Trends and risks of the Italian financial system in a comparative perspective - 2022 July - Consob

←

→

Trascrizione del contenuto della pagina

Se il tuo browser non visualizza correttamente la pagina, ti preghiamo di leggere il contenuto della pagina quaggiù

Statistics and analyses Trends and risks of the Italian financial system in a comparative perspective July 2022

Congiuntura e rischi del sistema finanziario italiano in una prospettiva comparata Il presente Rapporto è stato curato da: Nadia Linciano (coordinatrice), Valeria Caivano, Daniela Costa, Francesco Fancello, Monica Gentile. Lucia Pierantoni ha contribuito alle analisi relative a mercato obbligazionario e banche italiane (Sezioni 3 e 5). Le opinioni espresse nel Report sono personali degli autori e non impegnano in alcun modo la CONSOB. Nel citare i contenuti del rapporto, non è pertanto corretto attribuirli alla CONSOB o ai suoi Vertici. La copia, la distribuzione e la riproduzione del presente Rapporto, in tutto o in parte, è soggetta a preventiva autorizzazione scritta da parte della CONSOB. Segreteria di redazione e progettazione grafica: Eugenia Della Libera e Lucia Pierantoni. Per informazioni e chiarimenti scrivere a: studi_analisi@consob.it This Report was prepared by Nadia Linciano (coordinator), Valeria Caivano, Daniela Costa, Francesco Fancello, Monica Gentile. Lucia Pierantoni contributed to the analysis relative to bond markets and Italian banks (Sections 3 and 5). The opinions expressed in this Report are the authors’ personal views and are in no way binding on CONSOB. Full or partial copying, distribution and reproduction of the Report is subject to prior written authorisation by CONSOB. Editorial secretary and graphic design: Eugenia Della Libera and Lucia Pierantoni. For information and clarifications write to: studi_analisi@consob.it Tipografia Eurosia Roma, luglio 2022.

Il Rapporto analizza la congiuntura e i rischi del sistema finanziario italiano nel confronto internazionale, avendo riguardo anche alle dinamiche che possono rilevare per il raggiungimento degli obiettivi istituzionali della CONSOB. The Report analyses trends and risks of the Italian financial system in a comparative perspective, also with regard to the developments that can affect the achievement of CONSOB remit. 3

Nel primo semestre del 2022 le prospettive di crescita globale sono state riviste al ribasso a fronte di molteplici fattori: l’invasione dell’Ucraina da parte della Russia; il riacutizzarsi della pandemia di COVID-19; la dinamica crescente dell’inflazione alimentata, nell’ultima parte del 2021, dal rialzo dei prezzi dei beni energetici e da alcune rigidità dell’offerta, e accentuata nel 2022 a seguito dello scoppio del conflitto in Ucraina. Alla luce di tali dinamiche inflattive, nell’Eurozona è in atto la graduale normalizzazione della politica monetaria, già in corso in altre economie avanzate. I tassi di interesse, mantenuti su livelli estremamente bassi negli ultimi anni, sono attesi pertanto in rapida ascesa. In parallelo, a sostegno della crescita e della transizione verde e digitale, prosegue l’attuazione dei programmi lanciati dalla Commissione europea con il NGEU. Tali misure si associano a iniziative tese a mitigare gli scenari di recessione che si prefigurano soprattutto per i paesi connotati da forte dipendenza da fonti energetiche fossili e da vulnerabilità preesistenti, legate ad esempio a elevati livelli di debito pubblico e privato. I mercati finanziari delle economie più esposte al peggioramento del quadro macroeconomico hanno registrato tensioni significative. Dall’inizio dell’anno gli indici azionari S&P500 e EuroStoxx50 hanno perso entrambi il 20% circa, registrando al contempo un rilevante incremento della volatilità. Per quanto riguarda il mercato italiano, nel primo semestre del 2022 il Ftse Mib ha segnato una diminuzione del 22%, superiore a quella rilevata per le altre maggiori economie dell’Eurozona; la contrazione dei corsi è stata disomogenea tra settori, risultando più intensa nei comparti tecnologico (-30%) e bancario (-21%). Anche i mercati secondari dei titoli pubblici nell’area euro hanno registrato tensioni crescenti, con rialzi nei rendimenti che, rispetto all’inizio dell’anno, sono saliti di oltre il 2% in Italia, e con un netto incremento della volatilità, che a fine giugno 2022 ha raggiunto i massimi dal 2014. Analogo andamento si osserva nel mercato secondario dei titoli corporate, dove i rendimenti delle obbligazioni emesse sia dalle banche sia dalle imprese non finanziarie hanno sperimentato una crescita costante dall’inizio dell’anno. In prospettiva, il ciclo economico globale sperimenterà un deterioramento la cui portata sarà disomogenea tra aree e settori produttivi, anche in funzione dell’impatto dell’elevata inflazione e dell’aumento dei tassi di interesse. Le società non finanziarie e le banche, che nel 2021 hanno mostrato condizioni reddituali e patrimoniali in netto miglioramento, potrebbero vedere accentuate, nel medio termine, le proprie vulnerabilità, a fronte dei riflessi negativi del mutato contesto di riferimento sul costo del debito e sulla qualità del credito. Con specifico riferimento all’Italia, ulteriori criticità potrebbero emergere in relazione alle esposizioni delle banche verso i paesi coinvolti nel conflitto russo-ucraino, al calo del commercio estero e alla difficoltà di ridurre la dipendenza energetica dalla Russia in tempi brevi. Il ridimensionamento delle aspettative di ripresa economica e l’incertezza connessa agli sviluppi geopolitici in corso potranno innescare ulteriori tensioni nei mercati azionari e obbligazionari nei prossimi mesi dell’anno. 4

In the first half of 2022, the global economic outlook has been revised downwards in the wake of multiple factors: Russia's invasion of Ukraine; the resurgence of the COVID-19 pandemic; and rising inflation. In the Eurozone, the gradual normalisation of monetary policy, already under way in other advanced economies, is ongoing as a result of the significant rise in inflation, which was fuelled by the rise in energy prices and by some supply rigidities in the latter part of 2021, and finally amplified by the war in Ukraine in 2022. Interest rates, kept at extremely low levels in recent years, are therefore expected to rise rapidly. In order to support growth and accelerate the green and digital transition, the implementation of programmes launched by the European Commission with the NGEU continues. These measures are coupled with initiatives aimed at mitigating the recessionary scenarios that are foreseen especially for countries characterised by high dependence on fossil energy sources and pre-existing vulnerabilities, e.g. related to high levels of public and private debt. The financial markets of the economies most exposed to the deterioration of the macroeconomic scenario have experienced significant turbulences. Since the beginning of the year, the S&P500 and EuroStoxx50 stock indices have both lost around 20%, while showing a significant increase in volatility. As regards the Italian market, in the first half of 2022, the Ftse Mib fell by 22%, more than the drop observed in the other major Eurozone economies; the fall in stock prices was uneven across sectors, being more marked in the technology (-30%), banking (-21%). Secondary markets for government bonds in the euro area also experienced growing tensions, with yields rising by more than 2% in Italy compared to the beginning of the year, and with a sharp increase in volatility, which at the end of June 2022 reached its highest level since 2014. A similar trend can be observed in the secondary market for corporate debt instruments, where yields on bonds issued by both banks and non-financial companies have experienced steady growth since the beginning of the year. The expected worsening of the global economic outlook will be uneven across regions and sectors, also depending on the impact of high inflation and rising interest rates. Non-financial corporations and banks, which in 2021 markedly improved their profitability and capital adequacy, could experience increased vulnerabilities in the medium term, in the wake of the negative impact of this new economic environment on the cost of debt and credit quality. With specific reference to Italy, further issues could emerge in relation to banks' exposures to countries involved in the Russian-Ukrainian conflict, the drop in foreign trade, and the difficulty of reducing energy dependence on Russia in the short term. A further worsening in the expectations about economic growth and the uncertainty surrounding geopolitical developments may trigger further tensions in equity and bond markets in the coming months of the year. 5

