of Auditors and ISTAT will be

permanent members of the external

stakeholders’ advisory group from which

an opinion on the work of the Standard

Setter Board will be requested.

RGS Advisory Group: it has the task of

providing opinions on the standard draft

(and documents related);

IGB/IGEPA/IGEPA/IGF/IGESPES:

they support public administrations in the

application of principles and standards.

MEF – RGS – SeSD

33Model B: «Internal Standard Setter Approach»

This configuration provide for:

Technical Structure: it is composed

by external experts (at least 5 experts

who are chosen based on their different

accounting profiles), identified through

the same selection procedure applied

for the Standard Setter Board, and

coordinated by a representative of the

structure completely dedicated to the

reforming process;

Standard Setter Board: it should be

composed by a majority of non-RGS

members. It is established by

Determination of the State General

Accountant, after identifying its

members through a selection procedure

based on curricula by a special

Commission;

Institutional Stakeholders: the

same function and role of the previous

approach;

RGS Advisory Group: it has the task

of providing opinions on the standard

draft (and documents related);

Steering Committee: is constituted

by the State General Accountant, who

chairs, the RGS General Inspectors and

the General Director of the Research

Division.

MEF – RGS – SeSD

34Due

Process

Roma, May 2019

MEF – RGS – SeSD

35

GovernanceGovernance model

The governance model, inspired by an hypothesis of a model B set up by

EY, is finalized to introduce an accrual accounting system for the PS and:

• Is in line with the timeframe outlined at European level;

• Is consistent with the recommendations of the 'Action plan'

(EY-EC/SRSS);

• Is consistent and compatible with the “traditional” budgetary

accounting system (cash/commitments);

• Ensures a key role for RGS (keeping control).

The path outlined (characterized by a long test phase) should not interfere

with the ongoing reforming processes.

It will be consistent with the implementation path of IPSAS and EPSAS at

European level.

MEF – RGS – SeSD

36Progetto Eurostat

«Design a chart of accounts for the EPSAS/IPSAS based accrual

accounting»

• Ad ottobre 2018 è stato approvato da Eurostat il progetto c.d. CoA 2019,

finanziato da Eurostat nel quadro della Call for grants 2018 relativa alla

Modernisation of public sector accounting on an accruals basis in support of

EPSAS(1).

• Il progetto ha ad oggetto l’analisi, lo studio e l’elaborazione di un piano dei

conti multidimensionale coerente con una contabilità economico-

patrimoniale, quale elemento essenziale per la futura adozione degli IPSAS o

dei futuri EPSAS secondo il percorso delineato da Eurostat nell’ambito del

lavoro dell’EPSAS Working Group e relativo all’attuazione della Direttiva

85/2011/UE.

• Il progetto ha ufficialmente preso avvio in data 4 gennaio 2019 (grant

agreement 828828) ed è stato completato in data 1 ottobre 2019.

(1) Eurostat si pone l’obiettivo di fornire supporto finanziario agli SM con l’intento di modernizzare i sistemi contabili del

settore pubblico nell’ottica del principio accrual in vista della futura implementazione degli EPSAS al fine di rafforzare

la trasparenza finanziaria e l’armonizzazione contabile

MEF – RGS – SeSD

37Progetto Eurostat

ATTIVITA’ PARTNER TIMING

1 GAP ANALYSIS

• Approfondimento e studio dei requisiti

(Eurostat, FMI) Marzo 2019

• Analisi delle esperienze di altri stati membri

(es. Portogallo, Belgio, Francia, Estonia).

2 PIANO DEI CONTI E GLOSSARIO

Definizione di una struttura di piano dei conti

adatta e coerente con una contabilità Settembre 2019

economico-patrimoniale.

3 TAVOLE DI CORRELAZIONE Definizione delle

tavole di correlazione con la classificazione ESA Ottobre 2019

2010.

MEF – RGS – SeSD

38Progetto SRSS – Fase II

Progetto di AT per il supporto all’implementazione della contabilità

accrual a base IPSAS/EPSAS nella PA

Nell’ambito del programma SRSP 2019, la RGS ha presentato il progetto denominato

“Support for the implementation of the accrual IPSAS/EPSAS based accounting

in the Italian public administration”, naturale prosecuzione del progetto "Design of

the accrual IPSAS/EPSAS based accounting reform in the Italian public administration"

Il progetto ha ad oggetto le seguenti attività:

• Redazione (in bozza) degli standard ispirati agli IPSAS (o adozione degli EPSAS);

• Redazione di linee guida e manuali per l‘implementazione degli standard;

• Redazione del Quadro concettuale.

• Formazione per i formatori (contabilità accrual e IPSAS/EPSAS);

• Creazione di una piattaforma di e-learning per la formazione.

MEF – RGS – SeSD

39Contatti

Fabrizio Mocavini

fabrizio.mocavini@mef.gov.it

MEF – RGS – SeSD

40Puoi anche leggere