HIGHL -20% -22% energy -2% technology -30% travel&leisure +2% banking -21% manufacturing -18% index performance -19% 2022 real GDP estimates +2.7% +2.6% average revisions estimates -1.5% -1.6% inflation rate in June 2022 +8.6% +8.5% of which linked to food and energy prices 6.4% 6.6% public debt to GDP 95% 148% private debt to GDP 172% 116% GOVT 3.3% BANKS 3.9% NFCs 3.8% issuance Jun-22 7% maturing Dec-23 22% gross issuance bank -28% NFCs +32% 6

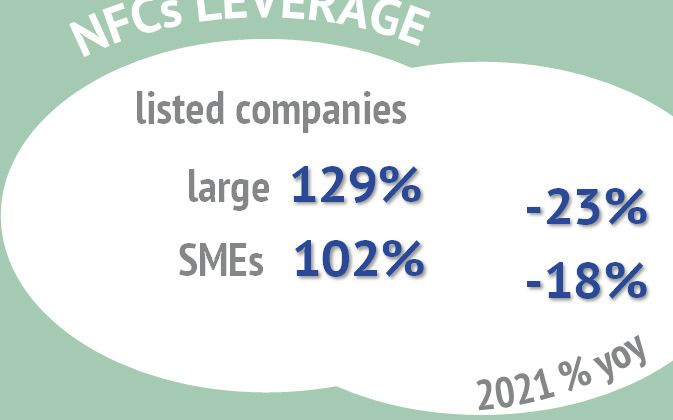

IGHTS listed companies large 129% -23% SMEs 102% -18% listed companies large +44% listed companies SMEs +14% large 11% SMEs 3% listed companies large 3% SMEs 1% 39% 43% gas import from Russia 58% 59% gas in storage total disbursement targets to Italy achieved 46 € bnl 110 out of 191.5 out of 1,172 23 €bln 0.8% total assets 26% large European bank exposures domestic govt bonds 10% total assets RoRWA 1% NPL ratio 3% CET1 ratio 15% 7

SOMMARIO Focus Energy dependence and trade with Russia 15 European support measures and national plans 17 Non-financial listed SMEs 65

1. Quadro macroeconomico Macroeconomic landscape 10 2. Mercati azionari Equity markets 34 3. Mercati obbligazionari Bond markets 48 4. Società non finanziarie Non-financial corporations 60 5. Banche Banks 76

Quadro macroeconomico Macroeconomic landscape

Attività economica Indicatori di incertezza e di fiducia Occupazione e inflazione Politica monetaria e fiscale Economic activity Indicators of uncertainty and economic sentiment Unemployment and inflation Monetary and fiscal policy

CONSOB Congiuntura e rischi del sistema finanziario italiano in una prospettiva comparata - 2022 Nei primi mesi del 2022 le prospettive In the first months of 2022, the di crescita delle maggiori economie economic outlook of major advanced avanzate sono state riviste al ribasso per countries deteriorated due to the effetto dell’impatto atteso del conflitto in expected impact of the conflict in Ukraine Ucraina sia sulla dinamica dell’inflazione on both inflation and foreign trade (in sia sul commercio estero (alla luce delle light of sanctions imposed on Russia). The sanzioni imposte alla Russia). I paesi con countries with the largest energy una maggiore dipendenza energetica dependence on Russia experienced the dalla Russia hanno registrato le correzioni largest downward corrections (Fig. 1.1 – più ampie (Fig. 1.1 – Fig. 1.2). Fig. 1.2). Gli sviluppi geopolitici ed economici Ongoing geopolitical and economic in atto alimentano un’incertezza developments are fuelling uncertainty, crescente, soprattutto in Europa, e un particularly in Europe, and a marked deciso calo degli indici di fiducia, decline in confidence indices, reversing interrompendo le tendenze positive the positive trends recorded the previous registrate l’anno precedente. Continua a year. The evolution of the COVID-19 pesare inoltre l’evoluzione della pandemia pandemic is still weighing heavily, with di COVID-19, che nel mese di giugno ha the significant rise in infections visto una crescita significativa dei contagi experienced in June in the context of a a fronte di una contestuale rimozione concomitant removal of the restrictive delle misure restrittive adottate negli measures adopted in recent years in all ultimi anni in tutti i maggiori paesi major Eurozone countries (Fig. 1.3 – dell’area euro (Fig. 1.3 – Fig. 1.7). Fig. 1.7). L’inflazione, che già nel 2021 risul- Inflation, already on the rise in 2021 tava in aumento per effetto della ripresa due to the recovery of global demand for della domanda globale dei beni energetici energy goods and some supply rigidities, e di alcune rigidità nell’offerta, ha rag- reached new highs in the euro area and giunto i massimi nell’area euro e in Italia Italy in June 2022, when it rose to 8.6% nel mese di giugno 2022, quando si è por- and 8.5%, respectively. The surge in the tata rispettivamente all’8,6% e all’8,5%. Al prices of commodities is accountable for rialzo dei prezzi dei beni energetici e dei an increase in the overall index of 6.4% in beni alimentari è riferibile un incremento the euro area and 6.6% in Italy. dell’indice generale pari al 6,4% nell’area Commodities that experienced the euro e al 6,6% in Italia. Tra le materie greatest upturns during 2022, and prime che hanno registrato i maggiori particularly after the outbreak of the rialzi nel corso del 2022, e in particolare conflict in Ukraine, include natural gas, dopo lo scoppio del conflitto in Ucraina, coal and nickel, while agricultural goods sono compresi il gas naturale, il carbone e include wheat and maize (Fig. 1.8 – il nickel, mentre tra i beni agricoli si anno- Fig. 1.10). verano grano e mais (Fig. 1.8 – Fig. 1.10). 12

QUADRO MACROECONOMICO A fronte delle aspettative di ripresa Given the expectations of economic economica (poi riviste al ribasso come recovery (later revised downward as ricordato prima) e della dinamica mentioned earlier) and inflationary inflazionistica, la BCE ha annunciato la pressures, the ECB announced the gradual riduzione graduale, a partire dai primi reduction, starting in early 2022, of net mesi del 2022, degli acquisti netti di purchases of financial assets under the attività finanziarie nell’ambito delle ope- unconventional operations launched in razioni non convenzionali avviate negli previous years. Purchases under the PEPP anni precedenti. Gli acquisti nell’ambito (pandemic emergency purchase program) del PEPP (pandemic emergency purchase were discontinued in March, although programme) sono stati interrotti a marzo, those under the APP (asset purchase sebbene nei mesi successivi siano program initiated in 2015) were slightly lievemente aumentati quelli nell’ambito increased in the following months, in dell’APP (asset purchase programme order to meet the announced graduality. avviato nel 2015), al fine di rispettare In June, the ECB also announced the l’annunciata gradualità nella riduzione discontinuation of net purchases of degli acquisti. A giugno la BCE ha securities under the APP as of July 2022. annunciato anche l’interruzione degli However, the total amount of securities acquisti netti di titoli nell’ambito dell’APP held by the ECB for monetary policy a partire da luglio 2022. L’ammontare di purposes remains high and amounted to titoli complessivamente detenuti dalla €4,957 billion at the end of June 2022 (of BCE ai fini della politica monetaria resta which 448 billion represented by Italian tuttavia elevato e pari a 4.957 miliardi di government bonds; Fig. 1.11). euro a fine giugno 2022 (di cui 448 miliardi rappresentati da titoli pubblici italiani; Fig. 1.11). Con riferimento all’andamento dei With regard to the main public principali parametri di finanza pubblica, finance indicators in the Eurozone, in nel 2021 il rapporto tra debito pubblico e 2021 the ratio of public debt to GDP PIL è lievemente diminuito nell’area euro, slightly decreased in the euro area to 95%, portandosi al 95%, pur rimanendo ai while remaining at historical highs in Italy massimi storici in Italia (148%), Francia e (148%), France and Spain. The very low Spagna. Il livello molto basso dei tassi di level of interest rates over the last 10 interesse negli ultimi 10 anni ha years has, however, contributed to a contribuito ad abbassare notevolmente le significant reduction in interest expenses spese per interessi nelle maggiori in all countries considered (from 5% of economie dell’Eurozona: in Italia, in GDP in 2007 to 3% in 2021 in Italy). The particolare, sono calate dal 5% del PIL nel European Commission most recent 2007 al 3% nel 2021. Le più recenti forecasts point to an improvement in previsioni della Commissione europea public accounts in 2022, with both debt 13

CONSOB Congiuntura e rischi del sistema finanziario italiano in una prospettiva comparata - 2022 indicano un miglioramento dei parametri and deficit as a share of GDP falling in all di finanza pubblica nel 2022, con un calo major countries (Fig. 1.12 - Fig. 1.13). dell’incidenza sia del debito sia del deficit rispetto al PIL in tutti i maggiori paesi (Fig. 1.12 - Fig. 1.13). Nel 2021, il debito privato, riferito sia In 2021, private debt, both household alle famiglie sia alle imprese, ha registrato and corporate, declined slightly in the una lieve diminuzione nelle principali major Eurozone economies, following the economie dell’Eurozona, dopo l’incremen- increase experienced in 2020; Italy to sperimentato nel 2020; l’Italia continua continues to be characterized by values a caratterizzarsi per valori notevolmente significantly lower than those of other inferiori rispetto a quelli degli altri paesi countries (Fig. 1.14). (Fig. 1.14). 2022 GDP (expected) 2021 GDP Italy 2.6 6.6 area euro 2.7 5.3 world 3.3 5.9 14

QUADRO MACROECONOMICO ENERGY DEPENDENCE AND TRADE WITH RUSSIA La Russia rappresenta il primo paese Russia is the leading net exporter of esportatore netto di gas naturale (con una natural gas (with a share of nearly 23% of quota pari a quasi il 23% delle esporta- global exports), the second largest net zioni globali), il secondo paese esportato- exporter of oil (13% of the global figure), re netto di petrolio (13% del dato globale) and the third largest country with regard e il terzo paese con riferimento al carbone to coal (with a 15% share). Oil, natural gas (con una quota del 15%). Petrolio, gas and coal cover 85% of global energy naturale e carbone coprono l’85% del needs, with slightly lower values in fabbisogno energetico globale, con valori advanced economies, in many cases due lievemente più bassi nelle economie to the wider reliance on nuclear energy avanzate, in molti casi grazie al maggior (Fig. 1.15). ricorso all’energia nucleare (Fig. 1.15). Lo scoppio del conflitto in Ucraina ha The outbreak of the conflict in avuto un impatto significativo sulle pro- Ukraine had a significant impact on the spettive di crescita delle economie euro- growth prospects of European economies pee anche a causa della elevata dipenden- also due to the high dependence on za dalla Russia nell’approvvigionamento Russian energy resources. di risorse energetiche. Over the past decade, the EU's imports of Nell’ultimo decennio le importazioni di natural gas from Russia have grown up to gas naturale dalla Russia da parte 39% of the total in 2020. The figure dell’Unione europea sono cresciute, reaches 65% and 43% respectively for raggiungendo nel 2020 il 39% del totale. Germany and Italy, which among the Il dato si attesta al 65% e al 43% largest Eurozone countries record the rispettivamente per Germania e Italia tra i highest dependence on Russian gas maggiori paesi dell’area euro con la più (Fig. 1.16). elevata dipendenza dal gas russo (Fig. 1.16). Negli ultimi anni, inoltre, l’Unione Moreover, in recent years, the EU has europea ha progressivamente ridotto la progressively reduced its domestic natural produzione interna di gas naturale (passa- gas production (from 24% of the total in ta dal 24% del totale nel 2015 al 9% nel 2015 to 9% in 2021). In 2022, following 2021). Nel 2022, a seguito dell’invasione the invasion of Ukraine, efforts to reduce dell’Ucraina, gli sforzi per ridurre la dipen- the EU's energy dependence on Russia denza energetica della UE dalla Russia si intensified, also in the wake of the new sono intensificati, anche sulla scia del REPowerEU plan published by the nuovo piano REPowerEU pubblicato dalla European Commission (see next section 15

CONSOB Congiuntura e rischi del sistema finanziario italiano in una prospettiva comparata - 2022 Commissione europea a maggio 2022 (si ‘European support measures and national veda la sezione successiva ‘Misure di plans’), with volumes of natural gas sostegno europee e piani nazionali’), con imported from Russia in the first half of un calo di oltre il 37% dei volumi di gas the year falling by more than 37% naturale importati dalla Russia nella prima compared to the previous year (Fig. 1.17 - metà dell’anno rispetto a quelli del Fig. 1.18). precedente anno (Fig. 1.17 - Fig. 1.18). Con riferimento specifico all’Italia, le Specifically, in Italy, energy sources fonti di energia utilizzate nei settori used in the manufacturing and service manifatturiero e dei servizi provengono da sectors come from energy goods imported beni energetici importati dalla Russia per from Russia for about 29%, while those il 29% circa mentre quelle utilizzate nel used in the residential sector (e.g. for settore residenziale (per riscaldamento, heating, cooling and cooking) refer to raffrescamento e impiego in cucina) sono Russian sources for 28% of the total. In riferibili a fonti russe per il 28%. Si addition, 24% of the energy goods related aggiunge, inoltre, la quota di beni to the production of electricity are energetici di origine russa relativa alla imported from Russia (Fig. 1.19). produzione di elettricità, pari al 24% circa del totale (Fig. 1.19). Con riferimento al commercio estero With regard to the EU's external trade, della UE, nell’ultimo anno sono cresciute imports from Russia grew last year and the le importazioni dalla Russia e si è ampliato negative balance of net exports widened. il saldo negativo delle esportazioni nette. However, this dynamic can be attributed Tale dinamica è tuttavia riconducibile a to valuation effects related to the sharp effetti di valutazione connessi al netto rise in the prices of energy goods. As rialzo dei prezzi dei beni energetici. regards the composition of trade between Quanto alla composizione del commercio the EU and Russia, manufacturing goods, tra UE e Russia, tra i beni esportati dalla machinery, and transport equipment UE predominano beni manifatturieri, predominate among the goods exported macchinari e mezzi di trasporto mentre tra by the EU, while energy goods and raw quelli maggiormente importati rientrano materials are among the most imported. A beni energetici e materie prime. Analoga similar composition is observed in Italy, composizione si osserva in Italia che vede where Russia is the 14th largest export nella Russia il 14° mercato di esportazione market (accounting for 1.5% of total (a cui è riferibile l’1,5% delle esportazioni exports) and the 7th largest import market complessive) e il 7° mercato di (accounting for 4% of total imports; importazione (a cui è riferibile il 4% del Fig. 1.20 – Fig. 1.21). totale; Fig. 1.20 – Fig. 1.21). 16

QUADRO MACROECONOMICO EUROPEAN SUPPORT MEASURES AND NATIONAL PLANS Il peggioramento delle prospettive The deteriorating economic outlook economiche e le perturbazioni del mer- and global energy market disruptions cato energetico globale causate dall'inva- caused by the Russian invasion of Ukraine sione russa dell'Ucraina hanno ulterior- have further raised the attention of policy mente innalzato l’attenzione dei policy makers on economic growth and makers su crescita economica e transizione transition to a sustainable development verso un modello di sviluppo sostenibile. model. A key policy tool in the European Uno strumento di policy fondamentale in arena is the Next Generation EU (NGEU) ambito europeo è il programma Next program and, in particular, the Recovery Generation EU (NGEU) e, in particolare, il and Resilience Facility (RRF), aimed at Recovery and Resilience Facility (RRF), making EU countries more resilient. The teso a rendere i paesi dell’Unione europea RRF is, in fact, at the heart of the più resilienti. Il RRF è, infatti, al centro implementation of the plan launched by dell'attuazione del piano lanciato dalla the European Commission and called Commissione europea e denominato REPowerEU, based on three cornerstones: REPowerEU, basato su tre punti cardine: energy saving, diversification in energy risparmio energetico, diversificazione sources, and acceleration of renewable nell’approvvigionamento e accelerazione energy (Fig. 1.23). delle energie rinnovabili (Fig. 1.23). diversifying away saving from fossil fuels energy 300 billions of euro 225 loans 75 grants massive investment in renewable energy La Commissione europea reperirà i The European Commission will fund fondi necessari a finanziarie NGEU sul NGEU through a diversified financing mercato dei capitali tramite una strategia strategy on capital markets, including the di finanziamento diversificata, che include issuance of €250 billion of green bonds (of l’emissione di obbligazioni green per un which €23 billion has already been ammontare pari a 250 miliardi di euro (di issued). Italy will be the largest beneficiary cui 23 miliardi già emesse). L’Italia sarà il of these issues, followed by Spain and maggior beneficiario di queste emissioni, France (Fig. 1.24). seguita da Spagna e Francia (Fig. 1.24). 17

CONSOB Congiuntura e rischi del sistema finanziario italiano in una prospettiva comparata - 2022 Alla data del presente Rapporto tutti i As of the date of this Report, all EU paesi dell’UE hanno presentato il proprio countries have submitted their own Piano nazionale di ripresa e resilienza National Recovery and Resilience Plans (PNRR), che la Commissione europea ha (RRPs), which the European Commission già approvato in 25 casi. Gli Stati membri has already approved in 25 cases. Overall, hanno destinato, nel complesso, più del Member States have allocated more than 40% della spesa prevista nei propri Piani 40% of the planned spending to green alla transizione sostenibile e il 26% alla transition and about 26% to digital transizione digitale (prevedendo quindi transition (thus providing for higher quote superiori a quelle indicate dalla shares than those indicated by the Commissione europea e pari, rispettiva- European Commission and amounting to, mente, a 37% e 20%; Fig. 1.25 - Fig. 1.26). respectively, 37% for and 20%; Fig. 1.25 - Fig. 1.26). L’attuazione del PNRR rappresenta The implementation of the RRP is per l’Italia un percorso obbligato per pro- essential for Italy to promote growth and muovere la crescita e sostenere il maggior sustain the increased public debt debito pubblico accumulato negli anni accumulated over the past years and passati e durante la pandemia. Il 13 agosto during the pandemic. On 13 August 2021, 2021 la Commissione europea, a seguito the European Commission, following the della valutazione positiva del PNRR positive assessment of the Italian RRP, italiano, ha erogato all'Italia 24,9 miliardi disbursed €24.9 billion in pre-financing di euro di fondi a titolo di prefinan- funds to Italy (including 8.957 billion in ziamento (di cui 8,957 miliardi a fondo grants and 15.937 billion in loans), perduto e 15,937 miliardi in prestiti), pari representing 13% of the total amount al 13% dell'importo totale stanziato a allocated to the country. On 13 April 2022, favore del Paese. Il 13 aprile 2022, la the European Commission paid Italy the Commissione europea ha versato all'Italia first instalment amounting to €21 billion la prima rata da 21 miliardi di euro (10 (10 billion in grants and 11 billion in miliardi di sovvenzioni e 11 miliardi di loans), following the achievement of 51 prestiti) a seguito del raggiungimento di targets under the Italian Plan by 31 51 obiettivi previsti dal Piano italiano December 2021, measured through entro il 31 dicembre 2021, misurati attra- specific goals both qualitative (so-called verso specifici traguardi sia qualitativi (i milestones, e.g., legislation adopted or cosiddetti milestones, ad esempio la legi- information systems fully operational) and slazione adottata o la piena operatività dei quantitative (so-called targets, e.g., km of sistemi informativi) sia quantitativi (i railways built, number of students cosiddetti targets, ad esempio chilometri completing education). di ferrovie costruite, numero di studenti che hanno completato la formazione). 18

QUADRO MACROECONOMICO Secondo le rilevazioni della Commissione According to the European Commission, as europea alla data del 15 dicembre 2021 in of 15 December 2021, on average, about media circa il 10% di tutti gli obiettivi 10% of all targets under the Italian Plan previsti dal Piano italiano sono stati have been achieved (Fig. 1.27). raggiunti (Fig. 1.27). Il pagamento della prima rata del The payment of the first instalment of PNRR italiano (il cui importo è maggiore the Italian RRP (which is larger than that di quello ricevuto finora da principali Stati received so far by major Member States) is membri) rappresenta un ulteriore a further step in the implementation of the passaggio nel percorso di attuazione degli investments and reforms envisaged by the investimenti e delle riforme previsti dal Italian Plan (Fig. 1.28). Piano italiano (Fig. 1.28). Rimangono rilevanti i passaggi da The steps to be taken and the compiere e le scadenze che l’Italia deve deadlines that Italy must meet in the rispettare nei prossimi mesi. Entro il 30 coming months remain relevant. By 30 giugno 2022, per ottenere il versamento June 2022, in order to qualify for the della seconda rata di esborsi (formalmente second instalment of disbursements, richiesta il 29 giugno) il nostro Paese (formally requested on 29 June), our dovrà dimostrare di aver raggiunto 45 country will have to deliver 45 targets obiettivi relativi a tutte le missioni del (related to all the missions of the Italian Piano italiano (ad eccezione della Plan (with the exception of mission 3 on missione 3 sulla mobilità sostenibile) e, in sustainable mobility) and, in particular, particolare, le macroaree concernenti the macro-areas concerning digitalisation digitalizzazione (14 obiettivi), rivoluzione (14 targets), green revolution and verde e transizione ecologica (14 obiettivi) ecological transition (14 targets) that will che richiederanno maggiori sforzi. Inoltre, require greater efforts. In addition, 100 per il conseguimento dei restanti obiettivi European deadlines will have to be del Piano italiano entro la fine del 2022 achieved by the end of 2022, rising to 476 dovranno essere rispettate 100 scadenze by 2026 (more than 80% of which have yet europee, che salgono a 476 entro il 2026 to be initiated) and including complex (di cui più dell’80% ancora da avviare) e reforms such as those on public che includono riforme complesse come procurement, the judiciary system, and quelle su appalti pubblici, sistema public administration (Fig. 1.29). giudiziario e pubblica amministrazione (Fig. 1.29). 19

CONSOB Trends and risks of the Italian financial system in a comparative perspective - 2022 List of figures 1.1 Revisions in real GDP growth forecasts for 2022 in the main advanced countries 22 1.2 Unemployment and activity rate in the euro area 22 1.3 Economic policy uncertainty indicators in the US and in Europe 22 1.4 PMI indexes in the main euro area countries 23 1.5 Sentiment indicators in the euro area 23 1.6 COVID-19 confirmed cases in the main euro area countries 23 1.7 COVID-19 Government Response Stringency Index in the main euro area countries 24 1.8 Inflation rate in the euro area 24 1.9 Drivers of inflation in Italy and in the main euro area countries 24 1.10 Trends in commodities prices 25 1.11 Net purchases of securities by the ECB 25 1.12 Trends in public debt and interest expenses in the main euro area countries 25 1.13 Public debt and deficit to GDP ratio in the main euro area countries 26 1.14 Private debt to GDP ratio in the main euro area countries 26 1.15 Energy consumption by source in selected countries in 2020 27 1.16 Natural gas imports from Russia 27 1.17 EU sources of natural gas and volumes imported from Russia in 2021 and 2022 27 1.18 Natural gas storage in Europe 28 1.19 Italian electricity production by source and reliance on Russian imports by sectorial end-uses 28 1.20 Trade of EU with Russia over time 28 1.21 Composition of imports and exports of EU and Italy with Russia 29 1.22 Italian main countries of imports and exports 29 20

MACROECONOMIC LANDSCAPE 1.22 REPowerEU: actions and additional investments 30 1.23 NextGenerationEU green bonds eligible amount 30 1.24 Recovery and resiliency plans (RRPs) endorsed by the European commission 30 1.25 Twin transitions: climate neutrality and digital transitions 31 1.26 RRF Commission’s disbursements (1st payment) per Member State 31 1.27 Italy Policy Pillars: milestones and targets achieved 31 1.28 Italian PNRR deadlines 32 21

CONSOB Trends and risks of the Italian financial system in a comparative perspective - 2022 Fig. 1.1 – Revisions in real GDP growth forecasts for 2022 in the main advanced countries before war after war 2022 real GDP growth forecasts World 3.3% 4.5% US 3.0% 4.2% China 4.5% 5.1% UK 3.6% 4.7% Euro area 2.7% 4.2% Italy 2.6% 4.2% Germany 1.8% 4.2% France 2.6% 3.8% Spain 4.3% 5.6% Source: calculations on OECD, IMF and European Commission data. Figure refers to average values of GDP forecasts published in OECD Economic Outlook June 2022, IMF World Economic Outlook April 2022 and European Commission Spring Forecasts May 2022 and Summer Forecasts July 2022 for euro area countries only. Fig. 1.2 – Unemployment and activity rate in the euro area euro area Italy unemployment rate (monthly data up to May 2022) activity rate (quarterly data up to Q1 2022) 14% 76% 12% 72% 10% 68% 8% 64% 6% 60% 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Source: European Commission DG - ECFIN, Eurostat, Istat. Figure on the left reports the unemployment rate as a percentage of active population; time series are seasonally adjusted. Figure on the right reports the activity rate computed as the ratio between the workforce (employed and unemployed) and population aged 15 years or more. Fig. 1.3 – Economic policy uncertainty indicators in the US and in Europe (monthly data up to May 2022) US euro area Italy 600 300 500 250 400 200 300 150 200 100 100 50 0 0 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Source: Economic Policy Uncertainty Index. The indicators are computed by counting the number of newspaper articles containing the terms uncertain or uncertainty, economic or economy, and one or more policy-relevant terms. For the US the newspapers considered are USA Today, the Miami Herald, the Chicago Tribune, the Washington Post, the Los Angeles Times, the Boston Globe, the San Francisco Chronicle, the Dallas Morning News, the Houston Chronicle, and the WSJ. For the European index the newspapers considered are Le Monde and Le Figaro for France, Handelsblatt and Frankfurter Allgemeine Zeitung for Germany, Corriere Della Sera and La Stampa for Italy, El Mundo and El Pais for Spain, and The Times of London and Financial Times for the United Kingdom. 22

MACROECONOMIC LANDSCAPE Fig. 1.4 – PMI indexes in the main euro area countries (monthly data up to June 2022) Spain France Germany Italy services manufacturing 70 70 60 60 50 50 40 40 30 30 20 20 10 10 0 0 2017 2018 2019 2020 2021 2022 2017 2018 2019 2020 2021 2022 Source: Refinitiv Datastream. Fig. 1.5 – Sentiment indicators in the euro area (monthly data up to June 2022) current general consumer confidence own family economic conditions (current and future) future current economic conditions future economic conditions (own family and Italy) (own family and Italy) Italian economic conditions (current and future) retail investor market sentiment in the euro area confidence indicator in Italy 80 170 40 140 0 110 -40 80 -80 50 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Source: Refinitiv Datastream and Istat. In the left figure retail investor Sentix Sentiment Indicator is reported. Fig. 1.6 – COVID-19 confirmed cases in the main euro area countries (daily data up to 30 June 2022; cases per millions) France Germany Spain Italy 6,000 5,000 4,000 3,000 2,000 1,000 0 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun 2020 | 2021 | 2022 Source: Our World in Data within the Oxford Martin Programme on Global Development at the University of Oxford and in partnership with the Global Change Data Lab; https://ourworldindata.org/covid-cases. 23

CONSOB Trends and risks of the Italian financial system in a comparative perspective - 2022 Fig. 1.7 – COVID-19 Government Response Stringency Index in the main euro area countries (daily data up to 30 June 2022) France Germany Spain Italy 100 80 60 40 20 0 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun 2020 | 2021 | 2022 Source: Our World in Data within the Oxford Martin Programme on Global Development at the University of Oxford and in partnership with the Global Change Data Lab. https://ourworldindata.org/grapher/covid-stringency-index. Fig. 1.8 – Inflation rate in the euro area (growth rate in percentage values; quarterly data) euro area Italy total inflation core inflation 8% 5% 6% 4% 4% 3% 2% 2% 0% 1% -2% 0% 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 Source: Oxford Economics. Dot lines represent forecasts. Core inflation does not include food and energy. Fig. 1.9 – Drivers of inflation in Italy and in the main euro area countries food energy other Italy June 2022 1.9% 2.2% 2.0% 2.0% 2.0% 0.6% 4.0% 4.8% 4.6% 4.5% 3.8% 3.5% 1.9% 2.5% 1.8% 1.7% 0.2% 1.0% 0.7% 1.1% -0.4% Jan-21 Jan-22 Jun-22 euro area Germany France Spain Source: calculations on Eurostat data. Food includes alcohol and tobacco. Figures for Spain refer to data as of May 2022. 24

MACROECONOMIC LANDSCAPE Fig. 1.10 – Trends in commodities prices (daily data up to 30 June 2022; 1st January 2019=100) natural gas crude oil coal wheat maize nickel 1,200 500 1,000 400 800 300 600 200 400 200 100 0 0 2019 2020 2021 2022 2019 2020 2021 2022 Source: Refinitiv Datastream. Fig. 1.11 – Net purchases of securities by the ECB (monthly data up to May 2022; amounts in billions of euro) PSPP CBPP3 CSPP ABSPP PEPP Italy Germany France Spain others supranationals net purchases by programme public sector securities net purchases by country 160 160 140 140 120 120 100 100 80 80 60 60 40 40 20 20 0 0 -20 -20 2015 2016 2017 2018 2019 2020 2021 2022 2015 2016 2017 2018 2019 2020 2021 2022 Source: ECB. Monthly net purchases of public sector securities through PEPP programme have been estimated based on bimonthly data. Fig. 1.12 – Trends in public debt and interest expenses in the main euro area countries Spain France Germany Italy 2007 2020 2021 debt-GDP ratio (annual data; 1970-2021) interest expenses as % of GDP 180% 5% 150% 120% 3% 3% 3% 3% 90% 2% 2% 60% 2% 1% 1% 30% 1% 0.5% 0% 1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 Italy Germany France Spain Source: IMF Fiscal Monitor April 2022, IMF Historical Public Debt Database and OECD Sovereign borrowing outlook May 2022. 25

CONSOB Trends and risks of the Italian financial system in a comparative perspective - 2022 Fig. 1.13 – Public debt and deficit to GDP ratio in the main euro area countries 2022 2021 public debt / GDP average euro area 2022, 95% public deficit / GDP average euro area 2022, 4% 151% 113% 118% 7% 7% 7% 69% 148% 4% 111% 115% 66% 6% 5% 5% Italy Germany France Spain Italy Germany 3% France Spain Source: European Commission Economic Forecasts Spring 2022, May 2022. Fig. 1.14 – Private debt to GDP ratio in the main euro area countries 2019 2020 2021 non-financial corporations households 173% 69% 67% 167% 153% 62% 62% 58% 57% 57% 58% 54% 45% 44% 107% 41% 93% 103% 77% 74% 73% 68% 73% 59% Italy Germany France Spain Italy Germany France Spain Source: Bank for the International Settlements. 26

MACROECONOMIC LANDSCAPE ENERGY DEPENDENCE AND TRADE WITH RUSSIA Fig. 1.15 – Energy consumption by source in selected countries in 2020 (share on total consumption) coal oil natural gas nuclear hydropower wind solar other renewables global 28% 32% 25% 4% 7% Italy 4% 38% 43% 7% 4% US 11% 38% 35% 9% 4% Germany 16% 36% 27% 5% 10% UK 36% 39% 7% 10% France 31% 17% 37% 6% EU 11% 37% 25% 11% 6% 6% Spain 45% 24% 11% 5% 10% Source: Statistical Review of World Energy trough OurWorldinData; https://ourworldindata.org/energy. Primary energy is calculated based on the 'substitution method' which takes account of the inefficiencies in fossil fuel production by converting non-fossil energy into the energy inputs required if they had the same conversion losses as fossil fuels. Fig. 1.16 – Natural gas imports from Russia (annual data; values in million cubic meters) EU Germany France Italy Spain average 2011-2019 2020 trend over time share of total natural gas imports 200,000 65% 160,000 45% 120,000 41% 43% 39% 36% 80,000 17% 17% 40,000 10% 1% 0 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 EU Italy Germany France Spain Source: calculations on Eurostat data. Fig. 1.17 – EU sources of natural gas and volumes imported from Russia in 2021 and 2022 domestic production Russia LNG 2021 Norway Algeria Libya Azerbaijan 2022 composition by sources natural gas imports from Russia (billions of cubic meters) 6% 9% 8% 8% 5% 6% 9% 15.8 15.7 19% 22% 24% 21% 21% 21% 22% 12.4 12.5 12.8 12.4 11.9 8% 8% 11% 11% 19% 20% 18% 9.5 9.1 8.3 36% 39% 7.0 40% 41% 40% 38% 38% 4.5 24% 21% 19% 17% 15% 13% 9% 2015 2016 2017 2018 2019 2020 2021 Jan Feb Mar Apr May Jun Source: calculations on Bruegel data. 27

CONSOB Trends and risks of the Italian financial system in a comparative perspective - 2022 Fig. 1.18 – Natural gas storage in the EU (share on total capacity) EU 2021 EU 2022 Italy 2021 Italy 2022 trend over time level as of 30 June 2022 100 72.2 80 58.9 61.2 62.4 58.2 60 40 20 0 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec EU average Italy Germany France Spain Source: AGSI Aggregated Gas Storage Inventory; https://agsi.gie.eu/#/. Fig. 1.19 – Italian electricity production by source and reliance on Russian imports by sectorial end-uses (annual data; values in TWh) coal gas oil hydropower solar wind other renewables Russian coal Russian natural gas Russian oil other sources sources of electricity production energy sources by end-uses 350 manufacturing 300 250 transport 200 residential 150 agricolture 100 services and others 50 electricity generation 0 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 0% 20% 40% 60% 80% 100% Source: BP Statistical Review of World Energy & Ember through OurWorld in Data and IEA statistics. Fig. 1.20 – Trade of EU with Russia over time net exports imports exports 30 20 10 0 -10 -20 -30 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Source: Eurostat. 28

MACROECONOMIC LANDSCAPE Fig. 1.21 – Composition of imports and exports of EU and Italy with Russia (amounts in billions of euro) food raw materials & oil manufactured goods chemicals commodities & others machinery & transport equipment European Union Italy 100 15 75 10 50 5 25 0 0 imports exports imports exports imports exports imports exports Jan-Apr 2021 Jan-Apr 2022 Jan-Apr 2021 Jan-Apr 2022 Source: calculations on Eurostat and ISTAT data. Fig. 1.22 – Italian main countries of imports and exports (data as of April 2022) imports exports Germany 16.0% Germany 13.0% France 8.3% France 10.2% China 8.2% USA 9.6% Netherlands 5.9% Switzerland 5.3% Spain 5.1% Spain 4.9% Belgium 4.5% UK 4.5% Russia 3.7% Belgium 3.5% USA 3.3% Poland 3.1% Poland 2.5% China 3.0% Switzerland 2.4% Netherlands 2.9% Austria 2.3% Austria 2.2% Turkey 2.1% Turkey 1.8% UK 1.7% Romania 1.6% Czech Republic 1.6% Russia 1.5% Romania 1.5% Japan 1.5% Source: ISTAT. 29

CONSOB Trends and risks of the Italian financial system in a comparative perspective - 2022 EUROPEAN SUPPORT MEASURES AND NATIONAL PLANS Fig. 1.23 – REPowerEU: actions and additional investments (billions of euro) renewables and hydrogen infrastructure 113 energy efficiency and heat pump 56 less fossil fuels used by industry 41 biomethane production 37 greater electricity use 29 sufficient liquefied natural gas 10 security of oil supply 2 other 12 Source: https://ec.europa.eu/commission/presscorner/api/files/attachment/872551/FS%20Financing%20REPowerEU.pdf. Fig. 1.24 – NextGenerationEU green bonds eligible amount (billions of euro) 69.9 26.4 13.9 12.2 10.3 6.1 5.4 2.4 2.4 2.3 2.0 1.8 1.0 0.6 0.6 0.6 0.5 0.4 0.4 0.3 0.2 0.0 Source: https://ec.europa.eu/info/strategy/eu-budget/eu-borrower-investor-relations/nextgenerationeu-green-bonds/dashboard_en. Expenditure in Member States’ Recovery and Resilience Plans that is eligible for being included in the pool of NextGenerationEU green bonds financing Fig. 1.25 – Recovery and resiliency plans (RRPs) endorsed by the European commission (distribution of total planned spending by green, digital and resilience components) green digital resilience 6% 7% 16% 16% 23% 26% 23% 20% 15% 38% 33% 32% 39% 30% 36% 37% 36% 36% 36% 35% 36% 38% 42% 32% 40% 40% 52% 25% 26% 39% 27% 27% 26% 21% 28% 32% 21% 21% 23% 20% 32% 22% 21% 21% 22% 21% 25% 23% 21% 22% 59% 61% 54% 59% 37% 46% 42% 40% 38% 45% 50% 37% 38% 38% 43% 42% 41% 40% 42% 42% 43% 44% 42% 50% 41% Source: https://ec.europa.eu/info/business-economy-euro/recovery-coronavirus/recovery-and-resilience-facility_en, retrieved 11 July 2022. Resilience (economic and social) includes, for example, investment in social and territorial cohesion, labour market policies, healthcare sector, public administration, productivity and competitiveness, policies for the next generation, education and skills. 30

MACROECONOMIC LANDSCAPE Fig. 1.26 – Twin transitions: climate neutrality and digital transitions target EU planned for 25 EU Member States 37% green spending 45% 20% digital spending 26% Source: https://ec.europa.eu/info/business-economy-euro/recovery-coronavirus/recovery-and-resilience-facility_en, retrieved 11 July 2022. Fig. 1.27 – RRF Commission’s disbursements (1st payment) per Member State (billions of euro) number of targets/milestones achieved disbursement 52 51 38 38 21 15 10 7.4 3.6 1.2 Spain Italy France Greece Portugal Source: https://ec.europa.eu/economy_finance/recovery-and-resilience-scoreboard, retrieved 30/06/2022. Under the RRF, two types of disbursements can take place. The pre-financings are granted upon request of the Member States. They are paid just after the recovery and resilience plans have been endorsed, are limited to plans endorsed in 2021, and should not exceed 13% of the overall allocation to the Member State. All further disbursements (payment) are made upon request of the Member State and conditional on a positive assessment by the Commission as to the satisfactory fulfilment of a set of relevant milestones and targets. Fig. 1.28 – Italy Policy Pillars: milestones and targets achieved number of milestones/targets to achieve number of milestones/targets achieved digital transformation 157 16 green transition 195 22 smart, sustainable and inclusive growth 206 25 social and territorial cohesion 239 18 health, economic, social and institutional resilience 225 25 policies for the next generation 40 4 Source: calculations on EU Recovery and Resilience scoreboard data, https://ec.europa.eu/economy_finance/recovery-and-resilience- scoreboard, 15/12/2021. This graph displays the share of satisfactorily fulfilled milestones and targets. A milestone or target is fulfilled once a Member State has provided the evidence to the Commission by submitting a payment request (maximum twice a year) that it has completed the milestone or target in a satisfactory manner and the Commission has assessed it positively in an implementing decision. The number of Italian milestones/targets is 527. In the representation of the data, due to overlaps between the different policy pillars, the total number of milestones/targets is greater than 527. 31

CONSOB Trends and risks of the Italian financial system in a comparative perspective - 2022 Fig. 1.29 – Italian PNRR deadlines deadlines before the end of 2022 deadlines before 2026 392 51 38 7 31 43 4 5 5 by 30/3/22 by 30/6/22 by 30/9/22 by 31/12/22 to start in progress well advanced completed late Source: https://openpnrr.it/, the data refers to European deadlines. retrieved 11 July 2022. 32

MACROECONOMIC LANDSCAPE 33

Mercati azionari Equity markets

Andamento dei corsi azionari Volatilità e liquidità Multipli di borsa Indicatori di interconnessione tra mercati Equity markets trends Volatility and liquidity Multiples Connectedness among stock markets 35

CONSOB Congiuntura e rischi del sistema finanziario italiano in una prospettiva comparata - 2022 Nel primo semestre 2022, i corsi azio- In the first half of 2022, in the major nari delle principali economie avanzate advanced economies stock prices declined hanno registrato un calo in conseguenza as a result of the worsening del peggioramento del quadro macro- macroeconomic environment also linked economico legato anche all’invasione to the invasion of Ukraine. The dell’Ucraina. L’EuroStoxx50 nell’area euro EuroStoxx50 in the euro area and the e lo S&P500 negli USA hanno subito una S&P500 in the US suffered a loss of about perdita di 20 punti percentuali circa, 20 percentage points, while the Ftse100 in mentre il Ftse100 nel Regno Unito ha the UK experienced a smaller decline of registrato una contrazione più ridotta e about 3 percentage points. Over the same pari a 3 punti percentuali circa. Nelle time period, in emerging economies drops economie emergenti le flessioni dei corsi in stock prices ranged from about 7% in azionari oscillano, nel periodo in esame, the Shanghai SE index to 42% in the Moex tra il 7% circa dell’indice Shanghai SE e il index. In all markets considered, volatility 42% dell’indice Moex. In tutti i mercati increased significantly, although in the considerati la volatilità è aumentata in advanced countries it remained below the misura significativa, anche se nei paesi peaks recorded in previous crisis episodes avanzati si è mantenuta su livelli più (e.g., the default of Lehman and during the contenuti rispetto a episodi di crisi pandemic outbreak; Fig. 2.1 – Fig. 2.2). precedenti (ad esempio, rispetto ai picchi registrati in occasione del fallimento Lehman e dello scoppio della pandemia; Fig. 2.1 – Fig. 2.2). Per quanto riguarda il mercato As for Italian market, in the first half italiano, nel primo semestre 2022 il Ftse of 2022 Ftse Mib experienced a decrease Mib ha sperimentato un calo di 22 punti by 22 percentage points, greater than that percentuali, superiore a quello rilevato per recorded by Dax30 (-20%), Cac40 (-17 %) il Dax30 (-20%), il Cac40 (-17%) e l’Ibex35 and Ibex35 (-7%). Similar trends were (-7%). Analoghi andamenti sono stati exhibited by small cap indices, which fell registrati per gli indici small cap, che nello by 19 percentage points in Italy and 25 stesso periodo hanno subito una flessione percentage points in Germany. In the di 19 punti percentuali in Italia e di 25 domestic stock market, price declines punti percentuali in Germania. Nel were uneven across sectors, being most mercato domestico la contrazione dei pronounced in the technology (-30%), corsi è stata disomogenea tra settori, banking (-21%), and manufacturing (-18%) risultando più intensa nei comparti sectors and significantly smaller in the tecnologico (-30%), bancario (-21%), energy sector (-2%; Fig. 2.3 – Fig. 2.5). manifatturiero (-18%) e significativamente più contenuta in quello energetico (-2%; Fig. 2.3 – Fig. 2.5). 36

MERCATI AZIONARI STOCK INDEX PRICES (daily data up to 30 June 2022; 1st January 2020=100) Main advanced economies S&P500 Ftse100 EuroStoxx50 160 140 120 100 80 60 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun 2020 | 2021 | 2022 Main emerging countries Moex Shanghai SE Ftse Brazil Nifty 500 200 150 100 50 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun 2020 | 2021 | 2022 Main euro area countries Cac40 Dax30 Ibex35 Ftse Mib 130 115 100 85 70 55 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun 2020 | 2021 | 2022 Source: Refinitiv Datastream. 37

CONSOB Congiuntura e rischi del sistema finanziario italiano in una prospettiva comparata - 2022 La flessione dei corsi azionari si è The downturn in stock prices was affiancata a un deterioramento della accompanied by a deterioration in the liquidità delle maggiori società quotate, liquidity of the largest listed companies, anche se in modo meno intenso rispetto a although less severe than in previous precedenti periodi di crisi (Fig. 2.6). crisis periods (Fig. 2.6). Nonostante la congiuntura negativa Despite the adverse trend in equity dei mercati azionari, nell’area euro le markets, in the euro area expected aspettative sull’andamento degli utili forward earnings over a 12-month horizon societari su un orizzonte di 12 mesi continue to tilt upward from the lowest hit continuano a mostrare un trend in crescita in 2020, especially for non-financial firms. rispetto al minimo registrato nel 2020, Compared to 2021, signals of a narrowing soprattutto per le imprese non finanziarie. gap between market valuations and Emergono inoltre segnali di riduzione del fundamental values of listed companies divario tra valutazioni di mercato e valori can also be detected, as shown by the fondamentali delle società quotate riscon- sharply decrease both in the cyclically trato nel corso del 2021, a fronte sia della adjusted price-earnings ratio and in dinamica nettamente decrescente del misalignment indicators developed on the price-earnings ratio aggiustato per il ciclo basis of the dividend discount model economico sia di indicatori di disallinea- (Fig. 2.7 – Fig. 2.11). mento elaborati sulla base del dividend discount model (Fig. 2.7 – Fig. 2.11). Nel primo semestre del 2022, The first half of 2022 recorded a nell’area euro si è attenuato il rischio di decline in the risk of a simultaneous, una reazione simultanea e sistemica dei systemic reaction to common exogenous corsi azionari dei mercati domestici a shocks of equity prices in the euro area shocks esogeni comuni, riflettendo domestic markets, likely reflecting verosimilmente le differenze strutturali structural differences among the tra le economie sottostanti anche in underlying economies also in terms of termini di esposizione agli shock stessi1 exposure to the shocks themselves (Fig. 2.12). (Fig. 2.12). 1 Il grado di interconnessione tra i mercati azionari europei è stato stimato distinguendo i paesi denominati core dai paesi cosiddetti periferici, dove il primo gruppo comprende le economie caratterizzate da condizioni di crescita e di finanza pubblica relativamente migliori rispetto a quelle del secondo gruppo. In condizioni normali, i paesi periferici sono esposti soprattutto a fattori idiosincratici e presentano, dunque, un livello di interconnessione più basso di quello stimabile per il gruppo core. In condizioni di crisi, tuttavia, la presenza di uno shock comune tende a ridurre il divario nel grado di interconnessione registrato per entrambi i gruppi di paesi. 38

Puoi anche leggere